Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

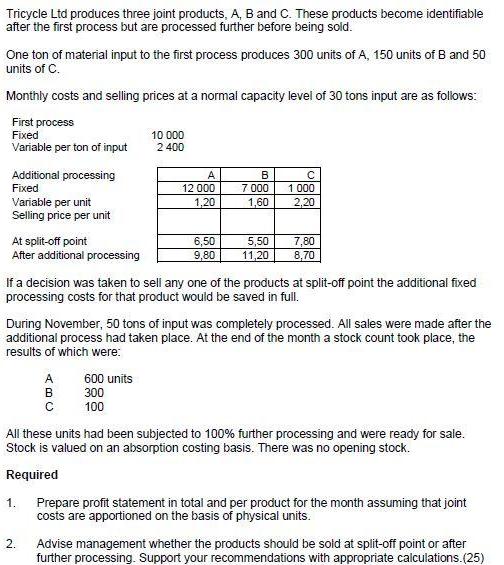

Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25) Tricycle Ltd produces three joint products, A, B and C. These products become identifiable after the first process but are processed further before being sold. One ton of material input to the first process produces 300 units of A, 150 units of B and 50 units of C. Monthly costs and selling prices at a normal capacity level of 30 tons input are as follows: First process Fixed Variable per ton of input Additional processing Fixed Variable per unit Selling price per unit At split-off point After additional processing 1. A 600 units 300 2. 10 000 2 400 BC A 12 000 1,20 с 100 6,50 9,80 If a decision was taken to sell any one of the products at split-off point the additional fixed processing costs for that product would be saved in full. B 7 000 1,60 During November, 50 tons of input was completely processed. All sales were made after the additional process had taken place. At the end of the month a stock count took place, the results of which were: 5,50 11,20 с 1 000 2,20 7,80 8,70 All these units had been subjected to 100% further processing and were ready for sale. Stock is valued on an absorption costing basis. There was no opening stock. Required Prepare profit statement in total and per product for the month assuming that joint costs are apportioned on the basis of physical units. Advise management whether the products should be sold at split-off point or after further processing. Support your recommendations with appropriate calculations.(25)

Expert Answer:

Answer rating: 100% (QA)

1 Profit Statement Total and Per Product Lets calculate the joint costs allocation based on the physical units produced Total Joint Costs Fixed Joint ... View the full answer

Related Book For

Cost Accounting A Managerial Emphasis

ISBN: 978-0133392883

6th Canadian edition

Authors: Horngren, Srikant Datar, George Foster, Madhav Rajan, Christ

Posted Date:

Students also viewed these accounting questions

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

H. Brown (Portsmouth) Ltd produces a range of central heating systems for sale to builders merchants. As a result of increasing demand for the businesss products, the directors have decided to expand...

-

What similarities are there in the inventories of a manufacturing and a merchandising organization? What are the differences?

-

Implement the following method using Fork/Join to find the sum of a list. public static double parallelSum(double[] list) Write a test program that finds the sum in a list of 9,000,000 double values.

-

The data given below show percentages of work completed for a construction project: Graph the data in Excel and comment on the shapes of the distributions. Forecast the cumulative percentages of...

-

Publishers, Inc., has two departments: printing and binding. Each department has one direct-cost category (direct materials) and one indirect-cost category (conversion costs). This problem focuses on...

-

Explore the concept of demand paging in virtual memory systems. What are some common page replacement policies, such as Least Recently Used (LRU) and Clock/Second Chance, and how do they impact...

-

1. Which process should VBB choose to produce?? 2. How much would VBP be willing to pay for the testing that is currently offered, for each batch?? 3. Would we be considered a perfect test, at twice...

-

A soy bean farmer sells soy bean futures to try to hedge some of their exposure to changing soy bean prices. Unfortunately the soybeans that are deliverable into the contract are not the same as the...

-

A plane is flying at an altitude of 10,000 meters and a speed of \(810 \mathrm{~km} / \mathrm{hr}\). The fuselage of the plane can be considered a cylinder of diameter \(4 \mathrm{~m}\) and length...

-

A giant submarine needs to travel great distances to reach destinations. The submarine can be modeled as a cylinder with a radius of \(7 \mathrm{~m}\), a length of \(50 \mathrm{~m}\), and a weight of...

-

What characteristics of a spherical particle are required for its terminal velocity in air at \(25^{\circ} \mathrm{C}\) to just enter the turbulent regime, \(R e_{d}=R e_{d c}\) ?

-

Golf balls have had dimples in them for well over a century after it was first discovered that dimpled balls could be driven farther. Now we know that the dimples trip up the boundary layer and...

-

A sailboard is gliding across a lake at a speed of \(20 \mathrm{mph}(9 \mathrm{~m} / \mathrm{s})\). The sailboard is \(3 \mathrm{~m}\) long, \(0.75 \mathrm{~m}\) wide and represents a smooth, flat...

-

Examine the code below from the AVLTree class and explain in convincing detail what the possible child configurations for the node to be removed all and how the code handles each of those cases. Be...

-

Saccharin is an artificial sweetener that is used in diet beverages. In order for it to be metabolized by the body, it must pass into cells. Below are shown the two forms of saccharin. Saccharin has...

-

Gower Inc., a manufacturer of plastic products, reports the following manufacturing costs and account analysis classification for the year ended December 31, 2012. Gower Inc., produced 75,000 units...

-

Hamilton Semiconductors manufactures specialized chips that sell for $20 each. Hamilton's manufacturing costs consist of variable cost of $2 per chip and fixed costs of $9,000,000. Hamilton also...

-

Low Tech Toys (LTT) produces dolls in two processes: moulding and assembly. LTT is currently producing two models: Chatty Chelsey and Talking Tanya. Production in the Moulding department is limited...

-

A stock's beta is a measure of the stock's: A. total risk. B. market risk. C. unsystematic risk.

-

The larger the standard deviation of an asset's returns, the greater is the assets: A. total risk. B. market risk. C. unsystematic risk.

-

Which of the following is most likely considered a negative covenant? A. The company must maintain a current ratio of 2.0 or above. B. The company must maintain insurance on specific property. C. The...

Study smarter with the SolutionInn App