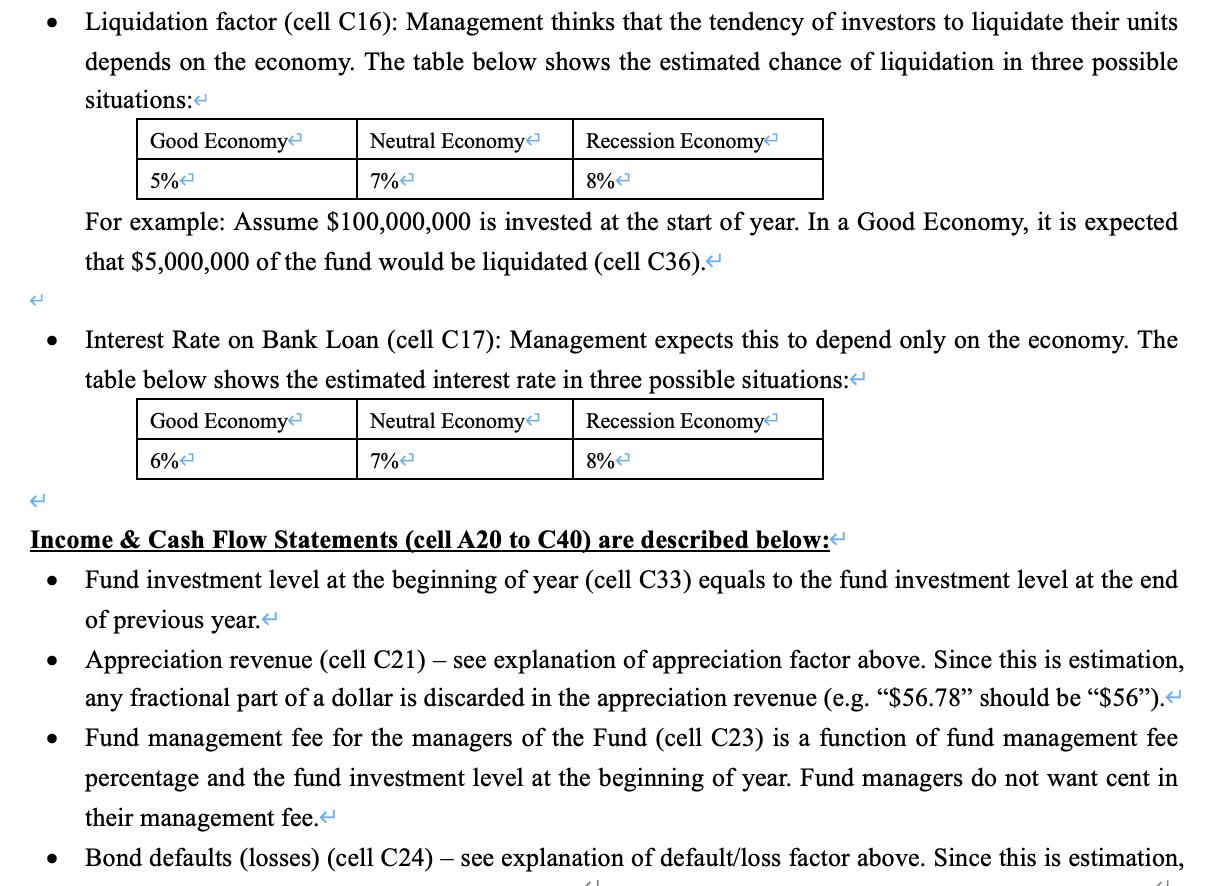

TUV Investment Company manages a family of mutual funds. TUV recently started a new fund called...

Fantastic news! We've Found the answer you've been seeking!

Question:

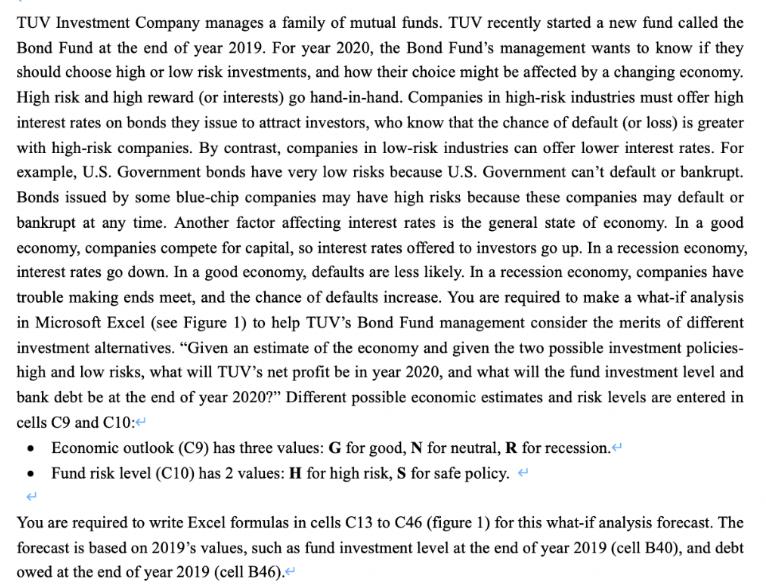

![В 2020 34 ?? [0.5 mark] ?? (0.5 mark] ?? [1 mark] ?? [1 mark] 32 2019 FUND INVESTMENT LEVEL NA 33 AT BEGINNING OF YEAR ADD: F](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2021/10/616cf7b3c6eaf_1634531251047.jpg)

Transcribed Image Text:

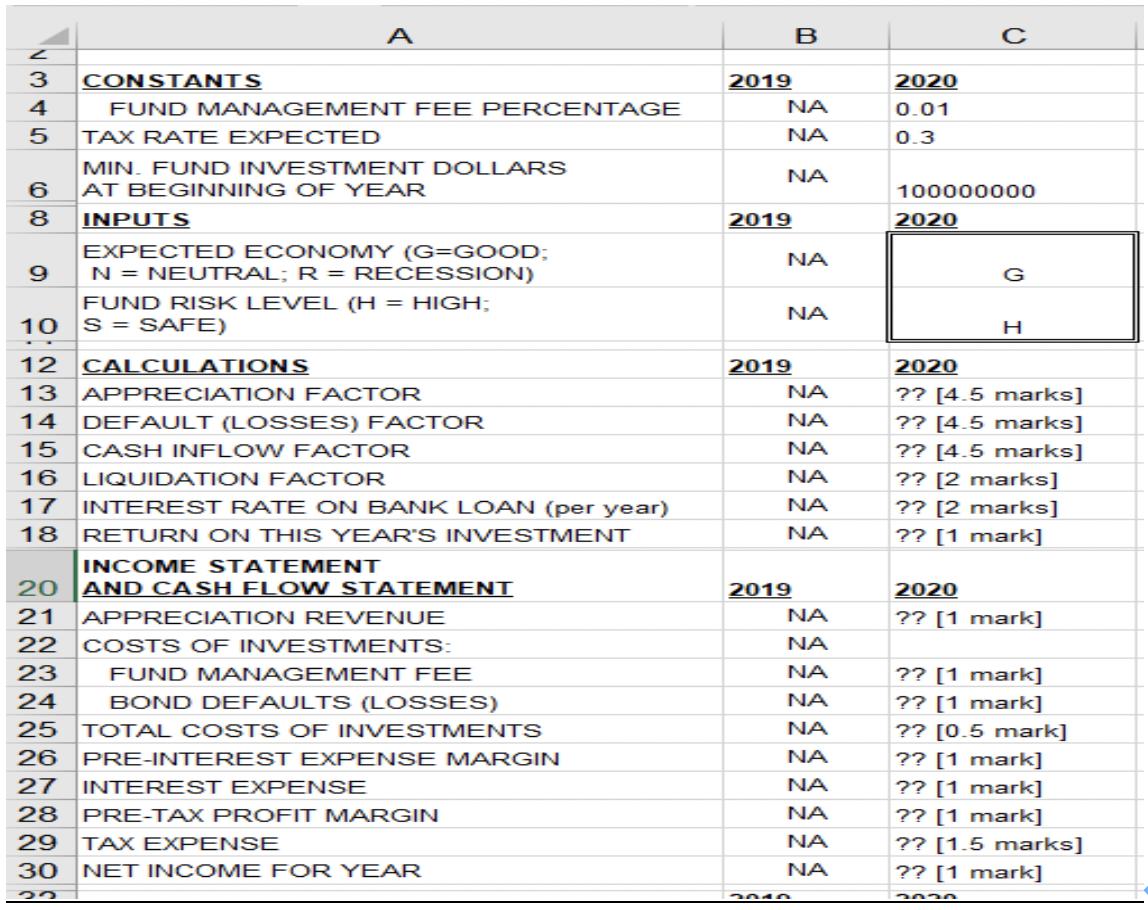

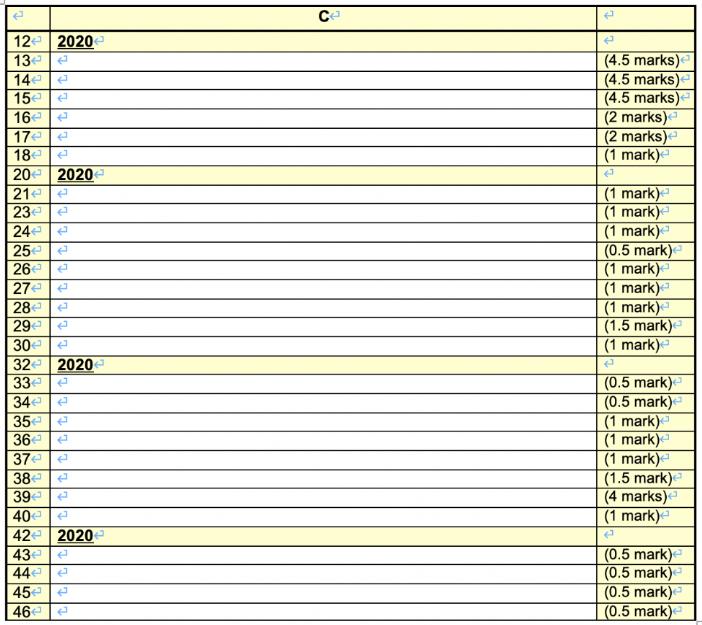

TUV Investment Company manages a family of mutual funds. TUV recently started a new fund called the Bond Fund at the end of year 2019. For year 2020, the Bond Fund's management wants to know if they should choose high or low risk investments, and how their choice might be affected by a changing economy. High risk and high reward (or interests) go hand-in-hand. Companies in high-risk industries must offer high interest rates on bonds they issue to attract investors, who know that the chance of default (or loss) is greater with high-risk companies. By contrast, companies in low-risk industries can offer lower interest rates. For example, U.S. Government bonds have very low risks because U.S. Government can't default or bankrupt. Bonds issued by some blue-chip companies may have high risks because these companies may default or bankrupt at any time. Another factor affecting interest rates is the general state of economy. In a good economy, companies compete for capital, so interest rates offered to investors go up. In a recession economy, interest rates go down. In a good economy, defaults are less likely. In a recession economy, companies have trouble making ends meet, and the chance of defaults increase. You are required to make a what-if analysis in Microsoft Excel (see Figure 1) to help TUV's Bond Fund management consider the merits of different investment alternatives. "Given an estimate of the economy and given the two possible investment policies- high and low risks, what will TUV's net profit be in year 2020, and what will the fund investment level and bank debt be at the end of year 2020?" Different possible economic estimates and risk levels are entered in cells C9 and C10:e • Economic outlook (C9) has three values: G for good, N for neutral, R for recession. • Fund risk level (C10) has 2 values: H for high risk, S for safe policy. You are required to write Excel formulas in cells C13 to C46 (figure 1) for this what-if analysis forecast. The forecast is based on 2019's values, such as fund investment level at the end of year 2019 (cell B40), and debt owed at the end of year 2019 (cell B46). You are required to write Excel formulas in cells C13 to C46 (figure 1) for this what-if analysis forecast. The forecast is based on 2019's values, such as fund investment level at the end of year 2019 (cell B40), and debt owed at the end of year 2019 (cell B46). To understand the operation in TUV, here is some background information on TUV. In late 2019, Fund managers started the Fund with $100 million, which was financed by having $10 million borrowed from (or owed to) the bank and $90 million invested from Fund's investors. The Fund managers invested in securities, and sold shares in the Fund, and the net income for year 2019 was $6 million. Thus the return on the initial investment was 6%, which is the "Return on This Year's Investment" (ROI) in cell C18 - net income divided by total dollars invested at the start of year. At the end of year 2019, the Fund investment level was $106 million, which was reinvested in the following year. Managers of the Bond Fund charge the Fund 1% (cell C4) of the total dollars invested as management fee, which forms part of Fund managers' salaries. However, this management fee is an expense to the Fund. Other Fund expenses include taxes, and losses when bond issuers default because of bankruptcy. Bond Fund managers gain money to invest in bonds in three ways: Net income from previous years reinvested in new bonds. Investors send in money for units of the Bond Fund; this is called "inflow factor". Bond Fund managers borrow money from the bank if total dollars in Bond Fund at the end of year fall below $100 million, which is the minimum fund investment dollars at the beginning of year 2020 (cell C6). - The Bond Fund's total invested dollars could be reduced in two ways: Investors cash out their units, and fund managers must liquidate some Fund investments to pay these investors. This is called the "liquidation factor". A bond issuer defaults, announcing it is not going to repay its debt. This means that the now-worthless investment must be written off as an expense in the Fund income statement. The