The total market value of your portfolio is $20,000,000 and the beta of the portfolio is 1.6.

Fantastic news! We've Found the answer you've been seeking!

Question:

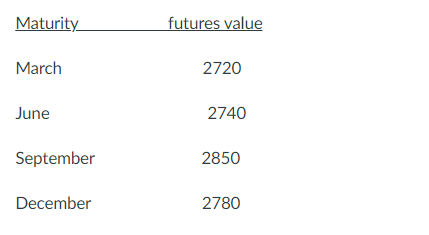

The total market value of your portfolio is $20,000,000 and the beta of the portfolio is 1.6. It is 3/23 and you want to hedge till 5/15. You have the following contracts on the S&P500 index available to you. The correlation between your portfolio and the S&P500 index is +.90.

Which of the following provides the optimal hedge?

Expert Answer:

Answer To determine the optimal hedge we need to calculate the hedge ratio and the number of contrac... View the full answer

Related Book For

Corporate Finance A Focused Approach

ISBN: 978-1439078082

4th Edition

Authors: Michael C. Ehrhardt, Eugene F. Brigham

Posted Date: