You have the following situation. KMT is a diversified company with a market value of 200mm USD.

Question:

You have the following situation. KMT is a diversified company with a market value of 200mm USD. It has a book value of $200 mm. With only $50 million in bank lines on which it draws up to the total and pays down annually, it has a very low borrowing costs. It is headquartered in Kansas and primarily it has been involved with agricultural products. This line of credit is guaranteed by the inventory of agricultural products.

It chairman has watched oil prices and as of today WTI is trading at $102bbl. It has risen over the last three years going up and down from a low of $60 bbl to today’s high. Yes, it has been volatile but has not broken below 50 for 7 years. KMT has identified a small oil field in the Balkan which he would like to buy. It looks like there is 5 mm bbl to 21 mm (million) bbl in the field based on the geological report. The price of the field is set at $40/bbl in the ground for the oil and the seller claims there are 10 mm barrels at a minimum. The acquisition price is going to be at least $400 million. Given the quality of the oil, the cost of production, a 7-year amortization of the equipment, drilling costs, etc

KMT believes one can deliver the oil at $75 bbl with costs spread over 10 mm bbl. At today’s price this leaves a $27 bbl profit before interest payments.

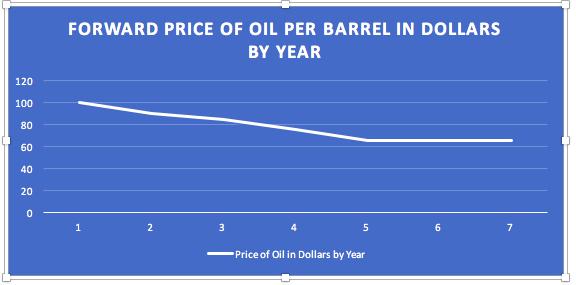

KMT has gone to a bank and asked for a project finance loan to buy the field and equipment of $500mm. They plan to spend 50 million in equity capital. The lead bank has come back and said that the project is doable only if you have hedged out the oil risk. See the shape of the forward curve. They did not say what the hedge means, but did say that if the structure was good enough it would lower their borrowing costs by a full 3% from what they would have to pay otherwise, which is 8%.

This deal is much larger than anything KMT has done. They do have expertise in that they have hired Joe the Oil Guy to oversee the project. Your job as advisor is to construct the plan of how KMT is going to borrow the money from the bank to obtain the property. Also, you should know that the annualized volatility of oil is trading in the market at around 30. At the planned pump-rate it will take 7 years to pump 21 mm bbl.

Questions 2: KMT has now fired its old advisor and is not happy with the bank. It has gone to an investment bank, which is advising them to borrow in the capital markets. What type of capital market instrument could you, the new advisor, come up with that would be acceptable to the market while also leave you with income sufficient to be profitable? As the advisor, you need a scheme that will keep the interest low enough to make all this work. Right now, KMT would have to pay 6% above treasuries for 5 - 7 year money (either floating or fixed) plus a 1% fee. What is your idea? Detail how it would work. Use the same forward curve you have above. Remember you are explaining this construct to the board, which is made up of Kansas Agricultural Folks. They probably know agricultural futures but not bonds.

Expert Answer:

Answer 1 KMT can use capital market instruments to finance their oil field acquisition One option would be to issue a bond A bond is a debt instrument in which investors loan money to KMT for a specif... View the full answer

Cornerstones of Financial and Managerial Accounting

ISBN: 978-1111879044

2nd edition

Authors: Rich, Jeff Jones, Dan Heitger, Maryanne Mowen, Don Hansen