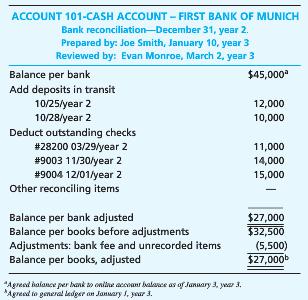

The auditor of Cubs obtained the following client-prepared bank reconciliation: The auditor for Cubs Co. has obtained

Question:

The auditor of Cubs obtained the following client-prepared bank reconciliation:

The auditor for Cubs Co. has obtained the client-prepared bank reconciliation.

The following information is available:

• Evan Monroe was promoted to controller on December 15, year 2; his former position was assistant controller—fixed assets.

• Evan Monroe has his personal bank accounts with First Bank of Munich.

• Joe Smith was hired on December 1, year 2, as a staff accountant.

• Joe Smith’s prior job was with First Bank of Munich.

• Cubs expects the year-end close to be complete on January 6, year 3.

• The adjustments on the bank reconciliation were booked on January 30, year 3.

In the table below, identify six potential issues that the auditor might have when examining the bank reconciliation prepared by Cubs from the list provided of potential issues. An issue may be used once or not at all.

1. Reconciliation is not mathematically accurate.

2. Reconciliation balance was not properly agreed to the December 31, general ledger balance.

3. Reconciliation line item “Other reconciling items” is left blank.

4. Reconciliation was not reviewed in a timely manner.

5. Reconciliation was improperly approved as reviewer had a conflict of interest.

6. Reconciliation has unsubstantiated unrecorded items.

7. Reconciliation contains aged items that should have been added to the bank balance.

8. Reconciliation was improperly prepared by someone with a conflict of interest.

9. Reconciliation does not contain a proper title.

10. Reconciliation does not agree to the cash disbursement subsidiary ledger.

11. Reconciliation was not agreed to bank statement balance at the appropriate date.

12. Reconciliation does not include January, year 3 reconciliation items.

13. Reconciliation was not prepared in a timely manner.

14. Reconciliation was prepared by an inexperienced individual.

15. Reconciliation contains stale checks.

Issues … Potential issue

A

B

C

D

E

F

Step by Step Answer:

TaskBased Simulation Issues Potential Issue A 2 Reconciliation balance was not properly agreed to th...View the full answer

Principles of Auditing and Other Assurance Services

ISBN: 978-0078025617

19th edition

Authors: Ray Whittington, Kurt Pany