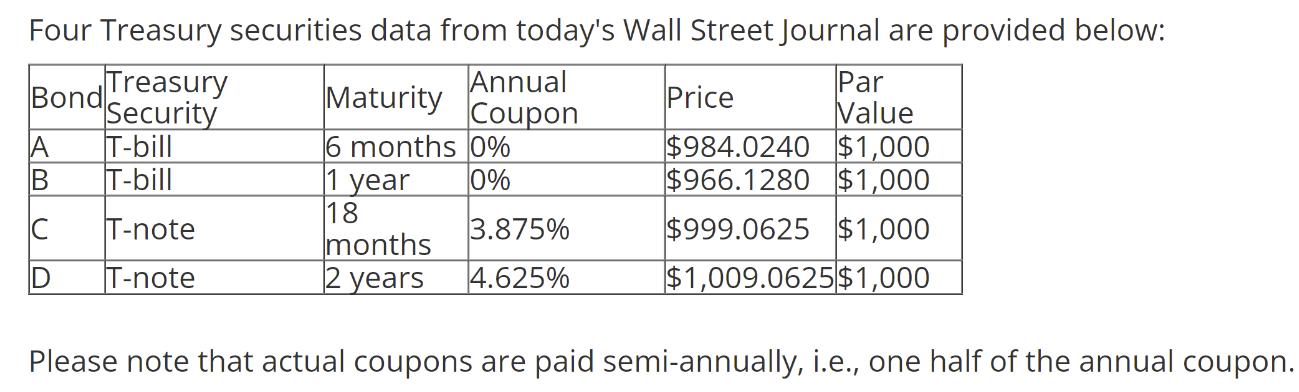

What are the zero prices for the 6-month, the 1-year, the 18-month, and the 2-year Treasury securities

Question:

What are the zero prices for the 6-month, the 1-year, the 18-month, and the 2-year Treasury securities above, respectively?

2. What is the 1-year forward rate beginning 6 months from today?

3. Given the zero prices obtained in (1) what should be the price of a 2-year T-note with 7.5% annual coupon (also paid semi-annually) with $1,000 par value per share?

4. Suppose the 2-year T-note with 7.5% annual coupon in (4) is currently traded at $1,010 per share for 10,000 shares in the market. How can you construct a risk-free arbitrage deal using all five Treasury securities above to lock in a positive profit today and zero obligations in the future? How much is the dollar profit in the deal?

Expert Answer:

1 Zero prices 6month Tbill 9840240 1year Tbill 9661280 18month Tnote 9990625 2year Tnote 10090625 2 ... View the full answer

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill