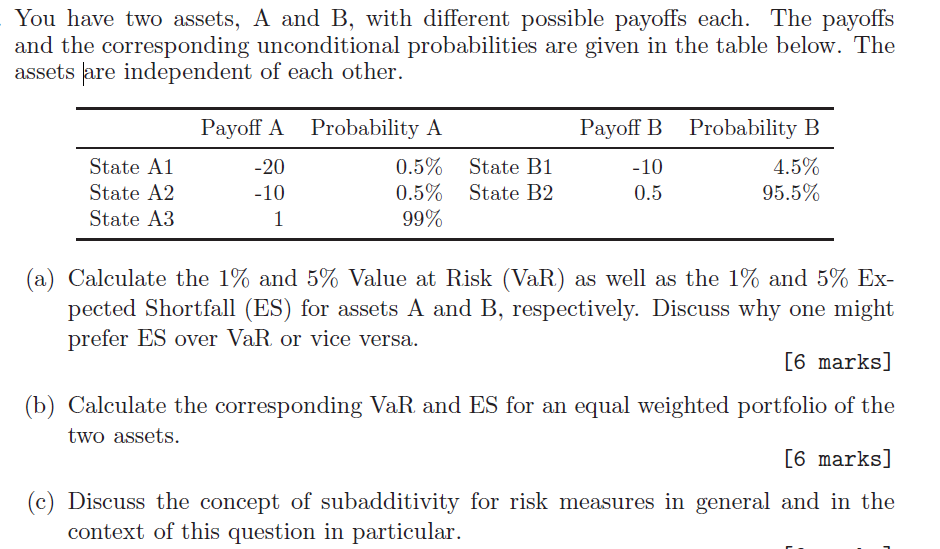

You have two assets, A and B, with different possible payoffs each. The payoffs and the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer To calculate the Value at Risk VaR and Expected Shortfall ES for assets A and B we need to determine the cumulative probabilities for each assets payoff distribution a Calculation of VaR and ES ... View the full answer

Related Book For

Multinational Finance Evaluating Opportunities Costs and Risks of Operations

ISBN: 978-1118270127

5th edition

Authors: Kirt C. Butler

Posted Date: