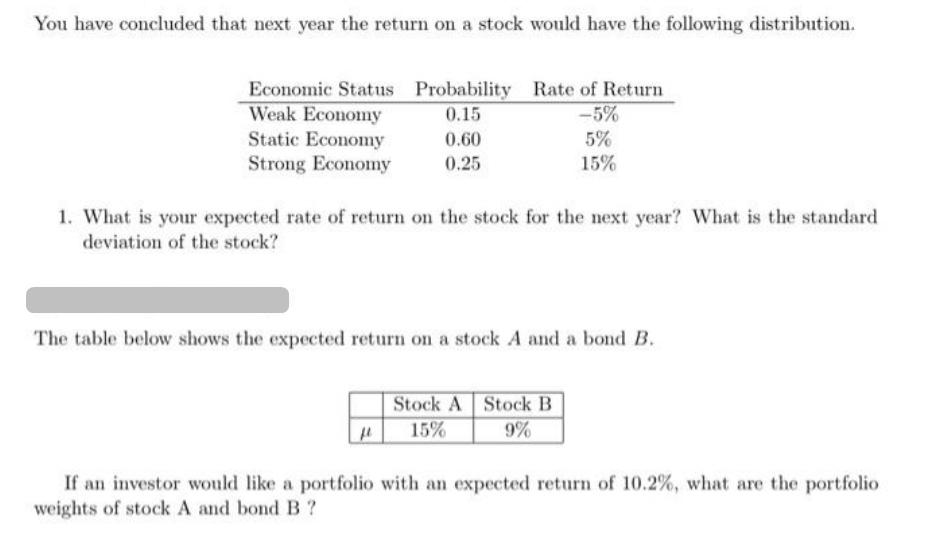

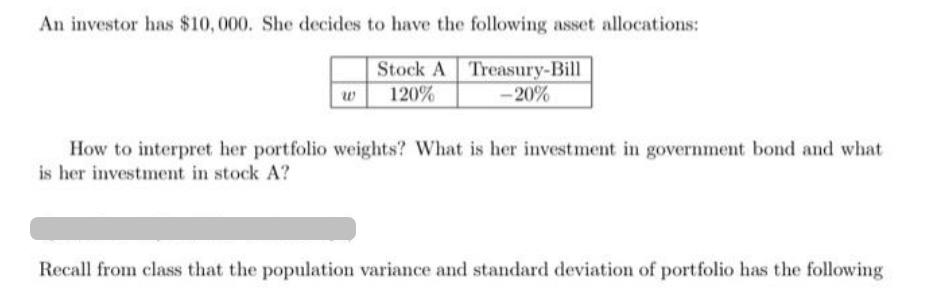

You have concluded that next year the return on a stock would have the following distribution....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

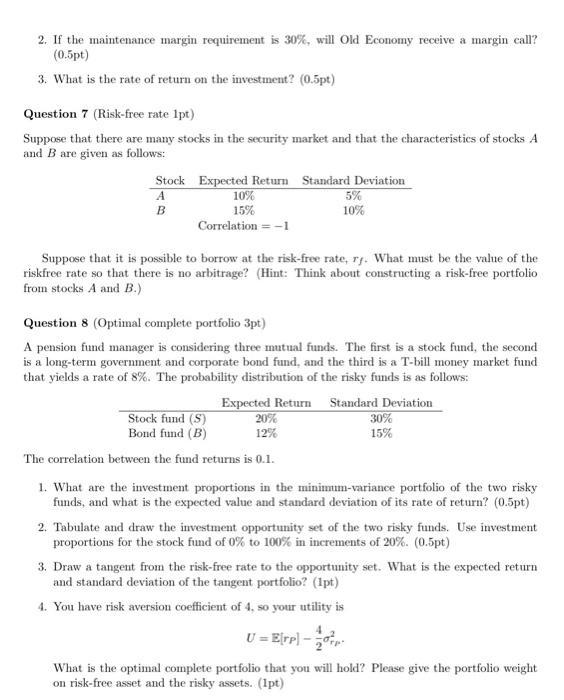

You have concluded that next year the return on a stock would have the following distribution. Economic Status Probability Weak Economy 0.15 Static Economy Strong Economy 0.60 0.25 Rate of Return -5% 5% 15% 1. What is your expected rate of return on the stock for the next year? What is the standard deviation of the stock? f The table below shows the expected return on a stock A and a bond B. Stock A Stock B 9% 15% If an investor would like a portfolio with an expected return of 10.2%, what are the portfolio weights of stock A and bond B? An investor has $10,000. She decides to have the following asset allocations: Stock A Treasury-Bill -20% 120% w How to interpret her portfolio weights? What is her investment in government bond and what is her investment in stock A? Recall from class that the population variance and standard deviation of portfolio has the following formulas. With two assets A and B: If the portfolio weight on asset A is and the the portfolio weight on asset B w, then =A+B Var(r) (u) Var(-) + () Var() + Cov(r) + ww Cov(r). With more than two assets: If the portfolio weight on asset i is a, and asset i has return r, then i=1 NN Var()-(w) Var(r) + u'w Cour.r) i=1 Suppose that an investor holds a portfolio of bonds X,Y and Z. Portfolio weights of the three assets are 20%, 50% and 30%, respectively. The table below shows the variance-covariance matrix of the three assets. What is the standard deviation of the portfolio? X Z X 0.0200 0.0150 0.0350 Y 0.0150 0.0500 0.0250 0.0350 0.0250 0.0100 Z Question 5 (AMR and GMR 0.5pt) The table below shows annual holding period returns on a stock over five years. What are the arithmetic and geometric means (AMR and GMR) of the stock's returns? Year HPR 1 10% 2 12% 8% 2% -3% 3 4 5 Question 6 (Margin trade 3pt) Old Economy Traders opened an account to short sell 1,000 shares of Internet Dreams from the previous problem. After borrowing the shares of Internet Dreams, Old Economy Traders immedi- ately sells the shares in the market at $60. After the sale of the shares, Old Economy Traders will not receive the dividend from the company. The initial margin requirement was 50%. (The margin account pays no interest.) A year later, the price of Internet Dreams has fallen from 860 to $50, and the stock paid a divide per share in between. 1. What is the remaining margin in the account? (2pt) 82 2. If the maintenance margin requirement is 30%, will Old Economy receive a margin call? (0.5pt) 3. What is the rate of return on the investment? (0.5pt) Question 7 (Risk-free rate 1pt) Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock Expected Return Standard Deviation 5% A 10% B 15% 10% Correlation = -1 Suppose that it is possible to borrow at the risk-free rate, ry. What must be the value of the riskfree rate so that there is no arbitrage? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) Question 8 (Optimal complete portfolio 3pt) A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation 20% 12% Stock fund (S) Bond fund (B) The correlation between the fund returns is 0.1. 30% 15% 1. What are the investment proportions in the minimum-variance portfolio of the two risky funds, and what is the expected value and standard deviation of its rate of return? (0.5pt) 2. Tabulate and draw the investment opportunity set of the two risky funds. Use investment proportions for the stock fund of 0% to 100% in increments of 20%. (0.5pt) 3. Draw a tangent from the risk-free rate to the opportunity set. What is the expected return and standard deviation of the tangent portfolio? (1pt) 4. You have risk aversion coefficient of 4, so your utility is U = Erp) - What is the optimal complete portfolio that you will hold? Please give the portfolio weight on risk-free asset and the risky assets. (1pt) You have concluded that next year the return on a stock would have the following distribution. Economic Status Probability Weak Economy 0.15 Static Economy Strong Economy 0.60 0.25 Rate of Return -5% 5% 15% 1. What is your expected rate of return on the stock for the next year? What is the standard deviation of the stock? f The table below shows the expected return on a stock A and a bond B. Stock A Stock B 9% 15% If an investor would like a portfolio with an expected return of 10.2%, what are the portfolio weights of stock A and bond B? An investor has $10,000. She decides to have the following asset allocations: Stock A Treasury-Bill -20% 120% w How to interpret her portfolio weights? What is her investment in government bond and what is her investment in stock A? Recall from class that the population variance and standard deviation of portfolio has the following formulas. With two assets A and B: If the portfolio weight on asset A is and the the portfolio weight on asset B w, then =A+B Var(r) (u) Var(-) + () Var() + Cov(r) + ww Cov(r). With more than two assets: If the portfolio weight on asset i is a, and asset i has return r, then i=1 NN Var()-(w) Var(r) + u'w Cour.r) i=1 Suppose that an investor holds a portfolio of bonds X,Y and Z. Portfolio weights of the three assets are 20%, 50% and 30%, respectively. The table below shows the variance-covariance matrix of the three assets. What is the standard deviation of the portfolio? X Z X 0.0200 0.0150 0.0350 Y 0.0150 0.0500 0.0250 0.0350 0.0250 0.0100 Z Question 5 (AMR and GMR 0.5pt) The table below shows annual holding period returns on a stock over five years. What are the arithmetic and geometric means (AMR and GMR) of the stock's returns? Year HPR 1 10% 2 12% 8% 2% -3% 3 4 5 Question 6 (Margin trade 3pt) Old Economy Traders opened an account to short sell 1,000 shares of Internet Dreams from the previous problem. After borrowing the shares of Internet Dreams, Old Economy Traders immedi- ately sells the shares in the market at $60. After the sale of the shares, Old Economy Traders will not receive the dividend from the company. The initial margin requirement was 50%. (The margin account pays no interest.) A year later, the price of Internet Dreams has fallen from 860 to $50, and the stock paid a divide per share in between. 1. What is the remaining margin in the account? (2pt) 82 2. If the maintenance margin requirement is 30%, will Old Economy receive a margin call? (0.5pt) 3. What is the rate of return on the investment? (0.5pt) Question 7 (Risk-free rate 1pt) Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock Expected Return Standard Deviation 5% A 10% B 15% 10% Correlation = -1 Suppose that it is possible to borrow at the risk-free rate, ry. What must be the value of the riskfree rate so that there is no arbitrage? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) Question 8 (Optimal complete portfolio 3pt) A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation 20% 12% Stock fund (S) Bond fund (B) The correlation between the fund returns is 0.1. 30% 15% 1. What are the investment proportions in the minimum-variance portfolio of the two risky funds, and what is the expected value and standard deviation of its rate of return? (0.5pt) 2. Tabulate and draw the investment opportunity set of the two risky funds. Use investment proportions for the stock fund of 0% to 100% in increments of 20%. (0.5pt) 3. Draw a tangent from the risk-free rate to the opportunity set. What is the expected return and standard deviation of the tangent portfolio? (1pt) 4. You have risk aversion coefficient of 4, so your utility is U = Erp) - What is the optimal complete portfolio that you will hold? Please give the portfolio weight on risk-free asset and the risky assets. (1pt)

Expert Answer:

Answer rating: 100% (QA)

To calculate the expected rate of return on the stock for the next year we can multiply the probabil... View the full answer

Related Book For

Understanding Basic Statistics

ISBN: 9781111827021

6th Edition

Authors: Charles Henry Brase, Corrinne Pellillo Brase

Posted Date:

Students also viewed these finance questions

-

The operations vice president of Security Home Bank has been interested in investigating the efficiency of the bank s operations. She has been particularly concerned about the costs of handling...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Repeat Prob. 37 using singularity functions exclusively (including reactions). Repeat Prob. 37, For the beam shown, find the reactions at the supports and plot the shear-force and bending-moment...

-

Can there be an effective EU leader? Is this a realistic prospect? Discuss the factors involved with this concept. What role has the financial crisis in the Euro zone played in this concept?

-

Listed below are eight events or transactions of Lone Star Corporation. a. Made an adjusting entry to record interest on a short-term note payable. b. Made a monthly installment payment of a fully...

-

Do larger butterflies live longer? The wingspan (in millimeters) and the lifespan in the adult state (in days) were measured for 22 species of butterfly. Following are the results. a. Compute the...

-

Consider the situation of La Nacin, a hypothetical Latin American country. In 2010, La Nacin was a net debtor to the rest of the world. Assume that all of La Nacins foreign debt was dollar...

-

discuss how understanding the influences on an operational environment (OE) affect the Army's ability to conductLarge Scale Combat Operations(LSCO)?

-

You want to purchase a home based upon your current salary you decide that you can afford $2000.00 per month. Your bank has approved you for a (30 year) loan at an interest rate of 5%. 1) Based upon...

-

Given the circuit shown in the following figure, and based on the 180 nm TSMC Technology, assume that the supply voltage (VDD) is 1.8V, and the length of each transistor (n-type MOSFET) is fixed at L...

-

2. Based on the Howe roof truss illustrated below, a) draw the free body diagram of the structure. b) calculate the force CD. c) determine the force in member DJ of the structure. 10 kN L 10 kN R KI...

-

A new company issues $30 Million Dollars of 12-year bonds bearing a 9.5% Coupon. If the market demands a 7.0% rate of return for the risk it believes it is taking, how much will the company receive...

-

Two opticians compete on price in the town. The marginal cost for a pair of glasses c = $10 and demand in the town is Q = 100 P per day in April. Assume first that both have a capacity to complete...

-

The price the investors are willing to pay for a share of Bouchard Company's stock is $20. Investors expect its dividends to grow at a constant rate, 6%, forever. The stock's beta is 1.3, the market...

-

What emergency legislation was created by Canadian Prime Minister Trudeau to combat terrorism?

-

A student multiplied incorrectly as follows (x+2)=x+4) What went wrong? Give the correct product.

-

Prove that if Σ an is absolutely convergent, then a. an

-

Let z be a random variable with a standard normal distribution. Find the indicated probability and shade the corresponding area under the standard normal curve. P(z 2.15)

-

Redo Problem 8 using the critical region method, and compare your results to those obtained using the P-value method. Problem 8 Would you favor spending more federal tax money on the arts? This...

-

Are Americas top chief executive officers (CEOs) really worth all that money? One way to answer this question is to look at row B, the annual company percentage increase in revenue, versus row A, the...

-

State which of the following items could appear as an asset on the statement of financial position of Goblin Combe plc, a leading premium drinks business: \($150,000\) of product sold during the...

-

Trading continues apace for your new business Climb On! The products have proved to be popular and, seeing this as your opportunity to seize the day, you decided to expand and grow the business. Here...

-

A rare book library at a University of England in England houses first edition (FE), original manuscript (OM), and authors journals (AJ). Some of these rare books are worth hundreds of thousands of...

Study smarter with the SolutionInn App