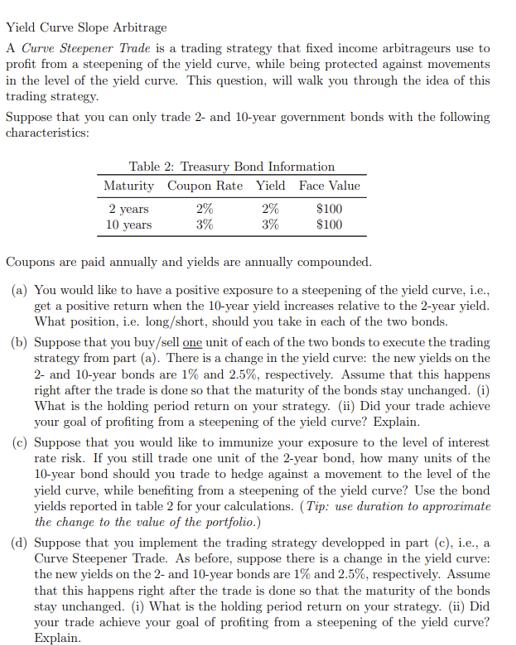

Yield Curve Slope Arbitrage A Curve Steepener Trade is a trading strategy that fixed income arbitrageurs...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

The image includes a description of a farming strategy referred to as Yield Curve Slope Arbitrage specifically a Curve Steepener Trade It provides data for two types of Treasury Bonds with 2year and 1... View the full answer

Related Book For

Microeconomics An Intuitive Approach with Calculus

ISBN: 978-0538453257

1st edition

Authors: Thomas Nechyba

Posted Date: