You are a portfolio manager and you would like to hedge a portfolio daily over a thirty-day

Fantastic news! We've Found the answer you've been seeking!

Question:

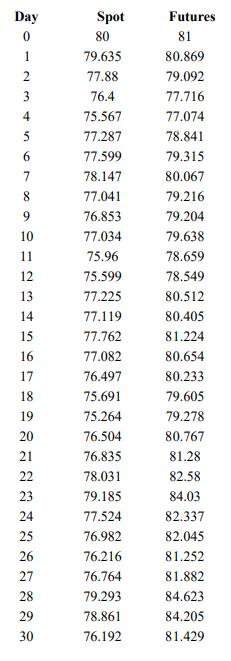

You are a portfolio manager and you would like to hedge a portfolio daily over a thirty-day horizon using futures. The table below provides data on the values of the spot portfolio and the futures that will be used as a hedging instrument:

a) Use the data to find the minimum variance hedge ratio you would use to achieve the hedge.

b) Using the hedge ratio from a., calculate the daily change in value of the hedged portfolio

c) What is the standard deviation of changes in value of the hedged portfolio? How does this compare to the standard deviation of changes in the unhedged spot position?

Expert Answer:

a To find the minimum variance hedge ratio we need to calculate the correlation coefficient between ... View the full answer

Related Book For

Financial Reporting and Analysis

ISBN: 978-0078025679

6th edition

Authors: Flawrence Revsine, Daniel Collins, Bruce, Mittelstaedt, Leon

Posted Date: