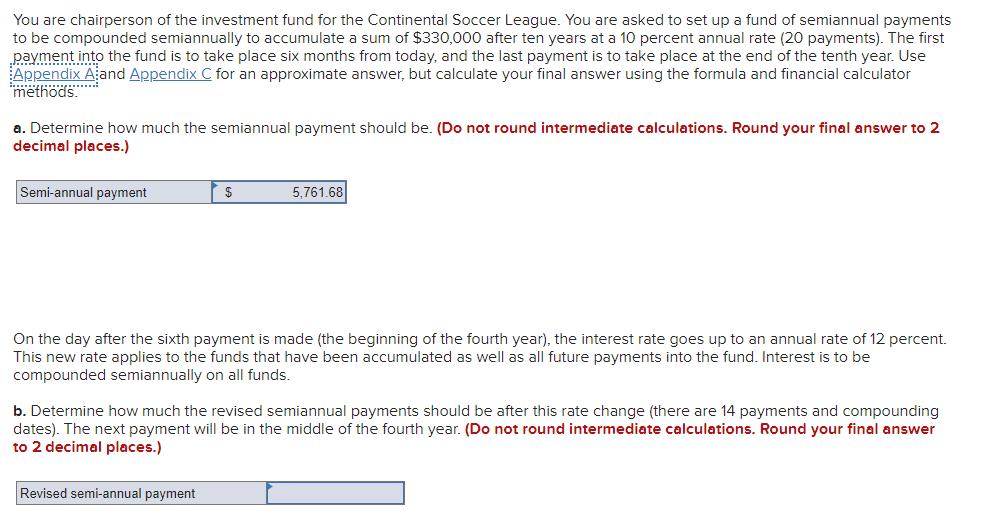

You are chairperson of the investment fund for the Continental Soccer League. You are asked to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

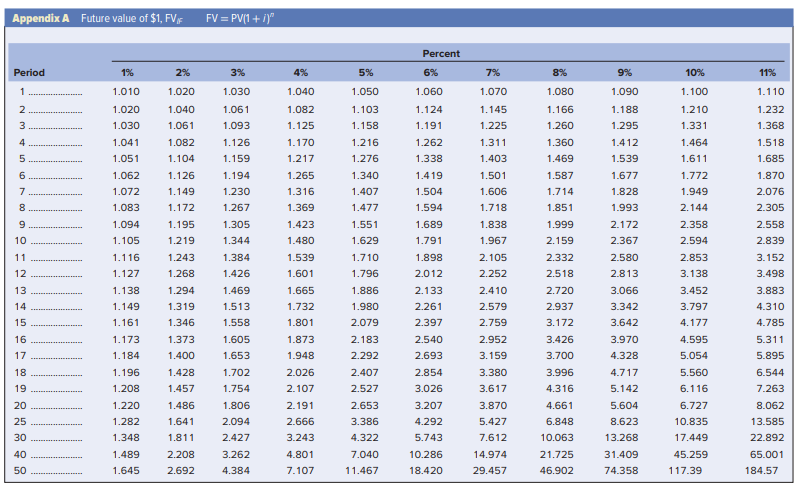

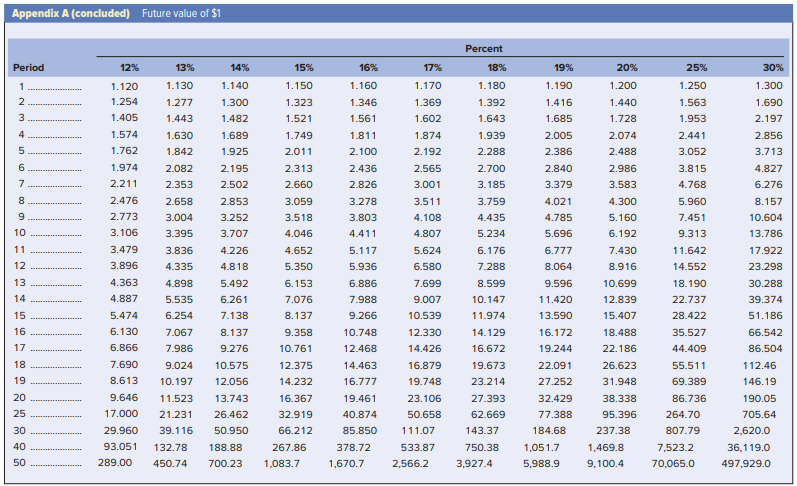

You are chairperson of the investment fund for the Continental Soccer League. You are asked to set up a fund of semiannual payments to be compounded semiannually to accumulate a sum of $330,000 after ten years at a 10 percent annual rate (20 payments). The first payment into the fund is to take place six months from today, and the last payment is to take place at the end of the tenth year. Use Appendix A and Appendix C for an approximate answer, but calculate your final answer using the formula and financial calculator methods. a. Determine how much the semiannual payment should be. (Do not round intermediate calculations. Round your final answer to 2 decimal places.) Semi-annual payment $ 5,761.68 On the day after the sixth payment is made (the beginning of the fourth year), the interest rate goes up to an annual rate of 12 percent. This new rate applies to the funds that have been accumulated as well as all future payments into the fund. Interest is to be compounded semiannually on all funds. b. Determine how much the revised semiannual payments should be after this rate change (there are 14 payments and compounding dates). The next payment will be in the middle of the fourth year. (Do not round intermediate calculations. Round your final answer to 2 decimal places.) Revised semi-annual payment Appendix A Future value of $1, FVF FV = PV(1+/)" Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 1 1.010 1.020 1.030 1.040 1.050 1.060 1.070 1.080 1.090 1.100 1.110 10 23 456 700 09 1.020 1.040 1.061 1.082 1.103 1.124 1.145 1.166 1.188 1.210 1.232 1.030 1.061 1.093 1.125 1.158 1.191 1.225 1.260 1.295 1.331 1.368 1.041 1.082 1.126 1.170 1.216 1.262 1.311 1.360 1.412 1.464 1.518 1.051 1.104 1.159 1.217 1.276 1.338 1.403 1.469 1.539 1.611 1.685 1.062 1.126 1.194 1.265 1.340 1.419 1.501 1.587 1.677 1.772 1.870 1.072 1.149 1.230 1.316 1.407 1.504 1.606 1.714 1.828 1.949 2.076 8 1.083 1.172 1.267 1.369 1.477 1.594 1.718 1.851 1.993 2.144 2.305 1.094 1.195 1.305 1.423 1.551 1.689 1.838 1.999 2.172 2.358 2.558 1.105 1.219 1.344 1.480 1.629 1.791 1.967 2.159 2.367 2.594 2.839 11 1.116 1.243 1.384 1.539 1.710 1.898 2.105 2.332 2.580 2.853 3.152 12 1.127 1.268 1.426 1.601 1.796 2.012 2.252 2.518 2.813 3.138 3.498 13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3.066 3.452 3.883 14 1.149 1.319 1.513 1.732 1.980 2.261 2.579 2.937 3.342 3.797 4.310 15 1.161 1.346 1.558 1.801 2.079 2.397 2.759 3.172 3.642 4.177 4.785 16 1.173 1.373 1.605 1.873 2.183 2.540 2.952 3.426 3.970 4.595 5.311 17 1.184 1.400 1.653 1.948 2.292 2.693 3.159 3.700 4.328 5.054 5.895 18 1.196 1.428 1.702 2.026 2.407 2.854 3.380 3.996 4.717 5.560 6.544 19 1.208 1.457 1.754 2.107 2.527 3.026 3.617 4.316 5.142 6.116 7.263 20 1.220 1.486 1.806 2.191 2.653 3.207 3.870 4.661 5.604 6.727 8.062 25 1.282 1.641 2.094 2.666 3.386 4.292 5.427 6.848 8.623 10.835 13.585 30 1.348 1.811 2.427 3.243 4.322 5.743 7.612 10.063 13.268 17.449 22.892 40 1.489 2.208 3.262 4.801 7.040 10.286 14.974 21.725 31.409 45.259 65.001 50 1.645 2.692 4.384 7.107 11.467 18.420 29.457 46.902 74.358 117.39 184.57 Appendix A (concluded) Future value of $1 Percent Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 1 1.120 1.130 1.140 1.150 1.160 1.170 1.180 1.190 1.200 1.250 1.300 2 3 4 5 6 7 8 9 1.254 1.277 1.300 1.323 1.346 1.369 1.392 1.416 1.440 1.563 1.690 1.405 1.443 1.482 1.521 1.561 1.602 1.643 1.685 1.728 1.953 2.197 1.574 1.630 1.689 1.749 1.811 1.874 1.939 2.005 2.074 2.441 2.856 1.762 1.842 1.925 2.011 2.100 2.192 2.288 2.386 2.488 3.052 3.713 1.974 2.082 2.195 2.313 2.436 2.565 2.700 2.840 2.986 3.815 4.827 2.211 2.353 2.502 2.660 2.826 3.001 3.185 3.379 3.583 4.768 6.276 2.476 2.658 2.853 3.059 3.278 3.511 3.759 4.021 4.300 5.960 8.157 2.773 3.004 3.252 3.518 3.803 4.108 4.435 4.785 5.160 7.451 10.604 10 3.106 3.395 3.707 4.046 4.411 4.807 5.234 5.696 6.192 9.313 13.786 11 3.479 3.836 4.226 4.652 5.117 5.624 6.176 6.777 7.430 11.642 17.922 12 3.896 4.335 4.818 5.350 5.936 6.580 7.288 8.064 8.916 14.552 23.298 13 4.363 4.898 5.492 6.153 6.886 7.699 8.599 9.596 10.699 18.190 30.288 14 4.887 5.535 6.261 7.076 7.988 9.007 10.147 11.420 12.839 22.737 39.374 15 5.474 6.254 7.138 8.137 9.266 10.539 11.974 13.590 15.407 28.422 51.186 16 6.130 7.067 8.137 9.358 10.748 12.330 14.129 16.172 18.488 35.527 66.542 17 6.866 7.986 9.276 10.761 12.468 14.426 16.672 19.244 22.186 44.409 86.504 18 7.690 9.024 10.575 12.375 14.463 16.879 19.673 22.091 26.623 55.511 112.46 19 8.613 10.197 12.056 14.232 16.777 19.748 23.214 27.252 31.948 69.389 146.19 UWNN 20 9.646 11.523 13.743 16.367 19.461 23.106 27.393 32.429 38.338 86.736 190.05 25 17.000 21.231 26.462 32.919 40.874 50.658 62.669 77.388 95.396 264.70 705.64 30 29.960 39.116 50.950 66.212 85.850 111.07 143.37 184.68 237.38 807.79 2,620.0 40 93.051 50 289.00 132.78 188.88 450.74 267.86 378.72 533.87 750.38 1,051.7 1,469.8 7,523.2 36,119.0 700.23 1,083.7 1,670.7 2,566.2 3,927.4 5,988.9 9,100.4 70,065.0 497,929.0 You are chairperson of the investment fund for the Continental Soccer League. You are asked to set up a fund of semiannual payments to be compounded semiannually to accumulate a sum of $330,000 after ten years at a 10 percent annual rate (20 payments). The first payment into the fund is to take place six months from today, and the last payment is to take place at the end of the tenth year. Use Appendix A and Appendix C for an approximate answer, but calculate your final answer using the formula and financial calculator methods. a. Determine how much the semiannual payment should be. (Do not round intermediate calculations. Round your final answer to 2 decimal places.) Semi-annual payment $ 5,761.68 On the day after the sixth payment is made (the beginning of the fourth year), the interest rate goes up to an annual rate of 12 percent. This new rate applies to the funds that have been accumulated as well as all future payments into the fund. Interest is to be compounded semiannually on all funds. b. Determine how much the revised semiannual payments should be after this rate change (there are 14 payments and compounding dates). The next payment will be in the middle of the fourth year. (Do not round intermediate calculations. Round your final answer to 2 decimal places.) Revised semi-annual payment Appendix A Future value of $1, FVF FV = PV(1+/)" Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 1 1.010 1.020 1.030 1.040 1.050 1.060 1.070 1.080 1.090 1.100 1.110 10 23 456 700 09 1.020 1.040 1.061 1.082 1.103 1.124 1.145 1.166 1.188 1.210 1.232 1.030 1.061 1.093 1.125 1.158 1.191 1.225 1.260 1.295 1.331 1.368 1.041 1.082 1.126 1.170 1.216 1.262 1.311 1.360 1.412 1.464 1.518 1.051 1.104 1.159 1.217 1.276 1.338 1.403 1.469 1.539 1.611 1.685 1.062 1.126 1.194 1.265 1.340 1.419 1.501 1.587 1.677 1.772 1.870 1.072 1.149 1.230 1.316 1.407 1.504 1.606 1.714 1.828 1.949 2.076 8 1.083 1.172 1.267 1.369 1.477 1.594 1.718 1.851 1.993 2.144 2.305 1.094 1.195 1.305 1.423 1.551 1.689 1.838 1.999 2.172 2.358 2.558 1.105 1.219 1.344 1.480 1.629 1.791 1.967 2.159 2.367 2.594 2.839 11 1.116 1.243 1.384 1.539 1.710 1.898 2.105 2.332 2.580 2.853 3.152 12 1.127 1.268 1.426 1.601 1.796 2.012 2.252 2.518 2.813 3.138 3.498 13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3.066 3.452 3.883 14 1.149 1.319 1.513 1.732 1.980 2.261 2.579 2.937 3.342 3.797 4.310 15 1.161 1.346 1.558 1.801 2.079 2.397 2.759 3.172 3.642 4.177 4.785 16 1.173 1.373 1.605 1.873 2.183 2.540 2.952 3.426 3.970 4.595 5.311 17 1.184 1.400 1.653 1.948 2.292 2.693 3.159 3.700 4.328 5.054 5.895 18 1.196 1.428 1.702 2.026 2.407 2.854 3.380 3.996 4.717 5.560 6.544 19 1.208 1.457 1.754 2.107 2.527 3.026 3.617 4.316 5.142 6.116 7.263 20 1.220 1.486 1.806 2.191 2.653 3.207 3.870 4.661 5.604 6.727 8.062 25 1.282 1.641 2.094 2.666 3.386 4.292 5.427 6.848 8.623 10.835 13.585 30 1.348 1.811 2.427 3.243 4.322 5.743 7.612 10.063 13.268 17.449 22.892 40 1.489 2.208 3.262 4.801 7.040 10.286 14.974 21.725 31.409 45.259 65.001 50 1.645 2.692 4.384 7.107 11.467 18.420 29.457 46.902 74.358 117.39 184.57 Appendix A (concluded) Future value of $1 Percent Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 1 1.120 1.130 1.140 1.150 1.160 1.170 1.180 1.190 1.200 1.250 1.300 2 3 4 5 6 7 8 9 1.254 1.277 1.300 1.323 1.346 1.369 1.392 1.416 1.440 1.563 1.690 1.405 1.443 1.482 1.521 1.561 1.602 1.643 1.685 1.728 1.953 2.197 1.574 1.630 1.689 1.749 1.811 1.874 1.939 2.005 2.074 2.441 2.856 1.762 1.842 1.925 2.011 2.100 2.192 2.288 2.386 2.488 3.052 3.713 1.974 2.082 2.195 2.313 2.436 2.565 2.700 2.840 2.986 3.815 4.827 2.211 2.353 2.502 2.660 2.826 3.001 3.185 3.379 3.583 4.768 6.276 2.476 2.658 2.853 3.059 3.278 3.511 3.759 4.021 4.300 5.960 8.157 2.773 3.004 3.252 3.518 3.803 4.108 4.435 4.785 5.160 7.451 10.604 10 3.106 3.395 3.707 4.046 4.411 4.807 5.234 5.696 6.192 9.313 13.786 11 3.479 3.836 4.226 4.652 5.117 5.624 6.176 6.777 7.430 11.642 17.922 12 3.896 4.335 4.818 5.350 5.936 6.580 7.288 8.064 8.916 14.552 23.298 13 4.363 4.898 5.492 6.153 6.886 7.699 8.599 9.596 10.699 18.190 30.288 14 4.887 5.535 6.261 7.076 7.988 9.007 10.147 11.420 12.839 22.737 39.374 15 5.474 6.254 7.138 8.137 9.266 10.539 11.974 13.590 15.407 28.422 51.186 16 6.130 7.067 8.137 9.358 10.748 12.330 14.129 16.172 18.488 35.527 66.542 17 6.866 7.986 9.276 10.761 12.468 14.426 16.672 19.244 22.186 44.409 86.504 18 7.690 9.024 10.575 12.375 14.463 16.879 19.673 22.091 26.623 55.511 112.46 19 8.613 10.197 12.056 14.232 16.777 19.748 23.214 27.252 31.948 69.389 146.19 UWNN 20 9.646 11.523 13.743 16.367 19.461 23.106 27.393 32.429 38.338 86.736 190.05 25 17.000 21.231 26.462 32.919 40.874 50.658 62.669 77.388 95.396 264.70 705.64 30 29.960 39.116 50.950 66.212 85.850 111.07 143.37 184.68 237.38 807.79 2,620.0 40 93.051 50 289.00 132.78 188.88 450.74 267.86 378.72 533.87 750.38 1,051.7 1,469.8 7,523.2 36,119.0 700.23 1,083.7 1,670.7 2,566.2 3,927.4 5,988.9 9,100.4 70,065.0 497,929.0

Expert Answer:

Related Book For

Foundations of Financial Management

ISBN: 978-1259194078

15th edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

Posted Date:

Students also viewed these finance questions

-

On November 1, 2012, Galaxy Philippines took delivery from a Thailand firm of inventory costing 225,000 baht. Payment is due on January 30, 2013. Concurrently, Galaxy Philippines paid 2,025 cash to...

-

You are chairperson of the investment fund for the Continental Soccer League. You are asked to set up a fund of semiannual payments to be compounded semiannually to accumulate a sum of $230,000 after...

-

You are chairperson of the investment fund for the Continental Soccer League. You are asked to set up a fund of semiannual payments to be compounded semiannually to accumulate a sum of $250,000 after...

-

Consider the following. (a) Find aw s aw at (b) Find aw s w at w = x cos(yz), x = s, y = t, z =s - 2t aw aw by using the appropriate Chain Rule. (Enter your answers in terms of s and t.) s at aw s...

-

No Leak Plumbing and Repair provides customers with firm quotes for a plumbing repair job before actually starting the job. To be able to do this, No Leak has been very careful to maintain time...

-

Let A be as in Exercise 9. Use the inverse power method with x0 = (1, 0, 0) to estimate the eigenvalue of A near a = - 1.4, with an accuracy to four decimal places.

-

Stan LaRue is attempting to outline the important points about overhead variances on a class examination. List four points that Stan should include in his outline.

-

Herbal Resources is a small but profitable producer of dietary supplements for pets. This is not a high-tech business, but Herbals earnings have averaged around $1.2 million after tax, largely on the...

-

If QT = 2b and ST = b + 17, find the value of b that makes quadrilateral PQRS a parallelogram. S b = P R Q T

-

4. What is the net present value of the following stream of cash flows assuming the opportunity cost rate is 12%? Solve NPV using each cash flow and the NPV function in Excel (use basic PV/FV...

-

How does the process of socialization contribute to identity formation, and what is the role of various agents of socialization (such as family, education, and media) in reinforcing or challenging...

-

How do contemporary understandings of race and ethnicity inform institutional practices, and to what extent do these constructs perpetuate structural discrimination within societies ?

-

In an informed search algorithm, the heuristic function h(n) is a (not necessarily accurate) heuristic estimate of the cost of the path from n to its nearest goal node, which have non-zero positive...

-

You are considering an investment in either individual stocks or a portfolio of stocks. The two stocks you are researching, Stock A and Stock B, have the following historical returns: Year FA FB 2017...

-

Morganton Company makes one product and it provided the following information to help prepare the master budget: The budgeted selling price per unit is $90. Budgeted unit sales for June, July,...

-

Internal Rate of Return Method The internal rate of return method is used by King Bros. Construction Co. in analyzing a capital expenditure proposal that involves an Investment of $90,668 and annual...

-

Read Case Study Google: Dont Be Evil Unless and answer the following: Why do you think Google was adamant about not wanting to supply information requested by the government concerning the Child...

-

What role does growth-need strength play in the job characteristics model?

-

Explain the difference between halo errors and recency errors in performance appraisal.

-

When is a team effective?

Study smarter with the SolutionInn App