following constants (cell A3 to C6) for the forecast are described below: The Fund's management fee is 1% (cell C4) of the total dollars invested at the beginning of; year 2020. The government tax rate on pre-tax profit is in cell C5. TUV's policy is to have at least $100 million in cash on hand at the end of each financial year in order to continue the Bond Fund for the next year. This is called the minimum fund investment dollars required at the start of financial year – cell C6. TUV will obtain bank loans if there is insufficient cash to meet this minimum amount. Calculations (cell A12 to C18) are described below: This part considers some factors and calculates intermediate results necessary for the Income & Cash Flow Statement. These calculations are based on the input values in cell C9 and C10. Appreciation factor (cell C13): This is the average investment interest rate in a year. The investment portfolio "appreciates" (or earns income) at this average interest rate. The better the economy and the higher the risk taken, the higher the appreciation factor. The table below shows the estimated appreciation factor in six possible situations: Good Economy Neutral Economy Recession Economy High Risk Policy 14% 12% 10% Safe Policy 10% 9%e 9%e For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a High Risk Policy, the average interest rate on money invested is 14%, and appreciation revenue (cell C21) would be $14,000,000 in the income statement. Default (Losses) factor (cell C14): This is an estimated % of investment dollars that will be defaulted. The table below shows the average loss rate for year 2020 in six possible situations: Good Economy Neutral Economy Recession Economy High Risk Policy 1% 3% 5% Safe Policy 1% 1% 2% For example: Assume $100,000,000 is invested at the start of year. With a Recession Economy and a High Risk Policy, the average loss rate on money invested is 5%, and bond defaults/losses (cell C24) would be $5,000,000 in the income statement. Cash inflow factor (cell C15): The willingness of investors to buy more units of the Bond Fund depends on the economy and the Bond Fund's prior year ROI. Potential investors watch closely the ROI as a performance measure of the Bond Fund. The better the economy and the better the prior year's ROI, the higher the cash inflow. The table below shows the estimated rate of cash inflow in six possible situations: Good Economy Neutral Economy Recession Economy Prior Year ROI > 0.05 10% 8% 8% Prior Year ROI <= 0.05< 8% 3% 3% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a prior year ROI of 0.06, the inflow rate is 10%, and new investment dollars (cell C35) would be $10,000,000. Liquidation factor (cell C16): Management thinks that the tendency of investors to liquidate their units depends on the economy. The table below shows the estimated chance of liquidation in three possible situations: Good Economye Neutral Economy Recession Economy 5% 7%e 8%e For example: Assume $100,000,000 is invested at the start of year. In a Good Economy, it is expected that $5,000,000 of the fund would be liquidated (cell C36). Interest Rate on Bank Loan (cell C17): Management expects this to depend only on the economy. The table below shows the estimated interest rate in three possible situations: Good Economye Neutral Economy Recession Economy 6%e 7%e 8% Income & Cash Flow Statements (cell A20 to C40) are described below: Fund investment level at the beginning of year (cell C33) equals to the fund investment level at the end of previous year. • Appreciation revenue (cell C21) – see explanation of appreciation factor above. Since this is estimation, any fractional part of a dollar is discarded in the appreciation revenue (e.g. "$56.78" should be "$56"). Fund management fee for the managers of the Fund (cell C23) is a function of fund management fee percentage and the fund investment level at the beginning of year. Fund managers do not want cent in their management fee. Bond defaults (losses) (cell C24) – see explanation of default/loss factor above. Since this is estimation, - any fractional part of a dollar is discarded. Pre-Interest expense margin (cell C26) is total revenue minus total costs and fees. Interest expense (cell C27) must be paid on bank loan. It equals to the interest rate for the year times the amount of debt owed to the bank at the beginning of year. Bank does not want to receive cent in simple interests. Pre-Tax profit margin (cell C28) is the profit before considering tax expense. Tax expense (cell C29) is zero if pre-tax profit margin is zero or negative; otherwise apply the tax rate for the year to the pre-tax profit margin. Government does not want to receive cent in taxes. Investment Inflow (cell C35) – see explanation of cash flow factor above. Since this is estimation, any fractional part of a dollar is discarded. Liquidations (cell C36) – see explanation of liquidation factor above. Since this is estimation, any fractional part of a dollar is discarded. Fund investment level before any payments of debt or borrowings from the bank (cell C37) is the fund investment level at the beginning of year plus net income of the year, plus any investment inflow, and less any liquidations. At the end of year, the Fund's bankers will lend enough money (cell C38) to get the Fund back to the minimum investment level (cell C6). If the Fund's investment level before financing is less than the minimum investment required at the end of year, the Bond Fund must borrow; otherwise there is no need to borrow. If the Fund's investment level is more than the minimum investment required at the start of next business year, and there is outstanding debt, some or all of the outstanding debt (cell C39) can be repaid, but not to take the Fund below its minimum investment level. The Fund's investment level at the end of year (cell C40) is the Fund's investment level before financings plus any borrowings from bank and minus any repayments to bank." Debt Owed (cell A42 to C46) is described below: Debt owed at the beginning of year (cell C43) equals to the debt owed at the end of previous year. Amounts borrowed from the bank (cell C44) and payments of debt bank (cell C45) have been calculated previously in cash flow statement, and they can be copied here. The amount of debt owed at the end of year (cell C46) equals to the debt owed at the beginning of year plus any borrowings and less any repayments of debt of that year. NOTE: Assume that there is no typing mistakes in input cells C9 and C10. B CONSTANTS 2019 2020 FUND MANAGEMENT FEE PERCENTAGE NA 0.01 TAX RATE EXPECTED NA 0.3 MIN. FUND INVESTMENT DOLLARS NA 6 AT BEGINNING OF YEAR 100000000 8 INPUTS 2019 2020 EXPECTED ECONOMY (G=GOOD; N = NEUTRAL; R = RECESSION) NA G FUND RISK LEVEL (H = HIGH; S = SAFE) NA 10 H 12 CALCULATIONS 2019 2020 13 NA ?? [4.5 marks] ?? [4.5 marks] APPRECIATION FACTOR 14 DEFAULT (LOSSES) FACTOR NA 15 CASH INFLOW FACTOR NA ?? [4.5 marks] 16 LIQUIDATION FACTOR NA ?? [2 marks] INTEREST RATE ON BANK LOAN (per year) RETURN ON THIS YEAR'S INVESTM ENT 17 NA ?? [2 marks] 18 NA ?? [1 mark] INCOME STATEMENT 20 AND CASH FLOW STATEMENT 2019 2020 21 APPRECIATION REVENUE NA ?? [1 mark] 22 COSTS OF INVESTMENTS: NA ?? [1 mark] ?? [1 mark] 23 FUND MANAGEMENT FEE NA 24 BOND DEFAULTS (LOSSES) NA 25 TOTAL C OSTS OF INVESTMENTS NA ?? [0.5 mark] ?? [1 mark] ?? [1 mark] ?? [1 mark] 26 PRE-INTEREST EXPENSE MARGIN NA 27 INTEREST EXPENSE NA 28 PRE-TAX PROFIT MARGIN NA 29 TAX EXPENSE NA ?? [1.5 marks] 30 NET INCOME FOR YEAR NA ?? [1 mark] 2020 N345 A B C 32 FUND INVESTMENT LEVEL 33 AT BEGINNING OF YEAR 34 ADD: FUND NET INCOME FOR YEAR 35 ADD: INVESTMENT INFLOW LESS: LIQUIDATIONS 2019 2020 NA ?? [0.5 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] NA NA 36 NA FUND INVESTMENT LEVEL 37 ?? [1 marks] BEFORE FINANCINGS 38 ADD: BORROWINGS FROM BANK NA ?? [1.5 marks] 39 NA ?? [4 marks] ?? [1 mark] LESS: REPAYMENTS TO BANK 40 FUND INVESTMENT LEVEL AT YEAR END 106000000 42 DEBT OWED 2019 2020 43 OWED TO BANK AT BEGINNING OF YEAR NA ?? [0.5 mark] ?? [0.5 mark] ?? [0.5 mark] 44 ADD: BORROWINGS IN YEAR NA 45 LESS: DEBT REPAYMENTS/YR NA 46 EQUALS: OWED TO BANK AT END OF YEAR 1000000o ?? [0.5 mark] Figure 1: (NA stands for Not Applicable) C 12e 2020 13 14ee 15e 16ee 17ee 18 20 2020 21 23 24 (4.5 marks)e (4.5 marks) (4.5 marks) (2 marks) (2 marks) (1 mark) (1 mark) (1 mark) (1 mark) (0.5 mark)e (1 mark) (1 mark) (1 mark) (1.5 mark) (1 mark) 25 26e 27e 28 e 29 30 32 2020 33e 34ee (0.5 mark) (0.5 mark) (1 mark) (1 mark) (1 mark) (1.5 mark) (4 marks) (1 mark) 35e 36e 37 38 e 39e 40e 42 2020 43 (0.5 mark)e (0.5 mark) (0.5 mark) (0.5 mark) 44 45ee 46e TUV Investment Company manages a family of mutual funds. TUV recently started a new fund called the Bond Fund at the end of year 2019. For year 2020, the Bond Fund's management wants to know if they should choose high or low risk investments, and how their choice might be affected by a changing economy. High risk and high reward (or interests) go hand-in-hand. Companies in high-risk industries must offer high interest rates on bonds they issue to attract investors, who know that the chance of default (or loss) is greater with high-risk companies. By contrast, companies in low-risk industries can offer lower interest rates. For example, U.S. Government bonds have very low risks because U.S. Government can't default or bankrupt. Bonds issued by some blue-chip companies may have high risks because these companies may default or bankrupt at any time. Another factor affecting interest rates is the general state of economy. In a good economy, companies compete for capital, so interest rates offered to investors go up. In a recession economy, interest rates go down. In a good economy, defaults are less likely. In a recession economy, companies have trouble making ends meet, and the chance of defaults increase. You are required to make a what-if analysis in Microsoft Excel (see Figure 1) to help TUV's Bond Fund management consider the merits of different investment alternatives. "Given an estimate of the economy and given the two possible investment policies- high and low risks, what will TUV's net profit be in year 2020, and what will the fund investment level and bank debt be at the end of year 2020?" Different possible economic estimates and risk levels are entered in cells C9 and C10:e • Economic outlook (C9) has three values: G for good, N for neutral, R for recession. • Fund risk level (C10) has 2 values: H for high risk, S for safe policy. You are required to write Excel formulas in cells C13 to C46 (figure 1) for this what-if analysis forecast. The forecast is based on 2019's values, such as fund investment level at the end of year 2019 (cell B40), and debt owed at the end of year 2019 (cell B46). You are required to write Excel formulas in cells C13 to C46 (figure 1) for this what-if analysis forecast. The forecast is based on 2019's values, such as fund investment level at the end of year 2019 (cell B40), and debt owed at the end of year 2019 (cell B46). To understand the operation in TUV, here is some background information on TUV. In late 2019, Fund managers started the Fund with $100 million, which was financed by having $10 million borrowed from (or owed to) the bank and $90 million invested from Fund's investors. The Fund managers invested in securities, and sold shares in the Fund, and the net income for year 2019 was $6 million. Thus the return on the initial investment was 6%, which is the "Return on This Year's Investment" (ROI) in cell C18 - net income divided by total dollars invested at the start of year. At the end of year 2019, the Fund investment level was $106 million, which was reinvested in the following year. Managers of the Bond Fund charge the Fund 1% (cell C4) of the total dollars invested as management fee, which forms part of Fund managers' salaries. However, this management fee is an expense to the Fund. Other Fund expenses include taxes, and losses when bond issuers default because of bankruptcy. Bond Fund managers gain money to invest in bonds in three ways: Net income from previous years reinvested in new bonds. Investors send in money for units of the Bond Fund; this is called "inflow factor". Bond Fund managers borrow money from the bank if total dollars in Bond Fund at the end of year fall below $100 million, which is the minimum fund investment dollars at the beginning of year 2020 (cell C6). - The Bond Fund's total invested dollars could be reduced in two ways: Investors cash out their units, and fund managers must liquidate some Fund investments to pay these investors. This is called the "liquidation factor". A bond issuer defaults, announcing it is not going to repay its debt. This means that the now-worthless investment must be written off as an expense in the Fund income statement. The following constants (cell A3 to C6) for the forecast are described below: The Fund's management fee is 1% (cell C4) of the total dollars invested at the beginning of; year 2020. The government tax rate on pre-tax profit is in cell C5. TUV's policy is to have at least $100 million in cash on hand at the end of each financial year in order to continue the Bond Fund for the next year. This is called the minimum fund investment dollars required at the start of financial year – cell C6. TUV will obtain bank loans if there is insufficient cash to meet this minimum amount. Calculations (cell A12 to C18) are described below: This part considers some factors and calculates intermediate results necessary for the Income & Cash Flow Statement. These calculations are based on the input values in cell C9 and C10. Appreciation factor (cell C13): This is the average investment interest rate in a year. The investment portfolio "appreciates" (or earns income) at this average interest rate. The better the economy and the higher the risk taken, the higher the appreciation factor. The table below shows the estimated appreciation factor in six possible situations: Good Economy Neutral Economy Recession Economy High Risk Policy 14% 12% 10% Safe Policy 10% 9%e 9%e For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a High Risk Policy, the average interest rate on money invested is 14%, and appreciation revenue (cell C21) would be $14,000,000 in the income statement. Default (Losses) factor (cell C14): This is an estimated % of investment dollars that will be defaulted. The table below shows the average loss rate for year 2020 in six possible situations: Good Economy Neutral Economy Recession Economy High Risk Policy 1% 3% 5% Safe Policy 1% 1% 2% For example: Assume $100,000,000 is invested at the start of year. With a Recession Economy and a High Risk Policy, the average loss rate on money invested is 5%, and bond defaults/losses (cell C24) would be $5,000,000 in the income statement. Cash inflow factor (cell C15): The willingness of investors to buy more units of the Bond Fund depends on the economy and the Bond Fund's prior year ROI. Potential investors watch closely the ROI as a performance measure of the Bond Fund. The better the economy and the better the prior year's ROI, the higher the cash inflow. The table below shows the estimated rate of cash inflow in six possible situations: Good Economy Neutral Economy Recession Economy Prior Year ROI > 0.05 10% 8% 8% Prior Year ROI <= 0.05< 8% 3% 3% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a prior year ROI of 0.06, the inflow rate is 10%, and new investment dollars (cell C35) would be $10,000,000. Liquidation factor (cell C16): Management thinks that the tendency of investors to liquidate their units depends on the economy. The table below shows the estimated chance of liquidation in three possible situations: Good Economye Neutral Economy Recession Economy 5% 7%e 8%e For example: Assume $100,000,000 is invested at the start of year. In a Good Economy, it is expected that $5,000,000 of the fund would be liquidated (cell C36). Interest Rate on Bank Loan (cell C17): Management expects this to depend only on the economy. The table below shows the estimated interest rate in three possible situations: Good Economye Neutral Economy Recession Economy 6%e 7%e 8% Income & Cash Flow Statements (cell A20 to C40) are described below: Fund investment level at the beginning of year (cell C33) equals to the fund investment level at the end of previous year. • Appreciation revenue (cell C21) – see explanation of appreciation factor above. Since this is estimation, any fractional part of a dollar is discarded in the appreciation revenue (e.g. "$56.78" should be "$56"). Fund management fee for the managers of the Fund (cell C23) is a function of fund management fee percentage and the fund investment level at the beginning of year. Fund managers do not want cent in their management fee. Bond defaults (losses) (cell C24) – see explanation of default/loss factor above. Since this is estimation, - any fractional part of a dollar is discarded. Pre-Interest expense margin (cell C26) is total revenue minus total costs and fees. Interest expense (cell C27) must be paid on bank loan. It equals to the interest rate for the year times the amount of debt owed to the bank at the beginning of year. Bank does not want to receive cent in simple interests. Pre-Tax profit margin (cell C28) is the profit before considering tax expense. Tax expense (cell C29) is zero if pre-tax profit margin is zero or negative; otherwise apply the tax rate for the year to the pre-tax profit margin. Government does not want to receive cent in taxes. Investment Inflow (cell C35) – see explanation of cash flow factor above. Since this is estimation, any fractional part of a dollar is discarded. Liquidations (cell C36) – see explanation of liquidation factor above. Since this is estimation, any fractional part of a dollar is discarded. Fund investment level before any payments of debt or borrowings from the bank (cell C37) is the fund investment level at the beginning of year plus net income of the year, plus any investment inflow, and less any liquidations. At the end of year, the Fund's bankers will lend enough money (cell C38) to get the Fund back to the minimum investment level (cell C6). If the Fund's investment level before financing is less than the minimum investment required at the end of year, the Bond Fund must borrow; otherwise there is no need to borrow. If the Fund's investment level is more than the minimum investment required at the start of next business year, and there is outstanding debt, some or all of the outstanding debt (cell C39) can be repaid, but not to take the Fund below its minimum investment level. The Fund's investment level at the end of year (cell C40) is the Fund's investment level before financings plus any borrowings from bank and minus any repayments to bank." Debt Owed (cell A42 to C46) is described below: Debt owed at the beginning of year (cell C43) equals to the debt owed at the end of previous year. Amounts borrowed from the bank (cell C44) and payments of debt bank (cell C45) have been calculated previously in cash flow statement, and they can be copied here. The amount of debt owed at the end of year (cell C46) equals to the debt owed at the beginning of year plus any borrowings and less any repayments of debt of that year. NOTE: Assume that there is no typing mistakes in input cells C9 and C10. B CONSTANTS 2019 2020 FUND MANAGEMENT FEE PERCENTAGE NA 0.01 TAX RATE EXPECTED NA 0.3 MIN. FUND INVESTMENT DOLLARS NA 6 AT BEGINNING OF YEAR 100000000 8 INPUTS 2019 2020 EXPECTED ECONOMY (G=GOOD; N = NEUTRAL; R = RECESSION) NA G FUND RISK LEVEL (H = HIGH; S = SAFE) NA 10 H 12 CALCULATIONS 2019 2020 13 NA ?? [4.5 marks] ?? [4.5 marks] APPRECIATION FACTOR 14 DEFAULT (LOSSES) FACTOR NA 15 CASH INFLOW FACTOR NA ?? [4.5 marks] 16 LIQUIDATION FACTOR NA ?? [2 marks] INTEREST RATE ON BANK LOAN (per year) RETURN ON THIS YEAR'S INVESTM ENT 17 NA ?? [2 marks] 18 NA ?? [1 mark] INCOME STATEMENT 20 AND CASH FLOW STATEMENT 2019 2020 21 APPRECIATION REVENUE NA ?? [1 mark] 22 COSTS OF INVESTMENTS: NA ?? [1 mark] ?? [1 mark] 23 FUND MANAGEMENT FEE NA 24 BOND DEFAULTS (LOSSES) NA 25 TOTAL C OSTS OF INVESTMENTS NA ?? [0.5 mark] ?? [1 mark] ?? [1 mark] ?? [1 mark] 26 PRE-INTEREST EXPENSE MARGIN NA 27 INTEREST EXPENSE NA 28 PRE-TAX PROFIT MARGIN NA 29 TAX EXPENSE NA ?? [1.5 marks] 30 NET INCOME FOR YEAR NA ?? [1 mark] 2020 N345 A B C 32 FUND INVESTMENT LEVEL 33 AT BEGINNING OF YEAR 34 ADD: FUND NET INCOME FOR YEAR 35 ADD: INVESTMENT INFLOW LESS: LIQUIDATIONS 2019 2020 NA ?? [0.5 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] NA NA 36 NA FUND INVESTMENT LEVEL 37 ?? [1 marks] BEFORE FINANCINGS 38 ADD: BORROWINGS FROM BANK NA ?? [1.5 marks] 39 NA ?? [4 marks] ?? [1 mark] LESS: REPAYMENTS TO BANK 40 FUND INVESTMENT LEVEL AT YEAR END 106000000 42 DEBT OWED 2019 2020 43 OWED TO BANK AT BEGINNING OF YEAR NA ?? [0.5 mark] ?? [0.5 mark] ?? [0.5 mark] 44 ADD: BORROWINGS IN YEAR NA 45 LESS: DEBT REPAYMENTS/YR NA 46 EQUALS: OWED TO BANK AT END OF YEAR 1000000o ?? [0.5 mark] Figure 1: (NA stands for Not Applicable) C 12e 2020 13 14ee 15e 16ee 17ee 18 20 2020 21 23 24 (4.5 marks)e (4.5 marks) (4.5 marks) (2 marks) (2 marks) (1 mark) (1 mark) (1 mark) (1 mark) (0.5 mark)e (1 mark) (1 mark) (1 mark) (1.5 mark) (1 mark) 25 26e 27e 28 e 29 30 32 2020 33e 34ee (0.5 mark) (0.5 mark) (1 mark) (1 mark) (1 mark) (1.5 mark) (4 marks) (1 mark) 35e 36e 37 38 e 39e 40e 42 2020 43 (0.5 mark)e (0.5 mark) (0.5 mark) (0.5 mark) 44 45ee 46e

Expert Answer:

Related Book For

Statistics for Business and Economics

ISBN: 978-0132930192

8th edition

Authors: Paul Newbold, William Carlson, Betty Thorne

Posted Date:

Students also viewed these accounting questions

-

A potential client wants to know if Social Security benefits are included in his gross income for tax purposes. Other than the amount of the Social Security benefits and excluded foreign income, what...

-

The analyst in Exercise 8 wants to know if the mean purchase amount of all transactions is at least $40. a) What is the null hypothesis? b) Is the alternative one- or two-sided? c) 'What is the value...

-

A family of mutual funds maintains a service that allows clients to switch money among accounts through a telephone call. It was estimated that 3.2% of callers either get a busy signal or are kept on...

-

Pam has a $25,900 basis (including her share of debt) in her 50 percent partnership interest in the Meddoc Partnership before receiving any distributions. This year Meddoc makes a current...

-

Discuss the ethical issues involved in researching consumer preferences for toothpaste brands.

-

The following exercise relates to application control objectives for the payroll cycle. 1. List at least two application controls used in the payroll cycle. 2. Give an example of how the associated...

-

What is a unit root test and what are its consequences?

-

The owner of an Italian restaurant has just been notified by her landlord that the monthly lease on the building in which the restaurant operates will increase by 20 percent at the beginning of the...

-

Tucker Tutoring Service Company recorded the following cash transactions for the year: Paid $55,000 for salaries. Paid $7,000 to purchase office equipment. Paid $6,000 for utilities, advertising and...

-

OTE operates in a stable industry and the results for the company were relatively consistent over the past five years. The December 31 year-end statements are provided in Appendix I. There are a few...

-

Elle Corporation started the year with $150,000 in Raw Materials. They used $400,000 worth of materials and ended the year with $180,000 of material on hand. How much material did they purchase...

-

The beam shown in Figure Q1(a) has a cross-sectional area in the shape of I-beam, Figure Q1(b). Determine the maximum bending stress that occurs in the beam at section In order to increase its...

-

Complete the model by filling in the blank cells before answering the question below. Answers should be rounded to the nearest whole number, comma separating 000s, NOT written in currency format. So...

-

(e) Find the volatility of the portfolio in (d). (f) Would anyone prefer stock A to the portfolio in (d)? Why or why not. Suppose that there are two assets: A and B. Asset A has expected return of...

-

Determine which of the below service lines are over budget, and which outpatient service lines are over budget after accounting for workload increases? How is the second of those two calculated?...

-

QUESTIONS 1. SCRPC uses notes to finance its working capital and its seasonal needs. Should the firm use its cost of notes in the measure of the cost of capital? 2. Estimate the firms after-tax cost...

-

Regarding advertising in the medical care sector: Explaintheprosandconsof advertising in the medical care sector. Should there be more or less advertising in the medical care sector? Explain answer....

-

Why is inventory management important for merchandising and manufacturing firms and what are the main tradeoffs for firms in managing their inventory?

-

Write the model specification and define the variables for a multiple regression model to predict college GPA as a function of entering SAT scores and the year in college: freshman, sophomore,...

-

Individuals have their HEI measured on two different days with the first and second day indicated by the variable daycode. A number of researchers argue that individuals will have a higher-quality...

-

Consider two groups of students: B1, students who received high scores on tests, and B2, students who received low scores on tests. In group B1, 80% study more than 25 hours per week, and in group...

-

Do any problems arise when translating physical assets and economic events into monetary units? Give one or two illustrations to support your answer.

-

Entries for the Warren Clinic 2015 income statement are listed below in alphabetical order. Reorder the data in proper format. Depreciation expense General/administrative expenses Interest expense $...

-

Bright Horizons Skilled Nursing Facility, an investor-owned company, constructed a new building to replace its outdated facility. The new building was completed on January 1, 2015, and Bright...

Study smarter with the SolutionInn App