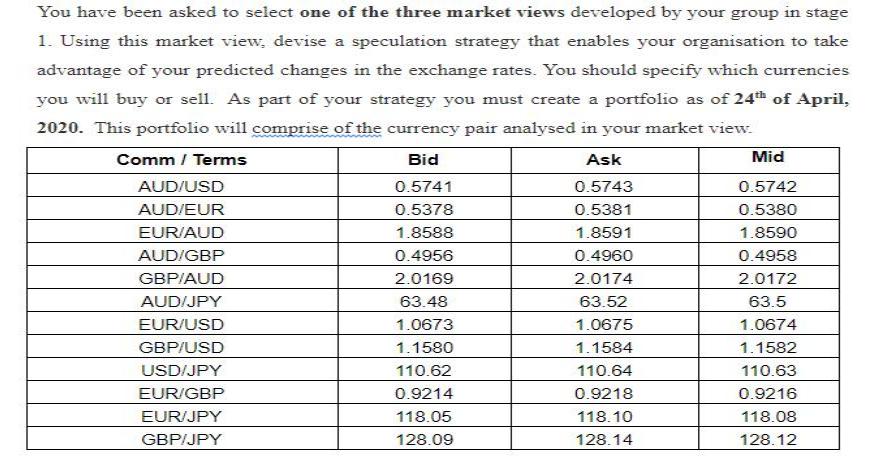

You have been asked to select one of the three market views developed by your group...

Fantastic news! We've Found the answer you've been seeking!

Question:

![Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a ge](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2021/05/60954f279ad38_1620397862664.jpg)

Transcribed Image Text:

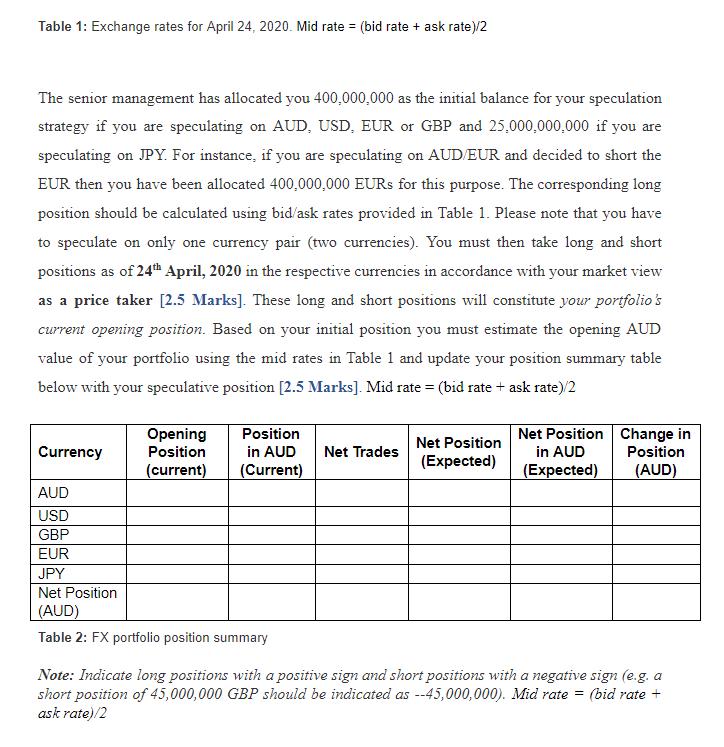

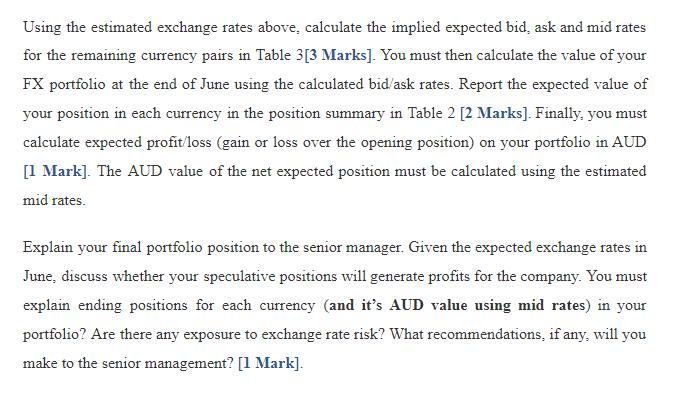

You have been asked to select one of the three market views developed by your group in stage 1. Using this market view, devise a speculation strategy that enables your organisation to take advantage of your predicted changes in the exchange rates. You should specify which currencies you will buy or sell. As part of your strategy you must create a portfolio as of 24th of April, 2020. This portfolio will comprise of the currency pair analysed in your market view. Comm / Terms Bid Ask Mid AUD/USD 0.5741 0.5743 0.5742 AUD/EUR 0.5378 0.5381 0.5380 EUR/AUD 1.8588 1.8591 1.8590 AUD/GBP 0.4956 0.4960 0.4958 GBP/AUD 2.0169 2.0174 2.0172 AUD/JPY 63.48 63.52 63.5 EUR/USD 1.0673 1.0675 1.0674 GBP/USD 1.1580 1.1584 1.1582 USD/JPY 110.62 110.64 110.63 EUR/GBP 0.9214 0.9218 0.9216 EUR/JPY 118.05 118.10 118.08 GBP/JPY 128.09 128.14 128.12 Table 1: Exchange rates for April 24, 2020. Mid rate = (bid rate + ask rate)/2 The senior management has allocated you 400,000,000 as the initial balance for your speculation strategy if you are speculating on AUD, USD, EUR or GBP and 25,000,000,000 if you are speculating on JPY. For instance, if you are speculating on AUD/EUR and decided to short the EUR then you have been allocated 400,000,000 EURS for this purpose. The corresponding long position should be calculated using bid/ask rates provided in Table 1. Please note that you have to speculate on only one currency pair (two currencies). You must then take long and short positions as of 24h April, 2020 in the respective currencies in accordance with your market view as a price taker [2.5 Marks]. These long and short positions will constitute your portfolio's current opening position. Based on your initial position you must estimate the opening AUD value of your portfolio using the mid rates in Table 1 and update your position summary table below with your speculative position [2.5 Marks]. Mid rate = (bid rate + ask rate)/2 Position in AUD (Current) Net Position Change in in AUD (Expected) Opening Net Position Currency Position Net Trades Position (Expected) (current) (AUD) AUD USD GBP EUR JPY Net Position (AUD) Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For BAFI1002 Financial Markets – Group FX Assignment (Stage 2) this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP GBP/AUD 2.0291 2.0298 2.0295 AUDIJPY EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP EURIJPY GBP/JPY Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit'loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark]. You have been asked to select one of the three market views developed by your group in stage 1. Using this market view, devise a speculation strategy that enables your organisation to take advantage of your predicted changes in the exchange rates. You should specify which currencies you will buy or sell. As part of your strategy you must create a portfolio as of 24th of April, 2020. This portfolio will comprise of the currency pair analysed in your market view. Comm / Terms Bid Ask Mid AUD/USD 0.5741 0.5743 0.5742 AUD/EUR 0.5378 0.5381 0.5380 EUR/AUD 1.8588 1.8591 1.8590 AUD/GBP 0.4956 0.4960 0.4958 GBP/AUD 2.0169 2.0174 2.0172 AUD/JPY 63.48 63.52 63.5 EUR/USD 1.0673 1.0675 1.0674 GBP/USD 1.1580 1.1584 1.1582 USD/JPY 110.62 110.64 110.63 EUR/GBP 0.9214 0.9218 0.9216 EUR/JPY 118.05 118.10 118.08 GBP/JPY 128.09 128.14 128.12 Table 1: Exchange rates for April 24, 2020. Mid rate = (bid rate + ask rate)/2 The senior management has allocated you 400,000,000 as the initial balance for your speculation strategy if you are speculating on AUD, USD, EUR or GBP and 25,000,000,000 if you are speculating on JPY. For instance, if you are speculating on AUD/EUR and decided to short the EUR then you have been allocated 400,000,000 EURS for this purpose. The corresponding long position should be calculated using bid/ask rates provided in Table 1. Please note that you have to speculate on only one currency pair (two currencies). You must then take long and short positions as of 24h April, 2020 in the respective currencies in accordance with your market view as a price taker [2.5 Marks]. These long and short positions will constitute your portfolio's current opening position. Based on your initial position you must estimate the opening AUD value of your portfolio using the mid rates in Table 1 and update your position summary table below with your speculative position [2.5 Marks]. Mid rate = (bid rate + ask rate)/2 Position in AUD (Current) Net Position Change in in AUD (Expected) Opening Net Position Currency Position Net Trades Position (Expected) (current) (AUD) AUD USD GBP EUR JPY Net Position (AUD) Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For BAFI1002 Financial Markets – Group FX Assignment (Stage 2) this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP GBP/AUD 2.0291 2.0298 2.0295 AUDIJPY EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP EURIJPY GBP/JPY Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit'loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark].

Expert Answer:

Related Book For

Organizational Behavior

ISBN: 978-0077862589

7th edition

Authors: Steven McShane, Mary Ann Von Glinow

Posted Date:

Students also viewed these accounting questions

-

As a junior congressperson you have been asked to help promote a bill to allow casino gambling in your state. There is much opposition to this bill. Using distributive bargaining, discuss the pros...

-

You have been asked to evaluate possible sites for an Asian production facility that will manufacture your firms products and sell them to the Asian market. What real exchange rate considerations...

-

As a securities analyst you have been asked to review a valuation of a closely held business, Wigwam Autoparts Heaven, Inc. (WAH), prepared by the Red Rocks Group (RRG). You are to give an opinion on...

-

Consider two industries in which firms hold the following market shares: Industry A: 25%, 20%, 18%, 15%, 8%, 7%, 4%, 2%, 1% Industry B: 30%, 10%, 9%, 8%, 8%, 8%, 8%, 6%, 6%, 5%, 2% What are the...

-

Consider the horizontal box plot shown below. a. What is the median of the data set (approximately)? b. What are the upper and lower quartiles of the data set (approximately)? c. What is the...

-

Defermine the dimensions of the spotted structural member as ' Q 1 " , which may be considered as a console bearn, using first. pniciples of "Strength of Mateniais" ( that is , \ sigma max < = \...

-

Why are information security and privacy important considerations in the design, development, and maintenance of an HRIS?

-

An online survey asked 1,004 adults "If purchasing a used car made certain upgrades or features more affordable, what would be your preferred luxury upgrade?" The results indicated that 9% of the...

-

Mega Corp., a semiweekly depositor, incurs a deposit liability on Wednesday, March 3 1 , of $ 9 9 , 0 0 0 . On Thursday, April 1 , it incurs an additional liability of $ 5 , 0 0 0 . When are these...

-

Consider the following parlor game to be played between two players. Each player begins with three chips: one red, one white, and one blue. Each chip can be used only once. To begin, each player...

-

Company A has agreed to supply the following quantities of spe- cial lamps to Company B during the next 4 months: Month January February 150 Units 160 March April 225 180 Company A can produce a...

-

Complete the following single replacement or substitution reaction to notathglov J. B. F. C. J For the following mentioned reactions, identified by their letters from this worksheet, write a net...

-

Decide what kind of crystalline solid each element or compound in the table forms, Then, rank the solids in order of decreasing melting point. That is, select "1" next highest melting point, and so...

-

1st choice vapor pressure 2nd choice boiling point 3rd choice freezing point decreases because rate of condensation increases for a solution relative to a pure solvent increases because vapor...

-

Prepare a schematic Brouwer diagram for NiO indicating: (i) (ii) the intrinsic defects under ambient conditions. the intrinsic defects under reducing conditions. (iii) the intrinsic defects under...

-

How many L of hydrogen gas (H) will be produced along with 27.5 L of O, according to the following reaction? +_ _H(g) + ___O(g) _HO(g) ___H(g) 1) 18.3 2) 55.0 L 3) 27.5 L 4) 13.8 L

-

Question 4 - Critical Mach Number Estimation (8 Points): The incompressible Cp distribution of an airfoil at a given angle of attack has been determined based on wind tunnel testing. The data is...

-

Swifty company is a publicly held corporation whose $1 par value stock is actively traded at $30 per share. The company issued 3400 shares of stock to acquire land recently advertised at $93000. When...

-

The organization for which you have been working for five years is suffering from a global recession. In response, it changes your compensation structure. Discuss the role of moral intensity, moral...

-

A federal government department has high levels of absenteeism among the office staff. The head of office administration argues that employees are misusing the company's sick leave benefits. However,...

-

How have the division and coordination of labor evolved at Merritt's Bakery from its beginnings to today?

-

A diploid organism has a total of 14 chromosomes and about 20,000 genes per haploid genome. Approximately how many genes are in each linkage group?

-

By conducting testcrosses, researchers have found that the sweet pea plant has seven linkage groups. How many chromosomes would you expect to find in leaf cells of sweet pea plants?

-

Describe the unique features of ascomycetes that facilitate genetic analysis of these fungi.

Study smarter with the SolutionInn App