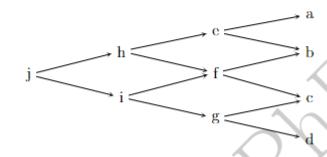

Using a three-period binomial tree, such as the one depicted below, calculate the price of an 18-month,

Question:

Using a three-period binomial tree, such as the one depicted below, calculate the price of an 18-month, at-the-money, European put option written on stock that is trading for $50 today. The option is trading at an implied volatility of 60%. The risk-free rate is equal to 3% per year, continuously compounded, and the stock pays no income.

(B) Using the risk-neutral valuation methodology, flesh-out the components of the option's manufacturing mix at nodes e, f, g, and j, i.e., the quantity of stock and the face value of the risk-free debt included in the option's replicating portfolio, and calculate the amount of leverage embedded in the option at each node.

(C) Based on your calculations other things kept equal, what is the relationship between the option's leverage ratio and its degree of moneyness?

(D) Based on your calculations other things equal, what is the relationship between the option's leverage and its time to maturity?

Expert Answer:

To address your questions we need to build a threeperiod binomial tree for the stock price then use ... View the full answer

Fundamentals of Financial Management

ISBN: 978-1285867977

14th edition

Authors: Eugene F. Brigham, Joel F. Houston