The Liverpool Company produces three types of circuit boards: Alpha, Beta, and Gamma. The cost accounting system

Question:

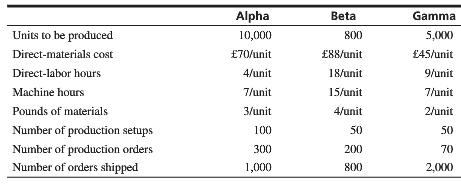

The Liverpool Company produces three types of circuit boards: Alpha, Beta, and Gamma. The cost accounting system used by Liverpool until 2012 applied all costs except direct materials to the products using direct-labor hours as the only cost driver. In 2012, the company undertook a cost study. The study determined that there were six main factors that incurred costs. A new system was designed with a separate cost pool for each of the six factors. The factors and the costs associated with each are as follows:

1. Direct-labor hours—direct-labor cost and related fringe benefits and payroll taxes

2. Machine hours—depreciation and repairs and maintenance costs

3. Pounds of materials—materials receiving, handling, and storage costs

4. Number of production setups—labor used to change machinery and computer configurations for a new production batch

5. Number of production orders—costs of production scheduling and order processing

6. Number of orders shipped—all packaging and shipping expenses

The company is now preparing a budget for 2013. The budget includes the following predictions:

The total budgeted cost for 2013 is £3,866,250, of which £995,400 was direct-materials cost, and the amount in each of the six cost pools defined previously is as follows:

Cost Pool* …………….. Cost

1 ……………. £1,391,600

2 ……………….. 936,000

3 ……………….. 129,600

4 ……………….. 160,000

5 …………………. 25,650

6 ……………….. 228,000

Total ………... £2,870,850

*Identified by the cost driver used.

1. Prepare a budget that shows the total budgeted cost and the unit cost for each circuit board. Use the new system with six cost pools (plus a separate direct application of direct-materials cost).

2. Compute the budgeted total and unit costs of each circuit board if the old direct-labor-hour sys- tem had been used.

3. How would you judge whether the new system is better than the old one?

Step by Step Answer:

1 Identified by the cost driver used Calculations for Alpha Beta and Gamma are similar 2 Total co...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta