You are an equity portfolio manager who holds shares of Hi-Flier, Inc., which currently has a market

Fantastic news! We've Found the answer you've been seeking!

Question:

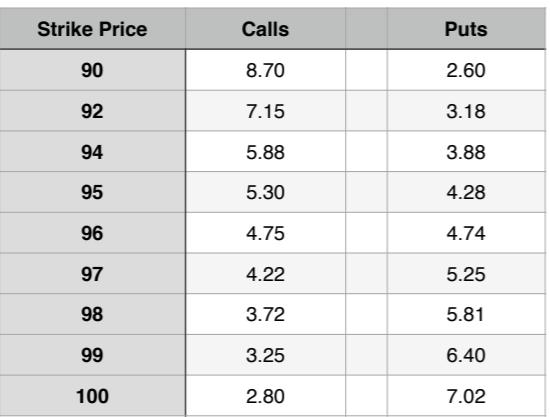

You are an equity portfolio manager who holds shares of Hi-Flier, Inc., which currently has a market price of $96/share. You are concerned the stock may fall over the next few months and you decide to examine 3-month put options on this stock. You observe the following prices: Draw a graph of the (i) the payout profile of the $98 strike put option at expiration and (ii) the approximate valuation curve this put option today. Identify the scale along the X-axis.

Draw a graph of the (i) the payout profile of the $98 strike put option at expiration and (ii) the approximate valuation curve this put option today. Identify the scale along the X-axis.

Expert Answer:

To draw the payout profile of the 98 strike put option at expiration we can create a simple profitlo... View the full answer

Related Book For

Posted Date: