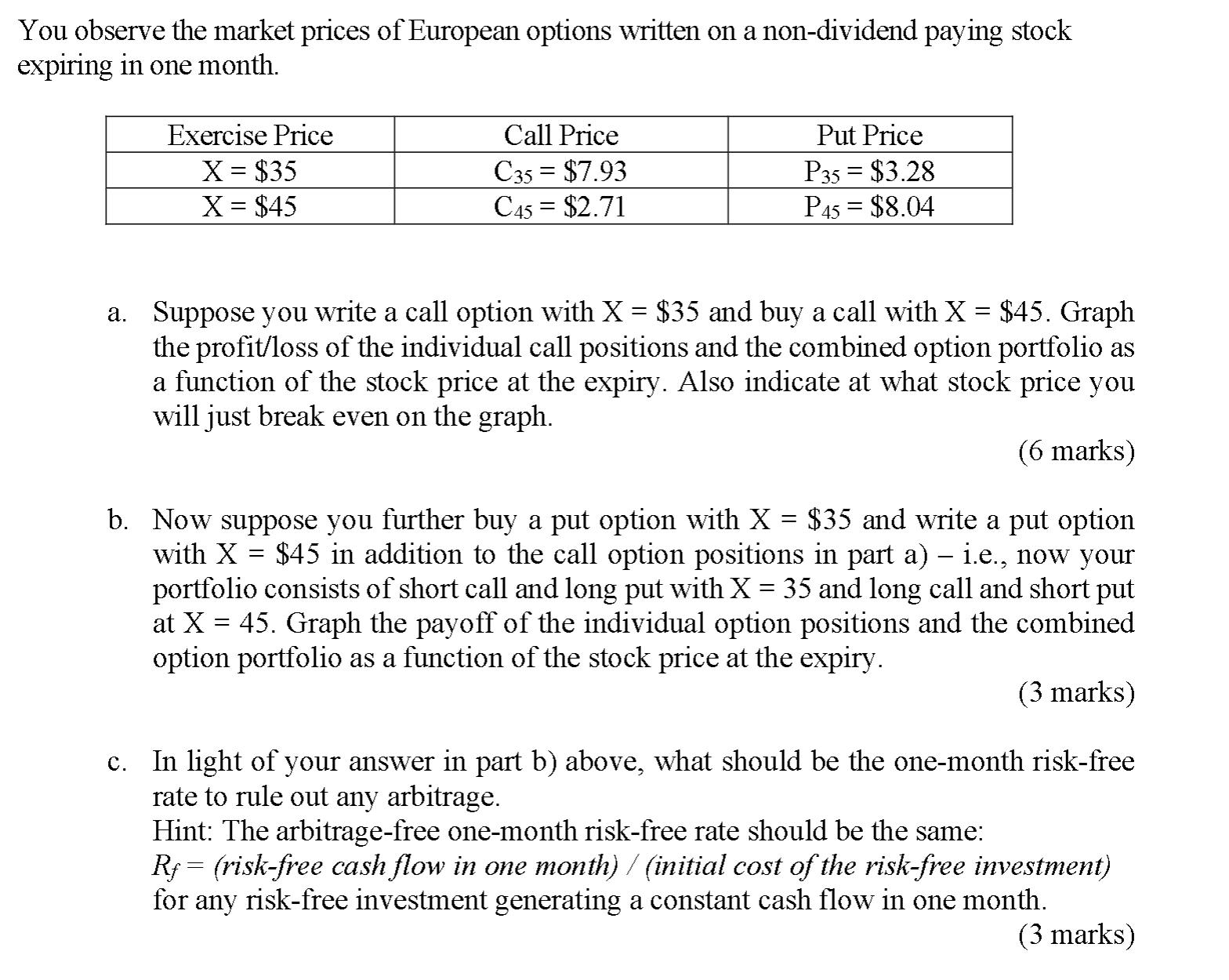

You observe the market prices of European options written on a non-dividend paying stock expiring in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION a ProfitLoss of Individual Call and Put Positions and Combined Option Portfolio Suppose we write a call option with X 35 and buy a call optio... View the full answer

Related Book For

Posted Date: