An autoregressive distributed lag model for a country observed by 25 yearly observations is estimated as where

Question:

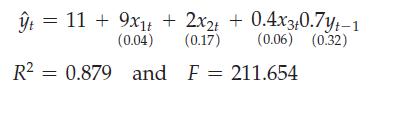

An autoregressive distributed lag model for a country observed by 25 yearly observations is estimated as

where

ŷ = inflation rate

x1 = Consumer Price Index (CPI)

x2 = price set by government

x3 = demand

The numbers below the coefficients are the coefficient standard errors.

a. Interpret the coefficients of the lagged variable.

b. Test at the 5% level the null hypothesis of the effect of the previous inflation rate on the current inflation rate.

c. Interpret the coefficient of determination.

d. What do you conclude about the significance of the overall model?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Rakshit Jain

I have 3 years of articleship experience in my chartered accountancy course, where I gathered skills of finance, accounting and other aspects of business. Further after clearing my chartered accountancy I worked in Kotak Mahindra Bank where I learned about various banking aspects. Currently I am working as an analyst in CARE Ratings where we used to analyze the financial statements of clients and give ratings to them. I am a CFA level 3 candidate also. I am also providing online tution through other sources.

Thanks

0 Reviews

10+ Question Solved

Related Book For

Statistics For Business And Economics

ISBN: 9781292315034

9th Global Edition

Authors: Paul Newbold, William Carlson, Betty Thorne

Question Posted: