You are given the following facts in respect of an individual taxpayer's 2022/23 income year: Assume that

Question:

You are given the following facts in respect of an individual taxpayer's 2022/23 income year: Assume that the individual has already derived residential rental income of $50,000 and paid PAYG instalments of $10,000. Also assume that the individual has private health insurance with hospital cover.

Sale of a painting, displayed in the family residence, for consideration of $43,000 on 10 October 2022. It had been acquired on 30 November 2021 at a cost of $21,500.

Sale of a TV set for $350 in May 2023. It had been bought for $1,500 in August 2016 and used solely in the family home.

Sale of a residential rental property for $175,000 in April 2023, with agent's fees of $3,250 incurred at the time of sale. The property had been purchased with the intention of deriving income from renting it in November 2002 at a total cost of $129,000, including valuation fees of $1,200 and stamp duty of $4,100. Furthermore, the taxpayer had spent $20,000 in upgrading the kitchen and laundry in May 2003.

In addition, the taxpayer had made a capital loss of $3,500 on the sale of shares in November 2019. He had no other capital transactions for that year and no net capital loss carried forward from any earlier year.

Required:

Calculate the taxpayer's taxable income and tax payable (including the rent income) in respect of the year ended 30 June 2023. The taxpayer is not registered for the goods and services tax. Please use relevant tax rates and Medicare levy to calculate final tax payable. Details are provided below. Cite and apply all relevant sections from the 1997 Act to support your calculation.

What would be the taxpayer's net capital gain if there were no paintings?

What would be the taxpayer's net capital gain if there were no rental property?

What would be the taxpayer's net capital gain if the capital loss were $25,000?

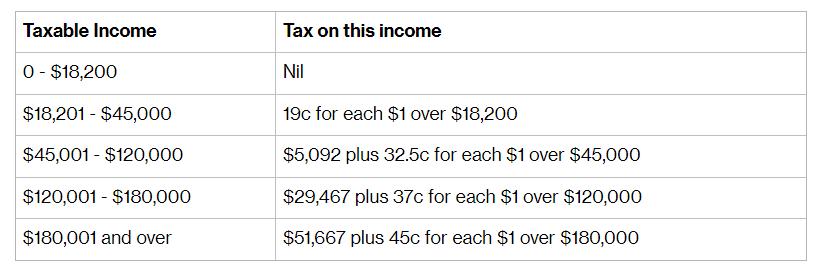

2023 Resident Individual Tax Rates

These rates do not include Medicare levy of 2% for individual taxpayers or Medicare levy Surcharge of 1.5% (if applicable).

Medicare levy surcharge is not payable when the taxpayer has private health insurance with hospital coverage.

Expert Answer:

SOLUTION To calculate the taxpayers taxable income and tax payable for the year ended June 30 2023 we need to consider the various income and deductions based on the given information Lets calculate t... View the full answer

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill