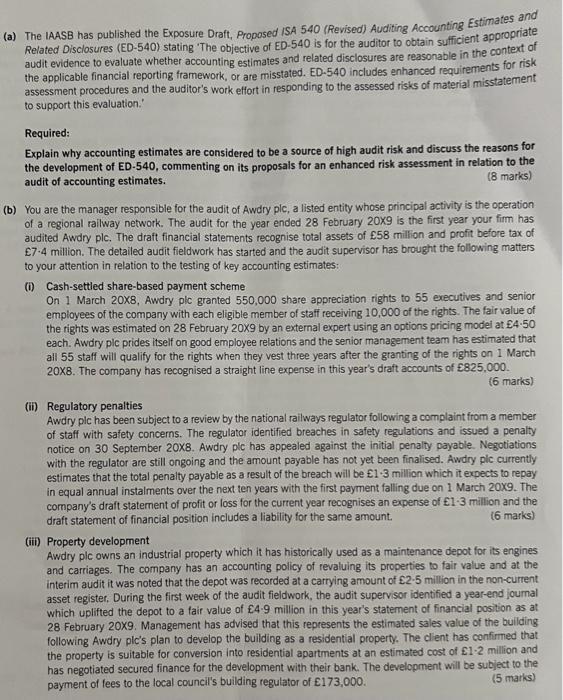

(a) The IAASB has published the Exposure Draft, Proposed ISA 540 (Revised) Auditing Accounting Estimates and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

(a) The IAASB has published the Exposure Draft, Proposed ISA 540 (Revised) Auditing Accounting Estimates and Related Disclosures (ED-540) stating The objective of ED-540 is for the auditor to obtain sufficient appropriate audit evidence to evaluate whether accounting estimates and related disclosures are reasonable in the context of the applicable financial reporting framework, or are misstated. ED-540 includes enhanced requirements for risk assessment procedures and the auditor's work effort in responding to the assessed risks of material misstatement to support this evaluation. Required: Explain why accounting estimates are considered to be a source of high audit risk and discuss the reasons for the development of ED-540, commenting on its proposals for an enhanced risk assessment in relation to the (8 marks) audit of accounting estimates. (b) You are the manager responsible for the audit of Awdry plc, a listed entity whose principal activity is the operation of a regional railway network. The audit for the year ended 28 February 20X9 is the first year your firm has audited Awdry plc. The draft financial statements recognise total assets of £58 million and profit before tax of £7-4 million. The detailed audit fieldwork has started and the audit supervisor has brought the following matters to your attention in relation to the testing of key accounting estimates: (i) Cash-settled share-based payment scheme On 1 March 20X8, Awdry plc granted 550,000 share appreciation rights to 55 executives and senior employees of the company with each eligible member of staff receiving 10,000 of the rights. The fair value of the rights was estimated on 28 February 20X9 by an external expert using an options pricing model at £4-50 each. Awdry plc prides itself on good employee relations and the senior management team has estimated that all 55 staff will qualify for the rights when they vest three years after the granting of the rights on 1 March 20X8. The company has recognised a straight line expense in this year's draft accounts of £825,000. (6 marks) (ii) Regulatory penalties Awdry plc has been subject to a review by the national railways regulator following a complaint from a member of staff with safety concerns. The regulator identified breaches in safety regulations and issued a penalty notice on 30 September 20X8. Awdry plc has appealed against the initial penalty payable. Negotiations with the regulator are still ongoing and the amount payable has not yet been finalised. Awdry plc currently estimates that the total penalty payable as a result of the breach will be £1-3 million which it expects to repay in equal annual instalments over the next ten years with the first payment falling due on 1 March 20X9. The company's draft statement of profit or loss for the current year recognises an expense of £1-3 million and the draft statement of financial position includes a liability for the same amount. (6 marks) (iii) Property development Awdry plc owns an industrial property which it has historically used as a maintenance depot for its engines and carriages. The company has an accounting policy of revaluing its properties to fair value and at the interim audit it was noted that the depot was recorded at a carrying amount of £2-5 million in the non-current asset register. During the first week of the audit fieldwork, the audit supervisor identified a year-end journal which uplifted the depot to a fair value of £4-9 million in this year's statement of financial position as at 28 February 20X9. Management has advised that this represents the estimated sales value of the building following Awdry plc's plan to develop the building as a residential property. The client has confirmed that the property is suitable for conversion into residential apartments at an estimated cost of £1-2 million and has negotiated secured finance for the development with their bank. The development will be subject to the (5 marks) payment of fees to the local council's building regulator of £173,000. Required: (i) Evaluate the client's accounting treatments and the difficulties which you might encounter when auditing each of the accounting estimates described above; and (ii) Design the audit procedures which should now be performed to gather sufficient and appropriate audit evidence. Note: The split of the mark allocation is shown against each of the issues above. (25 marks) (a) The IAASB has published the Exposure Draft, Proposed ISA 540 (Revised) Auditing Accounting Estimates and Related Disclosures (ED-540) stating The objective of ED-540 is for the auditor to obtain sufficient appropriate audit evidence to evaluate whether accounting estimates and related disclosures are reasonable in the context of the applicable financial reporting framework, or are misstated. ED-540 includes enhanced requirements for risk assessment procedures and the auditor's work effort in responding to the assessed risks of material misstatement to support this evaluation. Required: Explain why accounting estimates are considered to be a source of high audit risk and discuss the reasons for the development of ED-540, commenting on its proposals for an enhanced risk assessment in relation to the (8 marks) audit of accounting estimates. (b) You are the manager responsible for the audit of Awdry plc, a listed entity whose principal activity is the operation of a regional railway network. The audit for the year ended 28 February 20X9 is the first year your firm has audited Awdry plc. The draft financial statements recognise total assets of £58 million and profit before tax of £7-4 million. The detailed audit fieldwork has started and the audit supervisor has brought the following matters to your attention in relation to the testing of key accounting estimates: (i) Cash-settled share-based payment scheme On 1 March 20X8, Awdry plc granted 550,000 share appreciation rights to 55 executives and senior employees of the company with each eligible member of staff receiving 10,000 of the rights. The fair value of the rights was estimated on 28 February 20X9 by an external expert using an options pricing model at £4-50 each. Awdry plc prides itself on good employee relations and the senior management team has estimated that all 55 staff will qualify for the rights when they vest three years after the granting of the rights on 1 March 20X8. The company has recognised a straight line expense in this year's draft accounts of £825,000. (6 marks) (ii) Regulatory penalties Awdry plc has been subject to a review by the national railways regulator following a complaint from a member of staff with safety concerns. The regulator identified breaches in safety regulations and issued a penalty notice on 30 September 20X8. Awdry plc has appealed against the initial penalty payable. Negotiations with the regulator are still ongoing and the amount payable has not yet been finalised. Awdry plc currently estimates that the total penalty payable as a result of the breach will be £1-3 million which it expects to repay in equal annual instalments over the next ten years with the first payment falling due on 1 March 20X9. The company's draft statement of profit or loss for the current year recognises an expense of £1-3 million and the draft statement of financial position includes a liability for the same amount. (6 marks) (iii) Property development Awdry plc owns an industrial property which it has historically used as a maintenance depot for its engines and carriages. The company has an accounting policy of revaluing its properties to fair value and at the interim audit it was noted that the depot was recorded at a carrying amount of £2-5 million in the non-current asset register. During the first week of the audit fieldwork, the audit supervisor identified a year-end journal which uplifted the depot to a fair value of £4-9 million in this year's statement of financial position as at 28 February 20X9. Management has advised that this represents the estimated sales value of the building following Awdry plc's plan to develop the building as a residential property. The client has confirmed that the property is suitable for conversion into residential apartments at an estimated cost of £1-2 million and has negotiated secured finance for the development with their bank. The development will be subject to the (5 marks) payment of fees to the local council's building regulator of £173,000. Required: (i) Evaluate the client's accounting treatments and the difficulties which you might encounter when auditing each of the accounting estimates described above; and (ii) Design the audit procedures which should now be performed to gather sufficient and appropriate audit evidence. Note: The split of the mark allocation is shown against each of the issues above. (25 marks)

Expert Answer:

Answer rating: 100% (QA)

a Accounting estimates are considered to be a source of high audit risk because they are inherently subjective and are subject to the judgement of management Accounting estimates can be used to manipu... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Using the data from Problem 11.16, determine which means are different from one another using α = 0.05. In Problem Block Sample 1 Sample 2 Sample 3 13

-

Using the data from Problem 11.19, determine which means are different using = 0.05. In Problem Block Sample 1 Sample 2 Sample 3 Sample4 10

-

Using the data from Problem 11.2, determine which means are different using = 0.05. In Problem Sample apl mple 3 20 17 14 21 10 14 15 17

-

Prepare a personal SWOT analysis (Your personal Strengths and Weaknesses and the external macroeconomic Opportunities and Threats that all of your competitors will assess criteria examples Advantages...

-

Given two stocks and returns for five or six periods, construct combinations of returns in Excel for these two stocks that will produce the following four different correlation coefficients: -1,0,...

-

Describe your new sample. Estimate a bivariate VAR for the price growth for MSA1 (or MSA2) and MS A3. Choose the lag structure optimally. Comment on the estimation results. Assess whether there is...

-

Which of the following is necessary to determine sample size? a. Population size. b. Expected population deviation rate. c. Estimated population monetary error. d. Risk. Choose the correct answer.

-

The Byrd Companys Contributed Capital section of its January 1, 2007 balance sheet is as follows: Preferred stock (6%, $50 par, 8,000 shares authorized, 3,400 shares issued and outstanding) $170,000...

-

Maria just bought 2contracts of put options and, at the same time, 1 contract of call optionon the Swiss francs (SF) in the Philadelphia Stock Exchange at the strike price of 55cents per franc. Each...

-

Refer to the data set pit.csv. Find a confidence interval of the specified level for the mean depth of pits for the following durations and humidity levels. When the sample size is 30 or less,...

-

! Required information Use the following information for Exercises 25-27 below. (Algo) [The following information applies to the questions displayed below.] Carmen Camry operates a consulting firm...

-

Summarize the five steps that make up the financial planning process.

-

List and explain the four common concerns that should guide all financial plans.

-

Interview three heads of household, each from a household representing a different stage of the life cycle orsocioeconomic status. Inquire about their financial planning process and their strategies...

-

Review the six financial accomplishments that may result from studying personal finance. In your opinion, which three are most important? Why?

-

Describe a good, or effective, job interview.

-

Problem 3: The transmission electron micrograph given in the following figures shows atoms (or more precisely, columns of atoms) near the interface between crystals of CdTe and GaAs, both of which...

-

Provide an example of an aggressive accounting practice. Why is this practice aggressive?

-

Grade inflation, which is defined as an increase in the average GPA of an institution over time without a corresponding increase in academic performance, is a concern for many colleges. The presence...

-

The Independence School is a private grade school that depends on enrollment forecasting to plan for the upcoming school year. The following data show the enrollments for the past several years....

-

The following table shows the results of a survey that asked users of the Internet to identify their favorite search engine. These data can be found in the Excel file search engine. xlsx. (For your...

-

Verify that the log-likelihood of model (7.7) is \(\sum_{i=1}^{k}\left[n_{i} \lambda-\exp (\lambda) ight]\). (a) Compute MLE of \(\lambda\). (b) Compute the Pearson chi-square statistic and compare...

-

Think about the general concept of a relationship, not necessarily in a business setting, but just relationships in general between any two parties. What aspects of relationships are inherently...

-

What is value? In what ways does a relationship selling approach add value to your customers, to you the salesperson, and to your sales organization?

Study smarter with the SolutionInn App