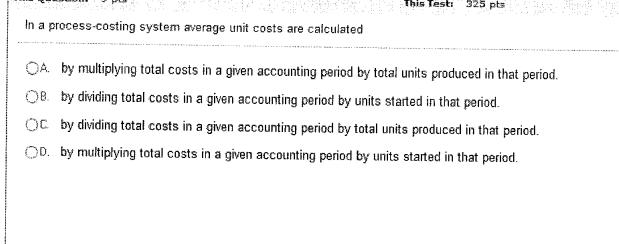

This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

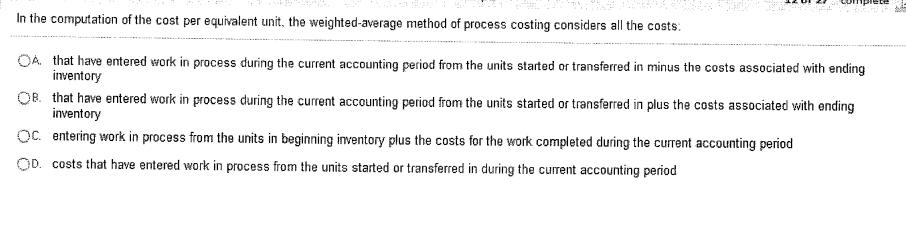

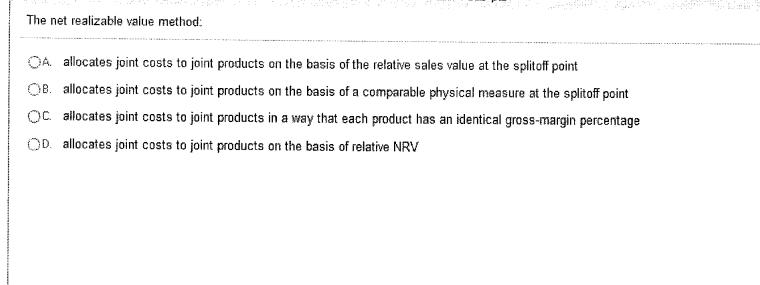

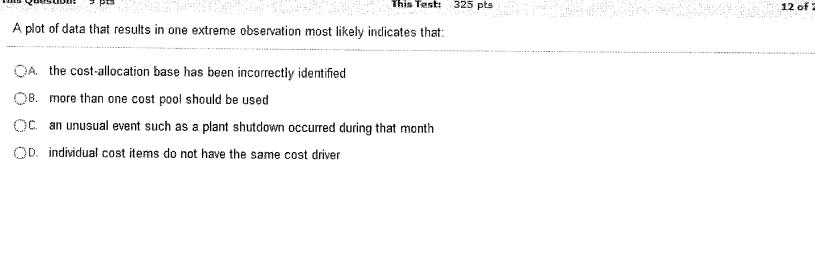

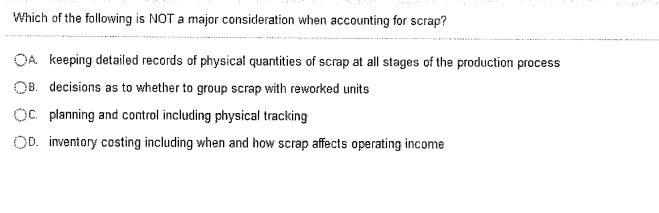

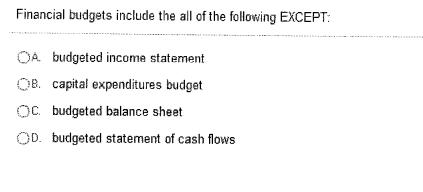

This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows This Test: 325 pts In a process-costing system average unit costs are calculated OA by multiplying total costs in a given accounting period by total units produced in that period. OB by dividing total costs in a given accounting period by units started in that period. OC by dividing total costs in a given accounting period by total units produced in that period. OD. by multiplying total costs in a given accounting period by units started in that period. In the computation of the cost per equivalent unit, the weighted-average method of process costing considers all the costs: OA that have entered work in process during the current accounting period from the units started or transferred in minus the costs associated with ending inventory OB. that have entered work in process during the current accounting period from the units started or transferred in plus the costs associated with ending inventory OC. entering work in process from the units in beginning inventory plus the costs for the work completed during the current accounting period OD. costs that have entered work in process from the units started or transferred in during the current accounting period ete The net realizable value method: OA allocates joint costs to joint products on the basis of the relative sales value at the splitoff point OB. allocates joint costs to joint products on the basis of a comparable physical measure at the splitoff point OC allocates joint costs to joint products in a way that each product has an identical gross-margin percentage OD allocates joint costs to joint products on the basis of relative NRV This Test: A plot of data that results in one extreme observation most likely indicates that: OA. the cost-allocation base has been incorrectly identified OB. more than one cost pool should be used OC an unusual event such as a plant shutdown occurred during that month OD. individual cost items do not have the same cost driver 325 pts 12 of ABC systems use the concept of a costs in the related cost pool. OA cost allocation OB. cost hierarchy OC. cost driver OD. cost pool to identify the cost drivers that best demonstrate the cause-and-effect relationship between each activity and the *********** OA actual market size in units and the budgeted market size in units OB. actual market share and the budgeted market share OC budgeted contribution margin per composite unit for the actual mix and the budgeted contribution margin per composite unit for the budgeted mix OD. actual contribution margin and the budgeted contribution margin Which of the following is NOT one of the three methods of allocating support department costs to operating departments? OA. reciprocal method OB. direct method OC step-down method OD. incremental method In a costing system: OA a cost object should be a product and not a department or a geographic territory OB. cost allocation assigns direct costs OC a cost-allocation base can be either financial or nonfinancial OD. cost tracing allocates indirect costs Many large companies which have multiple production methods and processes have hybrid costing systems that are: OA actual costing OB. a mix of job-costing and process costing O process costing OD. job-costing Design of an ABC system requires: OA an adjustment to product mix OB. that a cause-and-effect relationship exists between resource costs and individual activities OC. that the job bid process be redesigned OD. Both B and C are correct. What is the reason that accountants do NOT like to carry inventory at net realizable value? OA. NRV is acceptable to the taxing authorities QB. NRV is the most difficult costing method OC NRV recognizes income after the sale is complete OD. NRV recognizes income before sales are made Normal spoilage is computed on the basis of the number of: OA. units that are 100% complete as to materials OB. units that pass the inspection point during the current period OC good units that pass inspection during the current period OD. None of these answers is correct. Which of the following is NOT a major consideration when accounting for scrap? OA keeping detailed records of physical quantities of scrap at all stages of the production process OB. decisions as to whether to group scrap with reworked units Oc planning and control including physical tracking OD. inventory costing including when and how scrap affects operating income Financial budgets include the all of the following EXCEPT: OA budgeted income statement OB. capital expenditures budget OC budgeted balance sheet OD. budgeted statement of cash flows

Expert Answer:

Answer rating: 100% (QA)

1 Answer A by dividing total cost in a given accounting period by total unit produced in that period Explanation in process costing system average unit cost is computed by dividing total cost by the t... View the full answer

Related Book For

Cornerstones of Cost Management

ISBN: 978-1111824402

2nd edition

Authors: Don R. Hansen, Maryanne M. Mowen

Posted Date:

Students also viewed these accounting questions

-

The Jacksonville Shirt Company makes two types of T-shirts: basic and custom. Basic shirts are plain shirts without any screen printing on them. Custom shirts are created using the basic shirts and...

-

The Savannah Shirt Company makes two types of T-shirts: basic and custom. Basic shirts are plain shirts without any screen printing on them. Custom shirts are created using the basic shirts and then...

-

In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. It sells the products at cost. The direct materials costs are zero, but the operation...

-

An electron experiences the greatest force as it travels 2.9 X 106 m/s in a magnetic field when it is moving north-ward. The force is upward and of magnitude 7.2 X 10-13N. What are the magnitude and...

-

By some estimates, $185 billion to $260 billion in currency is held outside the United States. a. What is the value to the United States of the seignorage associated with these overseas dollars?...

-

A liquid mixture containing 40% cyclohexane, 20% benzene, 25% toluene, and 15% n-heptane is in equilibrium with its vapor at 1 bar. Determine the temperature and the vapor composition.

-

An audit of inventory records disclosed that the population comprises 20,000 items of inventory. Units within the items vary from 30 to 750 . The values of the units vary from \(20 otin\) to \(\$...

-

1. Suppose 1,000 people would each get a benefit of $40 from a levee. Building the levee is socially efficient if its cost is less than $ _________. If the cost is $30,000, a tax of $_________ per...

-

You purchase a machine for "$X" and secure a 5 yr contract where that machine produces parts (say plastic handles). One year later, you sell your company for 10 times the original cost of the...

-

In Problem 7.3, if no bedrock was present for at least 4 m below the foundation, determine the ultimate bearing capacity. Problem 7.3 A 1.5 m 2.0 m rectangular foundation is placed at 1.0 m depth in...

-

AVM is 21 year old asian who is a new patient in the pharmacy where you work. He presents a prescription for CBZ 100 mg 1 tab BID with instructions to increase to 200 mg 1 tab TID. Currently, he is...

-

Given the following program, how many times is TV Time expected to be printed? Assume 10 seconds is enough time for each task created by the program to complete. A. One time. B. Three times. C. The...

-

How many lines of the following code contain compiler errors? A. All of the lines compile B. One C. Two D. Three E. Four or more. 12: var path = Paths.get(new URI("ice.cool")); 13: var view =...

-

What is the output of the following application? A. true B. false C. The code does not compile. D. The result is unknown until runtime. E. An exception is thrown. F. None of the above. import...

-

Suppose you have the following class in a module named animal.insect.impl. Which two most likely go in the module-info of the service locator? (Choose two.) A. requires animal.insect.api.bugs; B....

-

Which statement about the following method is correct? Assume the directory coffee exists and is able to be read. A. It does not compile. B. It compiles but does not print anything at runtime. C. It...

-

Descriptive analytics is the most viable option for providing directional guidance to managers when: Question 6 options: Available data is limited and high levels of uncertainty exist Only limited...

-

Provide examples of a situations in which environmental disruptions affected consumer attitudes and buying behaviors.

-

Fiorello Company manufactures two types of cold-pressed olive oil, Refined Oil and Top Quality Oil, out of a joint process. The joint (common) costs incurred are $92,500 for a standard production run...

-

What are the main differences between a traditional and an activity-based make-or-buy analysis?

-

What is the role of the controller in an organization? Describe some of the activities over which he or she has control.

-

As the marketing manager for Independent Packaging Pty Ltd, you have asked the accountant what it costs to make the Container2000 model because you want to set a price for the container. A similar...

-

Incomplete information concerning the financial performance of two manufacturing companies is presented below. Required Determine the answers to (a) to(f) for the two companies. Work in process,...

-

Smart Manufacturing Systems Pty Ltd uses a periodic inventory system and closes its accounts on 30 June each year. The companys closing entries made on 30 June 2025 were as shown below. Required (a)...

Study smarter with the SolutionInn App