You are an Audit Supervisor of Taylor and Robert and the final audit of Derwent plc (Derwent)

Question:

You are an Audit Supervisor of Taylor and Robert and the final audit of Derwent plc (Derwent) for the year ended 30 June 2021 is due to commence shortly.

Derwent is a retailer offering food, clothing and homeware products to about 30 million customers every year across the United Kingdom. Derwent serves its customers through a channel network of 1,200 stores and online services.

The Company’s loss before tax per the draft financial statements for the year ended 30 June 2021 was £90.2m (2020: profit of £70.8m) and total assets as at that date were £2.2bn (2020: £3.1bn)

At a planning meeting held recently between the audit engagement team and the Finance Director of Derwent, you confirmed the following information obtained from Derwent’ accounting records and the notes to the draft financial statements:

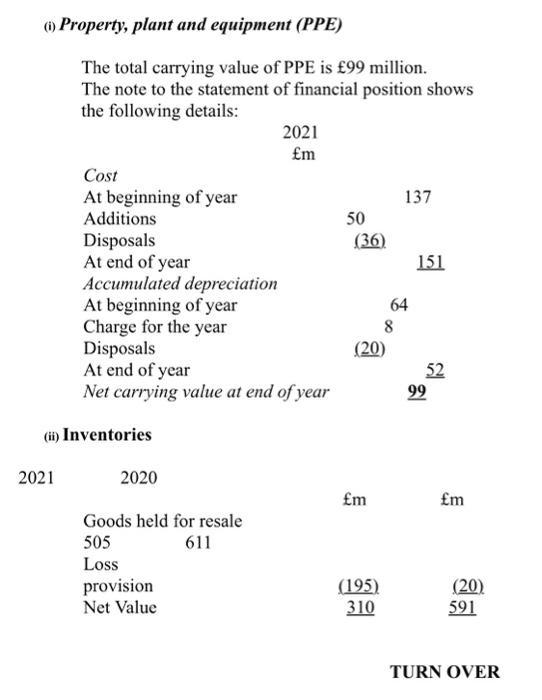

Inventories are valued on a weighted average cost basis and carried at the lower of cost and net realisable value. Cost includes all direct expenditure and other attributable costs incurred in bringing inventories to their present location and condition. All inventories are finished goods.

As a direct result of the restrictions on ‘non-essential’ trade imposed in response to the Covid-19 pandemic, Derwent’ ability to sell through existing Clothing & Homeware inventories has been significantly impacted and additional inventory loss provisioning has been made in respect of Clothing & Homeware.

When calculating inventory loss provision, the Directors considered the nature and condition of inventory, as well as applying assumptions around when trade restrictions might be eased leading to resumption of sales.

(iii) Trade payables and other liabilities

2021 2020

£m £m

Trade payables 276.0 273.5

Refund liabilities 2.4 6.2

Deferred revenue from sale of gift cards 10.2 60.8

Other creditors and accruals 120.4 180.3

409.0 520.8

Trade payables do not bear interest and are generally settled on 30-day terms. Other creditors and accruals also do not bear interest.

REQUIRED:

(a) Describe FOUR (4) substantive audit procedures you will perform in relation to the any TWO (2) elements of the property, plant and equipment note.

(b) Describe FOUR (4) substantive audit procedures you will perform in relation to the inventory balance.

(c) Describe SIX (6) audit procedures you will perform in relation to trade payables and other liabilities.

You should provide a minimum of one audit procedure for each item identified in the schedule of trade and other liabilities.

Expert Answer:

Auditing Cases An Interactive Learning Approach

ISBN: 978-0133852103

6th edition

Authors: Mark S. Beasley, Frank A. Buckless, Steven M. Glover, Douglas F. Prawitt