This case study on project evaluation is applicable for beginning courses in corporate finance or finance strategy.

Question:

This case study on project evaluation is applicable for beginning courses in corporate finance or finance strategy. Two alternative investment options are available to evaluate. Challenges are presented with the inclusion of equity, bank debt, and bonds in the capital structure. Each investment option need to be evaluated carefully and decision should be made on the basis of thorough analysis of the data available using various capital structure and capital budgeting techniques.

Introduction

Brooks Hamilton recently accepted a job with Tortuga Fishing Equipment Company (Tortuga) in the company’s finance department. His first few assignments were fairly straightforward and Brooks relied on his background in both accounting and finance to get his career off to a great start. His manager, the company’s Chief Financial Officer (CFO) was impressed with his work and decided to put Brooks on a new assignment. The firm was embarking on a new project which would define its future over the upcoming years. Given the importance of the project and high degree of visibility with the firm’s senior management, Brooks was flattered to be asked to assist and eager to show that he was up to the task. The finance department was tasked with preparing an analysis to make a decision between two competing project plans which could very well decide the future of Tortuga in the competitive fishing equipment industry. The Chief Executive Officer (CEO) wants to have an answer from finance and expects a thorough analysis very quickly.

The Company

Tortuga is an Islamorada, Florida based company specializing in manufacturing high-end fishing rods and reels. Tortuga was founded by a retired university professor who fished all of his life and wanted to create the best equipment possible to handle a variety of fishing conditions and fish species. He partnered with an engineer who ran a machine shop to produce some prototype reels and supplied these to commercial fishing captains as test market research. The equipment produced by Tortuga was a significant improvement over the current line available and orders were strong. Through the years, the company made some modest improvements to their original prototype and had become an industry leader.

Tortuga’s products are used by tournament fishing teams around the world. Over the past decade, tournament fishing has grown to become a big business with corporate endorsements and prize money. This growth has made what was once a recreational vocation into a full-time profession for some anglers.

The company recently launched an extensive research and development effort focused on a new fly rod and reel designed for one particular species of fish, the Atlantic Tarpon (Megaflops atlantics). Tarpon are long-lived fishes that migrate in the warmer climes of the Caribbean Sea, Gulf of Mexico, and along the Atlantic Ocean coastlines. Although the fish can reach lengths of eight feet (~2.4 meters) and weights of 280 pounds (127 kilograms), they inhabit the shallow flats and exhibit acrobatic leaps when hooked. These traits make tarpon a popular game fish for anglers. Fishing gear needs to be sturdy to handle the power of these fish and Tortuga had developed products for this niche market which were allowing anglers to be successful in their angling pursuits.

Recently, several sponsors had come together to launch competitive angling events called tournaments, where the best anglers vie to catch, and then release, the most and largest tarpon. Winners may receive up to $50,000 in a single weekend tournament and the difference between winning and losing could be a few pounds. With so much money at stake, tournament teams purchase the best gear available and are always looking for any competitive advantage with their equipment. Tortuga is looking to capitalize on this trend by offering a new line called the Tortuga Tarpon Classic. This new line incorporates the latest material and design improvements and is predicted to be the “gold standard” for all serious tournaments anglers. Tortuga plans to offer the Tortuga Tarpon Classic to recreational anglers as well to capture the growing demand by affluent anglers who want the same high-quality gear as the professionals.

Financial Information

Tortuga began with a modest amount of capital that the founder had managed to save during his years in academia. As the firm grew, its financing needs expanded as well. Through the years Tortuga had developed and maintained a strong relationship with a large bank which provided short-term working capital funds in the form of a revolving line of credit. When a funding need arose, Tortuga would draw from this line of credit and then repay the short-term draw as cash flowed back to Tortuga. The $200 million revolving line of credit currently has $25 million drawn at an interest rate of 3-month Libor plus 350 basis points. The remaining $175 million credit line can be assumed to have no fees associated with it. Brooks looks up the most recent 3month U.S. dollar Libor rate and sees that it is 1.50%.

Long-term financing was also in place in two forms. After several years of revenue and earnings growth, Tortuga issued five million shares of common stock at an issue price of $10 per share. The firm used this $50 million in funding to increase production lines and build a global presence by opening an additional manufacturing facility in Panama. Brooks finds the current price per share for Tortuga to be $16. Two years ago, Tortuga issued a 10-year bond for $50 million face value. Each $1,000 par bond carries a coupon of 8.5%. The bond pays interest semi-annually and is currently trading in the market at 102.50 as a percent of par. The company has a 34% corporate tax rate.

The firm calculates its required return on equity with the Capital Asset Pricing Model (CAPM) using a 4.0% historical Treasury rate for the risk-free rate and 6.0% as the historical market risk premium.

CAPM = Risk-free rate + beta (Market Risk Premium) (1)

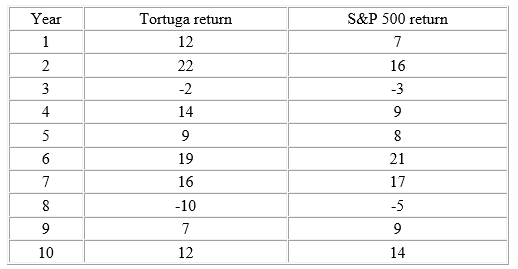

The annual stock returns versus the market are shown in Figure 1 below for the past 10 years. Beta is calculated by regressing Tortuga stock returns on the Standard & Poor’s (S&P) 500 returns. There are a variety of methods for calculating beta. Brooks could find beta by regressing five years of weekly Tortuga returns of the S&P 500. He could use five years of monthly returns or two years of weekly returns. Each of these is a valid sample period. One well-known data source provides an “adjusted” beta which is determined by first calculating a “raw” beta by regressing two years of weekly security returns on the market. This is then adjusted by taking 2/3 of the raw beta plus 1/3 of one. This adjusts the beta to be closer to one, since beta is not stationary and should naturally move towards one through time as a firm expands. Brooks only has 10 years of annual data available at the time and decides to conduct the analysis with this information to get a quick response. He will check his result with more data points before submitting his final report to the CFO.

Figure 1 Returns on Tortuga Stock versus the Standard & Poor 500

After Brooks calculates beta he employs formula (1) above along with the risk-free rate and market risk premium to determine the cost of equity. The firm’s weighted average cost of capital is a function of its equity market capitalization, cost of equity, short- and long-term debt amounts and costs, and the tax rate. Using formula (2) below, Brooks can find the firm’s weighted average cost of capital (WACC).

WACC = wdkd(1-T) + weke

where:

WACC = weighted average cost of capital

wd = weight of debt to total capital (note: this includes short- and long-term)

kd = cost of debt using yield to maturity and current values for short-term

T = corporate tax rate

we = weight of market capitalization to total capital

ke = cost of equity determined with CAPM

Tortuga Tarpon Classic

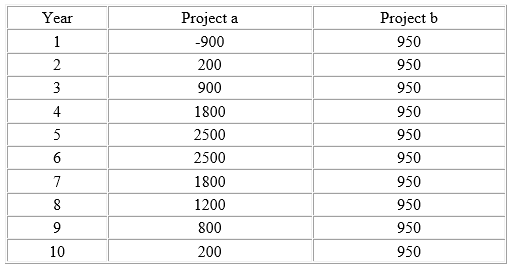

The company has two separate research teams working on the project and they develop two distinctly different fishing combinations. The two rod and reel combinations are test marketed with guides and past tournament champions and demand forecasts are determined. Most fishing gear has a relatively short life due to continual product innovation. Manufacturing of the two combinations is estimated to require an upfront cost of $5 million to retool the machine shop. The process for manufacturing the two combinations differ and ongoing variable costs are not the same. The net cash flows for the entire ten year expected life of the product is shown in Table 2 as Project A and Project B (all figures are $thousands of net cash flow).

Project A focuses on hand tooled fishing equipment which results in a more labor intensive process, but also allows for personalized features for customers. The price charged for customization offset the slower hand tooling process to generate substantial net cash flows. Part of the upfront $5 million includes the costs of training more machinists in the art of hand tooling, which is similar to watch making but with a few less moving parts. Project A is anticipated to generate lower cash flows in the early years due to the length of time required to get machinists who are adept at hand tooling to customer specifications. In fact, during the first year there will be continued expenses to attain these skills which causes year one net cash flows to be negative. Over time the cash flows increase as more machinists gain proficiency. The project is expected to experience lower cash flows towards the end of its life due to market saturation. Due to the quality of the reels, they are built to last and seldom fail or wear out. Technological obsolescence is certain although Tortuga will be investing cash flows into research and development to launch the next generation at the conclusion of the Tortuga Tarpon Classic life cycle.

Project B employs a mechanized approach to large scale production of standardized equipment. Although the approach does not allow for personalization, it does allow Tortuga to build its inventory quickly and capture positive net cash flows immediately. The upfront expense is almost completely devoted to tooling equipment procurement and the number of units produced will be much higher and at lower price points than the approach of Project A. At the end of both projects life it is assumed that there will be zero salvage value as the pace of innovation will require a complete re-tooling for the next generation and the useful life of the equipment will have been fully realized.

Brooks realizes that he will need to calculate the firm’s cost of capital discount rate and apply this to the cash flow projections of both projects. He recalls all of the assignments he completed at university and is thankful to have been so well-prepared for this task. He gets a cup of coffee, sits down at his desk, and gets to work.

Figure 2 Project Net Cash Flows for Tortuga Fishing Equipment ($thousands)

Since Brooks is new to his role, you have been asked to review his work and assess the financial viability of the projects. Given the importance of this decision you are helping to make sure the firm makes the right choice.

Specific Questions

1. Using the Capital Asset Pricing Model, what is the required rate of return on equity, ke (cost of equity) for Tortuga?

2. Analyzing the company’s bond, what is the yield to maturity on the bond issue, kd (cost of debt)?

3. Using the market weight of equity, the original issue amount of debt, and the outstanding portion of the revolving line of credit, what are the weights of equity and debt in the capital structure (we & wd)?

4. Using the information provided, what is the firm’s weighted average cost of capital (WACC, ka)?

Common StockCommon stock is an equity component that represents the worth of stock owned by the shareholders of the company. The common stock represents the par value of the shares outstanding at a balance sheet date. Public companies can trade their stocks on... Salvage Value

Salvage value is the estimated book value of an asset after depreciation is complete, based on what a company expects to receive in exchange for the asset at the end of its useful life. As such, an asset’s estimated salvage value is an important... Capital Asset Pricing Model

The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and expected return for assets, particularly stocks. The CAPM is a model for pricing an individual security or portfolio. For individual securities, we make use of the security market line (SML) and its... Capital Budgeting

Capital budgeting is a practice or method of analyzing investment decisions in capital expenditure, which is incurred at a point of time but benefits are yielded in future usually after one year or more, and incurred to obtain or improve the... Capital Structure

Capital structure refers to a company’s outstanding debt and equity. The capital structure is the particular combination of debt and equity used by a finance its overall operations and growth. Capital structure maximizes the market value of a... Cost Of Capital

Cost of capital refers to the opportunity cost of making a specific investment . Cost of capital (COC) is the rate of return that a firm must earn on its project investments to maintain its market value and attract funds. COC is the required rate of... Cost Of Debt

The cost of debt is the effective interest rate a company pays on its debts. It’s the cost of debt, such as bonds and loans, among others. The cost of debt often refers to before-tax cost of debt, which is the company's cost of debt before taking... Cost Of Equity

The cost of equity is the return a company requires to decide if an investment meets capital return requirements. Firms often use it as a capital budgeting threshold for the required rate of return. A firm's cost of equity represents the... Coupon

A coupon or coupon payment is the annual interest rate paid on a bond, expressed as a percentage of the face value and paid from issue date until maturity. Coupons are usually referred to in terms of the coupon rate (the sum of coupons paid in a... Discount Rate

Depending upon the context, the discount rate has two different definitions and usages. First, the discount rate refers to the interest rate charged to the commercial banks and other financial institutions for the loans they take from the Federal... Line of Credit

A line of credit (LOC) is a preset borrowing limit that can be used at any time. The borrower can take money out as needed until the limit is reached, and as money is repaid, it can be borrowed again in the case of an open line of credit. A LOC is... Maturity

Maturity is the date on which the life of a transaction or financial instrument ends, after which it must either be renewed, or it will cease to exist. The term is commonly used for deposits, foreign exchange spot, and forward transactions, interest...

Step by Step Answer:

1 Compute cost of equity capital in the following steps First step Compute beta of stock using SLOPE ...View the full answer

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley