Using the data in Table 7.3 (a) Compute the semiannual forward swap rate for a 1-year swap,

Question:

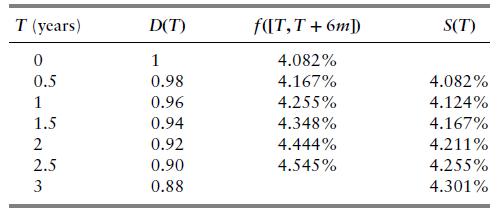

Using the data in Table 7.3

(a) Compute the semiannual forward swap rate for a 1-year swap, 2 -year forward, \(F_{2,1}\).

(b) Using Black's normal formula with \(\sigma_{N}=0.80 \%\), compute the value of a \$1M 2 year into a 1 -year ATMF payer swaption with semiannual fixed rate \(K=F_{2,1}\).

(c) Using Black's normal formula with \(\sigma_{N}=0.80 \%\), compute the value of a \$1M 2 year into 1-year ATMF receiver swaption with semiannual fixed rate \(K=F_{2,1}\).

(d) Solve for the implied volatility \(\sigma_{N}\) if the market value of a \(\$ 1 \mathrm{M}\) 2 -year into 1 -year semiannual payer swaption with \(K=5 \%\) p.a. is \(\$ 5,000\).

Table 7.3

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

GERALD KAMAU

non-plagiarism work, timely work and A++ work

6+ Reviews

11+ Question Solved

Related Book For

Mathematical Techniques In Finance An Introduction Wiley Finance

ISBN: 9781119838401

1st Edition

Authors: Amir Sadr

Question Posted: