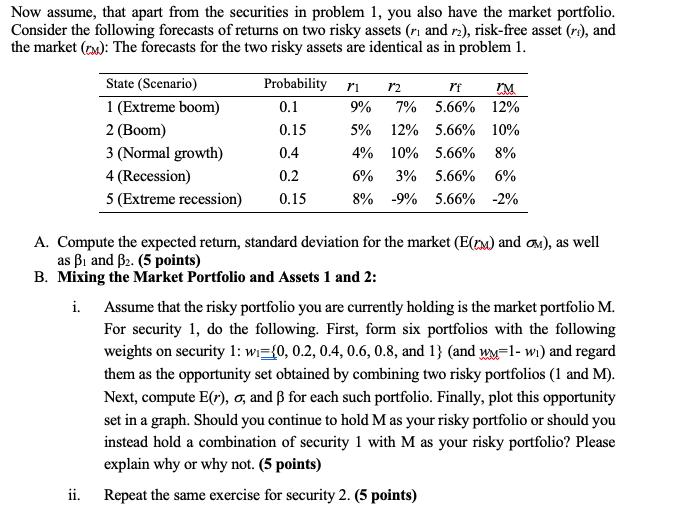

Now assume, that apart from the securities in problem 1, you also have the market portfolio....

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

solution EB B Na KR Page 1 ER EB B ER A first we compute expected return with the help o... View the full answer

Related Book For

Posted Date: