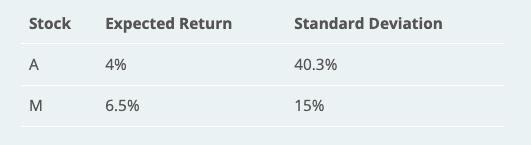

Assume that the market (M), stocks A have the following characteristics: Stock Expected Return Standard Deviation A

Fantastic news! We've Found the answer you've been seeking!

Question:

Assume that the market (M), stocks A have the following characteristics: Stock Expected Return Standard Deviation A 4% 40.3% M 6.5% 15% The risk-free rate is 3%. The correlation for stock return with the market is Corr(RetA, RetM) = 0.35 First, calculate the betas for stock A. According to the CAPM, comment on whether stocks A is underpriced or overpriced, and whether it is above or below the Security Market Line (SML).

Expert Answer:

Related Book For

Accounting What the Numbers Mean

ISBN: 978-0073527062

9th Edition

Authors: David H. Marshall, Wayne W. McManus, Daniel F. Viele,

Posted Date: