The management of Morales Co. is reevaluating the appropriateness of using its present inventory cost flow method,

Question:

The management of Morales Co. is reevaluating the appropriateness of using its present inventory cost flow method, which is average-cost. They request your help in determining the results of operations for 2010 if either the FIFO method or the LIFO method had been used. For 2010, the accounting records show the following data.

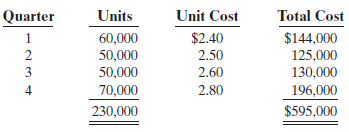

Purchases were made quarterly as follows.

Operating expenses were $147,000, and the company’s income tax rate is 34%.

Instructions

(a) Prepare comparative condensed income statements for 2010 under FIFO and LIFO. (Show computations of ending inventory.)

(b) Answer the following questions for management.

(1) Which cost flow method (FIFO or LIFO) produces the more meaningful inventory amount for the balance sheet? Why?

(2) Which cost flow method (FIFO or LIFO) produces the more meaningful net income?

Why?

(3) Which cost flow method (FIFO or LIFO) is more likely to approximate actual physical flow of the goods? Why?

(4) How much additional cash will be available for management under LIFO than under FIFO? Why?

(5) Will gross profit under the average-cost method be higher or lower than (a) FIFO and

(b) LIFO? (Note: It is not necessary to quantify your answer.)

Ending InventoryThe ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =...

Step by Step Answer:

a MORALES CO Condensed Income Statement For the Year Ended December 31 2010 FIFO LIFO Sales 865000 8...View the full answer

Accounting Principles

ISBN: 978-0470533475

9th Edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso