The Oahu Audio Company manufactures electronic subcomponents that can be sold as is or can be processed

Question:

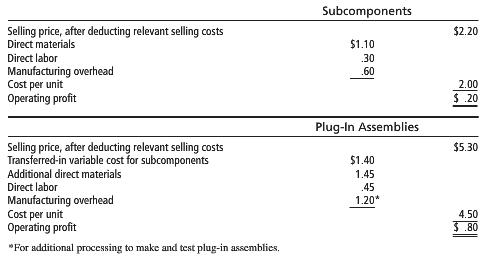

The Oahu Audio Company manufactures electronic subcomponents that can be sold as is or can be processed further into “plug-in” assemblies for a variety of intricate electronic equipment. The entire output of subcomponents can be sold at a market price of $2.20 per unit. The plug-in assemblies have been generating a sales price of $5.70 for 3 years, but the price has recently fallen to $5.30 on assorted orders.

Janet Oh, the vice president of marketing, has analyzed the markets and the costs. She thinks that production of plug-in assemblies should be dropped whenever the price falls below $4.70 per unit. However, at the current price of $5.30, the total available capacity should currently be devoted to producing plug-in assemblies. She has cited the data in Exhibit 6-7.

Direct-materials and direct-labor costs are variable. The total overhead is fixed; it is allocated to units produced by predicting the total overhead for the coming year and dividing this total by the total hours of capacity available.

The total hours of capacity available are 600,000. It takes 1 hour to make 60 subcomponents and 2 hours of additional processing and testing to make 60 plug-in assemblies.

1. If the price of plug-in assemblies for the coming year is to be $5.30, should sales of subcomponents be dropped and all facilities devoted to the production of plug-in assemblies? Show your computations.

2. Prepare a report for the vice president of marketing to show the lowest possible price for plug-in assemblies that would be acceptable.

3. Suppose 40% of the manufacturing overhead is variable with respect to processing and testing time. Repeat numbers 1 and 2. Do your answers change? If so, how?

Step by Step Answer:

1 The total amount of fixed overhead is common to all alternatives Therefore it is irrelevant to this analysis The scarce resource is hours of capacit...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta