Using the footnote for Hertz Rental Car for 2017 below, identify which level of the fair value

Fantastic news! We've Found the answer you've been seeking!

Question:

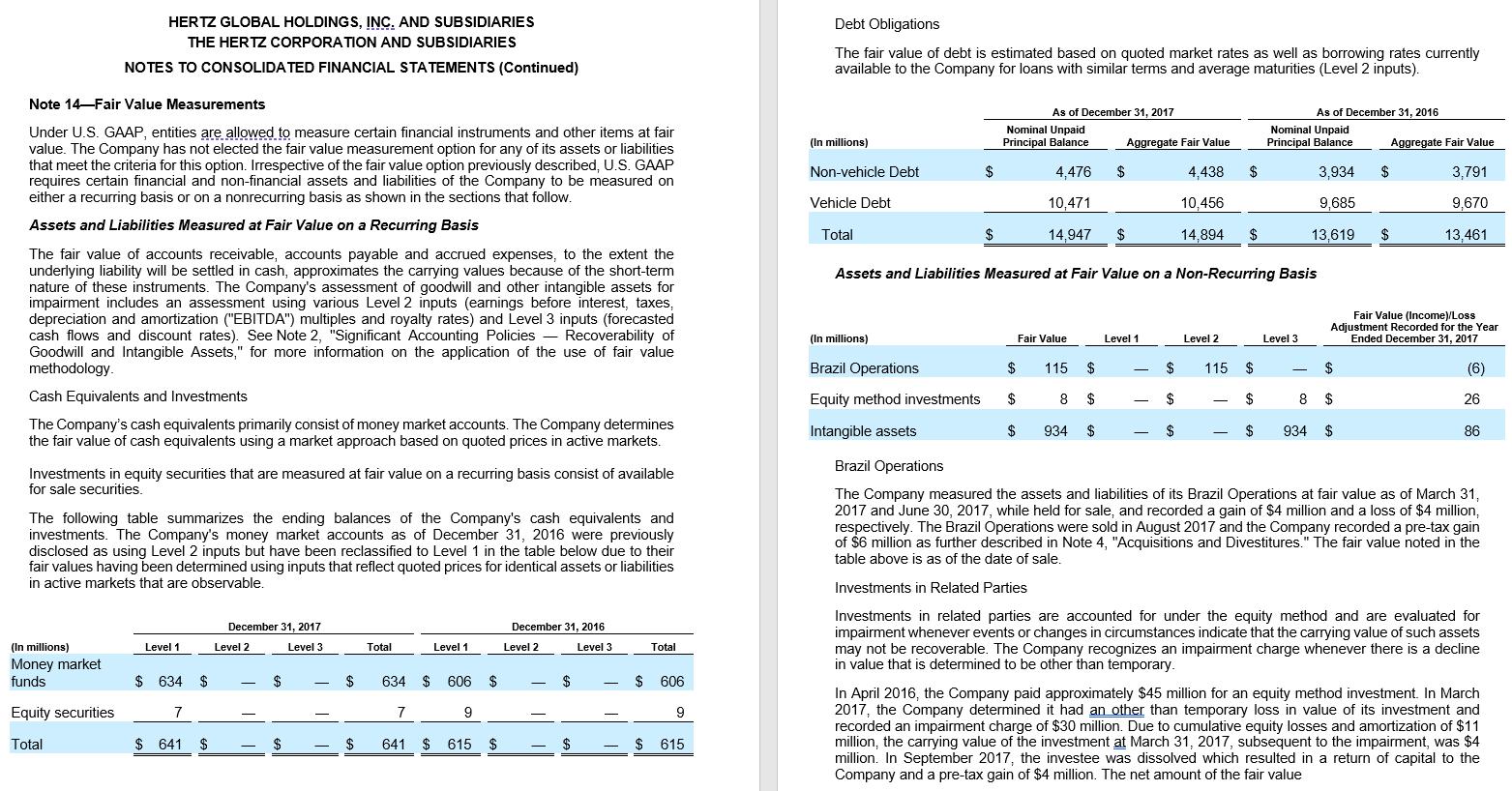

Using the footnote for Hertz Rental Car for 2017 below, identify which level of the fair value hierarchy was used to get the fair value of the following items reported by Hertz at the end of 2017. Investments in Equity Securities Non Vehicle Debt Money market funds Intangible Assets Vehicle Debt Brazil Operations Equity Method investment.

Required:

1. Identify the level of fair value hierarchy used for each asset or liability.

2. Describe how that level inputs were applied to the particular item.

Transcribed Image Text:

HERTZ GLOBAL HOLDINGS, INC. AND SUBSIDIARIES THE HERTZ CORPORATION AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) Note 14-Fair Value Measurements Under U.S. GAAP, entities are allowed to measure certain financial instruments and other items at fair value. The Company has not elected the fair value measurement option for any of its assets or liabilities that meet the criteria for this option. Irrespective of the fair value option previously described, U.S. GAAP requires certain financial and non-financial assets and liabilities of the Company to be measured on either a recurring basis or on a nonrecurring basis as shown in the sections that follow. Assets and Liabilities Measured at Fair Value on a Recurring Basis The fair value of accounts receivable, accounts payable and accrued expenses, to the extent the underlying liability will be settled in cash, approximates the carrying values because of the short-term nature of these instruments. The Company's assessment of goodwill and other intangible assets for impairment includes an assessment using various Level 2 inputs (earnings before interest, taxes, depreciation and amortization ("EBITDA") multiples and royalty rates) and Level 3 inputs (forecasted cash flows and discount rates). See Note 2, "Significant Accounting Policies Recoverability of Goodwill and Intangible Assets," for more information on the application of the use of fair value methodology. Cash Equivalents and Investments The Company's cash equivalents primarily consist of money market accounts. The Company determines the fair value of cash equivalents using a market approach based on quoted prices in active markets. Investments in equity securities that are measured at fair value on a recurring basis consist of available for sale securities. The following table summarizes the ending balances of the Company's cash equivalents and investments. The Company's money market accounts as of December 31, 2016 were previously disclosed as using Level 2 inputs but have been reclassified to Level 1 in the table below due to their fair values having been determined using inputs that reflect quoted prices for identical assets or liabilities in active markets that are observable. (In millions) Money market funds Equity securities Total Level 1 $ 634 $ 7 $ 641 $ December 31, 2017 Level 3 Level 2 - - $ $ - $ $ Total Level 1 634 $ 606 $ 7 641 $ 615 9 $ December 31, 2016 Level 2 Level 3 - $ $ - $ Total 606 9 $ 615 Debt Obligations The fair value of debt is estimated based on quoted market rates as well as borrowing rates currently available to the Company for loans with similar terms and average maturities (Level 2 inputs). (In millions) Non-vehicle Debt Vehicle Debt Total $ (In millions) Brazil Operations Equity method investments Intangible assets As of December 31, 2017 Nominal Unpaid Principal Balance 4.476 $ 10,471 14,947 $ Fair Value Aggregate Fair Value 4,438 10,456 14,894 $ Assets and Liabilities Measured at Fair Value on a Non-Recurring Basis $ 115 $ 8 $ $ $ 934 $ Level 1 $ $ $ Level 2 115 $ - As of December 31, 2016 Nominal Unpaid Principal Balance 3,934 $ 9,685 13.619 $ $ $ Level 3 - Aggregate Fair Value 3,791 9,670 13,461 8 $ 934 $ $ Fair Value (Income)/Loss Adjustment Recorded for the Year Ended December 31, 2017 (6) 26 86 Brazil Operations The Company measured the assets and liabilities of its Brazil Operations at fair value as of March 31, 2017 and June 30, 2017, while held for sale, and recorded a gain of $4 million and a loss of $4 million, respectively. The Brazil Operations were sold in August 2017 and the Company recorded a pre-tax gain of $6 million as further described in Note 4, "Acquisitions and Divestitures." The fair value noted in the table above is as of the date of sale. Investments in Related Parties Investments in related parties are accounted for under the equity method and are evaluated for impairment whenever events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. The Company recognizes an impairment charge whenever there is a decline in value that is determined to be other than temporary. In April 2016, the Company paid approximately $45 million for an equity method investment. In March 2017, the Company determined it had an other than temporary loss in value of its investment and recorded an impairment charge of $30 million. Due to cumulative equity losses and amortization of $11 million, the carrying value of the investment at March 31, 2017, subsequent to the impairment, was $4 million. In September 2017, the investee was dissolved which resulted in a return of capital to the Company and a pre-tax gain of $4 million. The net amount of the fair value HERTZ GLOBAL HOLDINGS, INC. AND SUBSIDIARIES THE HERTZ CORPORATION AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) Note 14-Fair Value Measurements Under U.S. GAAP, entities are allowed to measure certain financial instruments and other items at fair value. The Company has not elected the fair value measurement option for any of its assets or liabilities that meet the criteria for this option. Irrespective of the fair value option previously described, U.S. GAAP requires certain financial and non-financial assets and liabilities of the Company to be measured on either a recurring basis or on a nonrecurring basis as shown in the sections that follow. Assets and Liabilities Measured at Fair Value on a Recurring Basis The fair value of accounts receivable, accounts payable and accrued expenses, to the extent the underlying liability will be settled in cash, approximates the carrying values because of the short-term nature of these instruments. The Company's assessment of goodwill and other intangible assets for impairment includes an assessment using various Level 2 inputs (earnings before interest, taxes, depreciation and amortization ("EBITDA") multiples and royalty rates) and Level 3 inputs (forecasted cash flows and discount rates). See Note 2, "Significant Accounting Policies Recoverability of Goodwill and Intangible Assets," for more information on the application of the use of fair value methodology. Cash Equivalents and Investments The Company's cash equivalents primarily consist of money market accounts. The Company determines the fair value of cash equivalents using a market approach based on quoted prices in active markets. Investments in equity securities that are measured at fair value on a recurring basis consist of available for sale securities. The following table summarizes the ending balances of the Company's cash equivalents and investments. The Company's money market accounts as of December 31, 2016 were previously disclosed as using Level 2 inputs but have been reclassified to Level 1 in the table below due to their fair values having been determined using inputs that reflect quoted prices for identical assets or liabilities in active markets that are observable. (In millions) Money market funds Equity securities Total Level 1 $ 634 $ 7 $ 641 $ December 31, 2017 Level 3 Level 2 - - $ $ - $ $ Total Level 1 634 $ 606 $ 7 641 $ 615 9 $ December 31, 2016 Level 2 Level 3 - $ $ - $ Total 606 9 $ 615 Debt Obligations The fair value of debt is estimated based on quoted market rates as well as borrowing rates currently available to the Company for loans with similar terms and average maturities (Level 2 inputs). (In millions) Non-vehicle Debt Vehicle Debt Total $ (In millions) Brazil Operations Equity method investments Intangible assets As of December 31, 2017 Nominal Unpaid Principal Balance 4.476 $ 10,471 14,947 $ Fair Value Aggregate Fair Value 4,438 10,456 14,894 $ Assets and Liabilities Measured at Fair Value on a Non-Recurring Basis $ 115 $ 8 $ $ $ 934 $ Level 1 $ $ $ Level 2 115 $ - As of December 31, 2016 Nominal Unpaid Principal Balance 3,934 $ 9,685 13.619 $ $ $ Level 3 - Aggregate Fair Value 3,791 9,670 13,461 8 $ 934 $ $ Fair Value (Income)/Loss Adjustment Recorded for the Year Ended December 31, 2017 (6) 26 86 Brazil Operations The Company measured the assets and liabilities of its Brazil Operations at fair value as of March 31, 2017 and June 30, 2017, while held for sale, and recorded a gain of $4 million and a loss of $4 million, respectively. The Brazil Operations were sold in August 2017 and the Company recorded a pre-tax gain of $6 million as further described in Note 4, "Acquisitions and Divestitures." The fair value noted in the table above is as of the date of sale. Investments in Related Parties Investments in related parties are accounted for under the equity method and are evaluated for impairment whenever events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. The Company recognizes an impairment charge whenever there is a decline in value that is determined to be other than temporary. In April 2016, the Company paid approximately $45 million for an equity method investment. In March 2017, the Company determined it had an other than temporary loss in value of its investment and recorded an impairment charge of $30 million. Due to cumulative equity losses and amortization of $11 million, the carrying value of the investment at March 31, 2017, subsequent to the impairment, was $4 million. In September 2017, the investee was dissolved which resulted in a return of capital to the Company and a pre-tax gain of $4 million. The net amount of the fair value HERTZ GLOBAL HOLDINGS, INC. AND SUBSIDIARIES THE HERTZ CORPORATION AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) Note 14-Fair Value Measurements Under U.S. GAAP, entities are allowed to measure certain financial instruments and other items at fair value. The Company has not elected the fair value measurement option for any of its assets or liabilities that meet the criteria for this option. Irrespective of the fair value option previously described, U.S. GAAP requires certain financial and non-financial assets and liabilities of the Company to be measured on either a recurring basis or on a nonrecurring basis as shown in the sections that follow. Assets and Liabilities Measured at Fair Value on a Recurring Basis The fair value of accounts receivable, accounts payable and accrued expenses, to the extent the underlying liability will be settled in cash, approximates the carrying values because of the short-term nature of these instruments. The Company's assessment of goodwill and other intangible assets for impairment includes an assessment using various Level 2 inputs (earnings before interest, taxes, depreciation and amortization ("EBITDA") multiples and royalty rates) and Level 3 inputs (forecasted cash flows and discount rates). See Note 2, "Significant Accounting Policies Recoverability of Goodwill and Intangible Assets," for more information on the application of the use of fair value methodology. Cash Equivalents and Investments The Company's cash equivalents primarily consist of money market accounts. The Company determines the fair value of cash equivalents using a market approach based on quoted prices in active markets. Investments in equity securities that are measured at fair value on a recurring basis consist of available for sale securities. The following table summarizes the ending balances of the Company's cash equivalents and investments. The Company's money market accounts as of December 31, 2016 were previously disclosed as using Level 2 inputs but have been reclassified to Level 1 in the table below due to their fair values having been determined using inputs that reflect quoted prices for identical assets or liabilities in active markets that are observable. (In millions) Money market funds Equity securities Total Level 1 $ 634 $ 7 $ 641 $ December 31, 2017 Level 3 Level 2 - - $ $ - $ $ Total Level 1 634 $ 606 $ 7 641 $ 615 9 $ December 31, 2016 Level 2 Level 3 - $ $ - $ Total 606 9 $ 615 Debt Obligations The fair value of debt is estimated based on quoted market rates as well as borrowing rates currently available to the Company for loans with similar terms and average maturities (Level 2 inputs). (In millions) Non-vehicle Debt Vehicle Debt Total $ (In millions) Brazil Operations Equity method investments Intangible assets As of December 31, 2017 Nominal Unpaid Principal Balance 4.476 $ 10,471 14,947 $ Fair Value Aggregate Fair Value 4,438 10,456 14,894 $ Assets and Liabilities Measured at Fair Value on a Non-Recurring Basis $ 115 $ 8 $ $ $ 934 $ Level 1 $ $ $ Level 2 115 $ - As of December 31, 2016 Nominal Unpaid Principal Balance 3,934 $ 9,685 13.619 $ $ $ Level 3 - Aggregate Fair Value 3,791 9,670 13,461 8 $ 934 $ $ Fair Value (Income)/Loss Adjustment Recorded for the Year Ended December 31, 2017 (6) 26 86 Brazil Operations The Company measured the assets and liabilities of its Brazil Operations at fair value as of March 31, 2017 and June 30, 2017, while held for sale, and recorded a gain of $4 million and a loss of $4 million, respectively. The Brazil Operations were sold in August 2017 and the Company recorded a pre-tax gain of $6 million as further described in Note 4, "Acquisitions and Divestitures." The fair value noted in the table above is as of the date of sale. Investments in Related Parties Investments in related parties are accounted for under the equity method and are evaluated for impairment whenever events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. The Company recognizes an impairment charge whenever there is a decline in value that is determined to be other than temporary. In April 2016, the Company paid approximately $45 million for an equity method investment. In March 2017, the Company determined it had an other than temporary loss in value of its investment and recorded an impairment charge of $30 million. Due to cumulative equity losses and amortization of $11 million, the carrying value of the investment at March 31, 2017, subsequent to the impairment, was $4 million. In September 2017, the investee was dissolved which resulted in a return of capital to the Company and a pre-tax gain of $4 million. The net amount of the fair value HERTZ GLOBAL HOLDINGS, INC. AND SUBSIDIARIES THE HERTZ CORPORATION AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) Note 14-Fair Value Measurements Under U.S. GAAP, entities are allowed to measure certain financial instruments and other items at fair value. The Company has not elected the fair value measurement option for any of its assets or liabilities that meet the criteria for this option. Irrespective of the fair value option previously described, U.S. GAAP requires certain financial and non-financial assets and liabilities of the Company to be measured on either a recurring basis or on a nonrecurring basis as shown in the sections that follow. Assets and Liabilities Measured at Fair Value on a Recurring Basis The fair value of accounts receivable, accounts payable and accrued expenses, to the extent the underlying liability will be settled in cash, approximates the carrying values because of the short-term nature of these instruments. The Company's assessment of goodwill and other intangible assets for impairment includes an assessment using various Level 2 inputs (earnings before interest, taxes, depreciation and amortization ("EBITDA") multiples and royalty rates) and Level 3 inputs (forecasted cash flows and discount rates). See Note 2, "Significant Accounting Policies Recoverability of Goodwill and Intangible Assets," for more information on the application of the use of fair value methodology. Cash Equivalents and Investments The Company's cash equivalents primarily consist of money market accounts. The Company determines the fair value of cash equivalents using a market approach based on quoted prices in active markets. Investments in equity securities that are measured at fair value on a recurring basis consist of available for sale securities. The following table summarizes the ending balances of the Company's cash equivalents and investments. The Company's money market accounts as of December 31, 2016 were previously disclosed as using Level 2 inputs but have been reclassified to Level 1 in the table below due to their fair values having been determined using inputs that reflect quoted prices for identical assets or liabilities in active markets that are observable. (In millions) Money market funds Equity securities Total Level 1 $ 634 $ 7 $ 641 $ December 31, 2017 Level 3 Level 2 - - $ $ - $ $ Total Level 1 634 $ 606 $ 7 641 $ 615 9 $ December 31, 2016 Level 2 Level 3 - $ $ - $ Total 606 9 $ 615 Debt Obligations The fair value of debt is estimated based on quoted market rates as well as borrowing rates currently available to the Company for loans with similar terms and average maturities (Level 2 inputs). (In millions) Non-vehicle Debt Vehicle Debt Total $ (In millions) Brazil Operations Equity method investments Intangible assets As of December 31, 2017 Nominal Unpaid Principal Balance 4.476 $ 10,471 14,947 $ Fair Value Aggregate Fair Value 4,438 10,456 14,894 $ Assets and Liabilities Measured at Fair Value on a Non-Recurring Basis $ 115 $ 8 $ $ $ 934 $ Level 1 $ $ $ Level 2 115 $ - As of December 31, 2016 Nominal Unpaid Principal Balance 3,934 $ 9,685 13.619 $ $ $ Level 3 - Aggregate Fair Value 3,791 9,670 13,461 8 $ 934 $ $ Fair Value (Income)/Loss Adjustment Recorded for the Year Ended December 31, 2017 (6) 26 86 Brazil Operations The Company measured the assets and liabilities of its Brazil Operations at fair value as of March 31, 2017 and June 30, 2017, while held for sale, and recorded a gain of $4 million and a loss of $4 million, respectively. The Brazil Operations were sold in August 2017 and the Company recorded a pre-tax gain of $6 million as further described in Note 4, "Acquisitions and Divestitures." The fair value noted in the table above is as of the date of sale. Investments in Related Parties Investments in related parties are accounted for under the equity method and are evaluated for impairment whenever events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. The Company recognizes an impairment charge whenever there is a decline in value that is determined to be other than temporary. In April 2016, the Company paid approximately $45 million for an equity method investment. In March 2017, the Company determined it had an other than temporary loss in value of its investment and recorded an impairment charge of $30 million. Due to cumulative equity losses and amortization of $11 million, the carrying value of the investment at March 31, 2017, subsequent to the impairment, was $4 million. In September 2017, the investee was dissolved which resulted in a return of capital to the Company and a pre-tax gain of $4 million. The net amount of the fair value

Expert Answer:

Answer rating: 100% (QA)

2017 december 31 money marketing fund total 635 2016 dece... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0132162302

1st edition

Authors: Elizabeth A. Gordon, Jana S. Raedy, Alexander J. Sannella

Posted Date:

Students also viewed these accounting questions

-

Investments in equity securities for which the investor has insignificant influence over the investee are classified for reporting purposes under the fair value method in one of two categories. What...

-

Investments in equity securities are classified in one of three different ways, based on ownership percentage. identify the three ways amd the characteristics of each including how the accounting...

-

All investments in debt securities and investments in equity securities for which the investor lacks significant influence over the operation and financial policies of the investee are classified for...

-

Prestopino Corporation produces motorcycle batteries. Prestopino turns out 1,500 batteries a day at a cost of $6 per battery for materials and labor. It takes the firm 22 days to convert raw...

-

A cylindrical tank with radius 5 m is being filled with water at a rate of 3 m3/ min. How fast is the height of the water increasing?

-

A miniature spectrometer used for chemical analysis has a diffraction grating with 800 slits \(/ \mathrm{mm}\) set \(25.0 \mathrm{~mm}\) in front of the detector "screen." The detector can barely...

-

Because both radial readings on the top of a vertical motor are horizontal, how can you differentiate them?

-

The charter of Cherry Blossom Corporation authorizes the issuance of 900 shares of preferred stock and 3,500 shares of common stock. During a two-month period, Cherry Blossom completed these...

-

Consider flow between two large parallel plates. Fluid is placed between two plates separated by a distance of 8. The upper plate at temperature T2 moves at velocity U while the lower plate at...

-

A heat engine running backward is called a refrigerator if its purpose is to extract heat from a cold reservoir. The same engine running backward is called a heat pump if its purpose is to exhaust...

-

String one has 25 g on its mass hanger and is located at an angular position of 0. String two has 38 g of mass on the mass hanger and is located at an angular position of 180. Is there a third string...

-

How do people form impressions of what others are like and the causes of their behavior?

-

A package of Toys Galore Cereal is marked "Net Wt. 12 oz." The actual weight is normally distributed, with a mean of 12 \(\mathrm{oz}\) and a variance of 0.04 . a. What percent of the packages will...

-

What are the three steps in accounting for a business combination?

-

Name and describe several different types of graphs.

-

In Problems 23-26, suppose that people's heights (in centimeters) are normally distributed, with a mean of 170 and a standard deviation of 5. We find the heights of 50 people. a. How many would you...

-

Primary data is critical to any marketing endeavor. You will be learning how to create a survey, analyze results and make recommendations to the business owners. Scenario: Suppose you are the...

-

Marc Company assembles products from a group of interconnecting parts. The company produces some of the parts and buys some from outside vendors. The vendor for Part X has just increased its price by...

-

Using the data from BE11- 9, compute the depreciation expense for the first two years and determine the net book value at the end of the second year, assuming that Hermit Associates uses the double-...

-

Perfect Party Company contracts with a customer to provide its birth-day party package, including a its birth-day party package, including a cake, balloons, and musical entertainment. In addition,...

-

Centre Company provided the following listing of the current years post-closing account balances. Centre reported net income of $ 3,200 and declared dividends amounting to $ 600. Unrealized losses on...

-

Repeat Exercise 13.3, but this time work on the assumption that non-current assets that had originally cost :30,000, with accumulated depreciation of :12,000, had been sold during the year ended 31...

-

Study Figure 13.6. Write a short report on Bayers management of its cash flows over the period reported. Figure 13.6 Bayer Group's consolidated statement of cash flows Income after taxes Income taxes...

-

Expenses and revenues are subjective; cash flows are facts. Therefore cash flow statements cannot mislead. Discuss.

The Economics Of Imperfect Competition A Spatial Approach 1st Edition - ISBN: 0521315646 - Free Book

Study smarter with the SolutionInn App