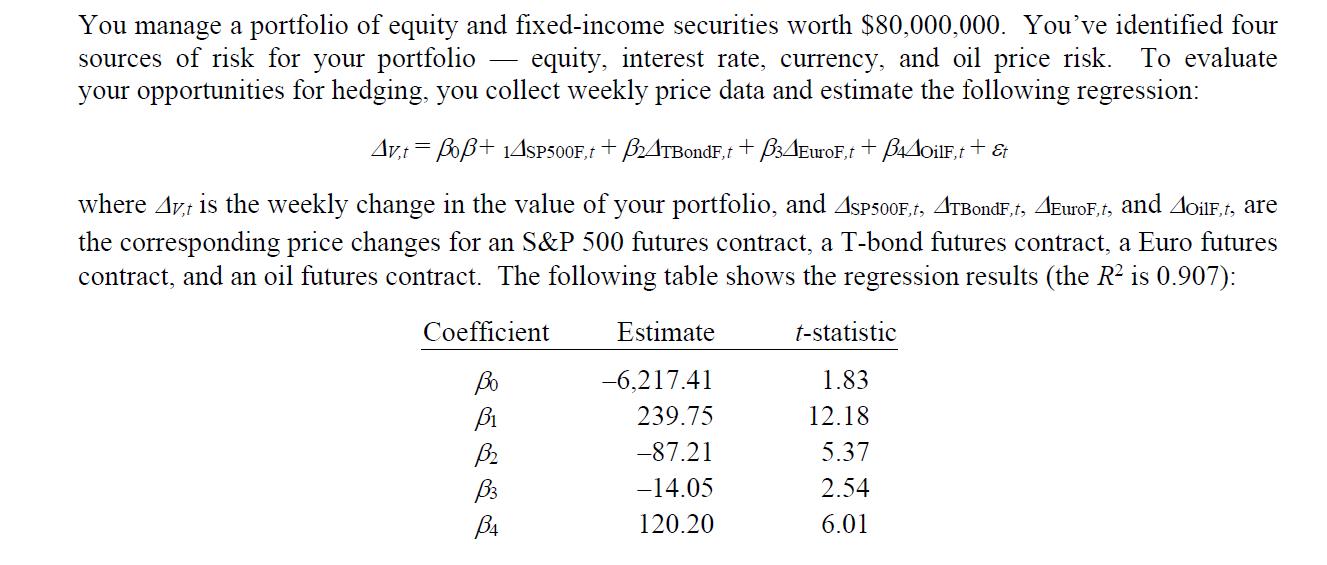

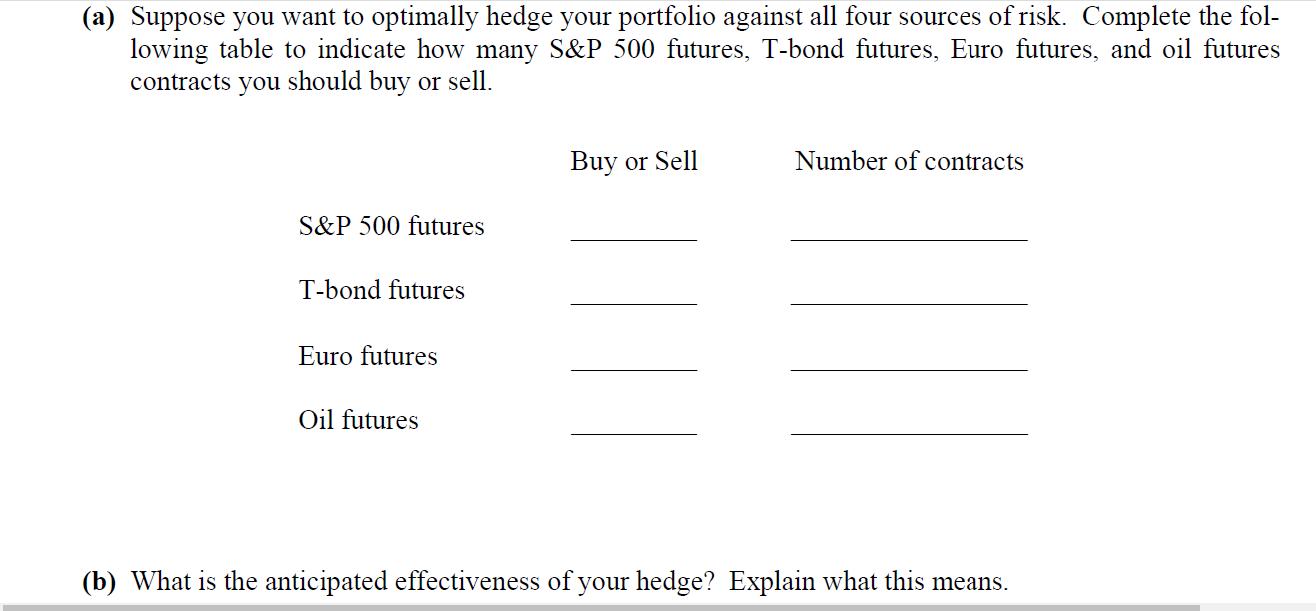

You manage a portfolio of equity and fixed-income securities worth $80,000,000. You've identified four sources of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To optimally hedge your portfolio against all four sources of risk we need to determine how many con... View the full answer

Related Book For

Intermediate Financial Management

ISBN: 9780357516669

14th Edition

Authors: Eugene F Brigham, Phillip R Daves

Posted Date: