The Cheetah Bus Company allocates all central corporate overhead costs to its divisions. Some costs, such as

Question:

The Cheetah Bus Company allocates all central corporate overhead costs to its divisions. Some costs, such as specified internal auditing and legal costs, are identified on the basis of time spent. However, other costs are harder to allocate so the revenue achieved by each division is used as an allocation base. Examples of such costs are executive salaries, travel, secretarial, utilities, rent, depreciation, donations, corporate planning, and general marketing costs.

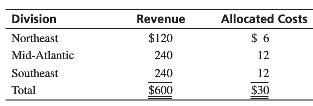

Allocations on the basis of revenue for 20X1 are as follows (in millions):

In 20X2, Northeast’s revenue remained unchanged. However, Southeast’s revenue increased to $260 million because of unusually large imports. The latter are troublesome to forecast because of variations in world markets. Mid-Atlantic had expected a sharp rise in revenue, but severe competitive conditions resulted in a decline to $220 million. The total central corporate overhead cost allocated on the basis of revenue was again $30 million, despite rises in many other costs. The president was pleased that central costs did not rise for the year.

1. Compute the allocations of costs to each division for 20X2.

2. How would each division manager probably feel about the cost allocation in 20X2 as compared with 20X1? What are the weaknesses of using revenue as a basis for cost allocation?

3. Suppose the budgeted revenues for 20X2 were $120, $240, and $280, respectively, and the budgeted revenues were used as a cost-allocation base for allocation. Compute the allocations of costs to each division for 20X2. Do you prefer this method to the one used in number 1? Why?

4. Many accountants and managers oppose allocating any central costs. Why?

Step by Step Answer:

1 2 Northeasts manager would probably be indifferent MidAtlantics would be pleased and Southeasts would be displeased The major weakness of using reve...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta