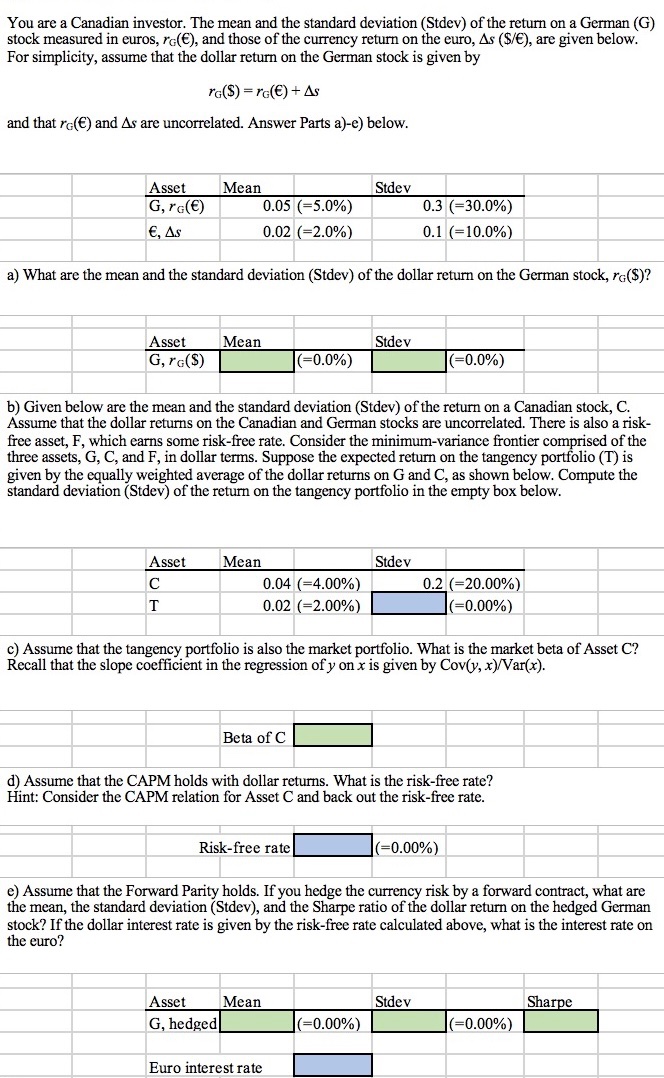

You are a Canadian investor. The mean and the standard deviation (Stdev) of the return on...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Lets solve each part step by step a The dollar return on the German stock r can be calculated using the given formula r rSr ASE From the table we have ... View the full answer

Related Book For

Investments

ISBN: 978-0071338875

8th Canadian Edition

Authors: Zvi Bodie, Alex Kane, Alan Marcus, Stylianos Perrakis, Peter

Posted Date: