Thomas-Britt Industries was founded by Matt Thomas in 1950 as a small machine shop that produced parts

Question:

Thomas-Britt Industries was founded by Matt Thomas in 1950 as a small machine shop that produced parts for the aircraft industry. The Korean War brought rapid growth to Thomas-Britt. By the end of the war, the company's annual sales had reached $15 million, almost exclusively from government contracts. The next 40 years brought slow but steady growth. Cost-reimbursement contracts from the government continued to be the main source of revenue.

In the early-1990s, president Will Thomas, son of the founder, realized that Thomas-Britt could not depend on government contracts for long-term growth and stability. Consequently, he began planning for diversified commercial growth. By the end of 2003, Thomas-Britt had succeeded in reducing government contract sales to 50% of total sales.

Traditionally, the costs of the Materials Handling Department have been allocated to other departments as a percentage of the dollar value of direct materials. Peter Anderson, manager of the government contracts unit, has been complaining about this allocation for several months.

He believes that since his unit's materials costs are high and materials handling activities are low relative to the commercial unit, he is absorbing more than his fair share of this overhead.

He wants to find a way to transfer some of these charges to another unit, thereby increasing the government contracts unit's profitability and his year-end performance bonus.

Peter shared his views in a recent meeting with Sarah Lindley, the newly hired cost accounting manager, and Reese Mason, manager of the commercial unit. After a heated discussion, Sarah agreed to investigate the current allocation method and, if appropriate, recommend an alternative method.

After doing some research, Sarah learned the following:

• The majority of the direct materials purchases for government contracts are high-dollar, low-volume purchases. Direct materials purchases for commercial contracts are mostly low-dollar, high-volume purchases.

• There are other departments that use the services of the Materials Handling Department on a limited basis, but they have never been charged for materials handling costs.

• One purchasing agent with a direct phone line is assigned exclusively to purchasing high-dollar, low-volume materials for government contracts, at an annual salary of

$36,000. His employee benefits are estimated to amount to 20% of his annual salary.

The dedicated phone line costs $2,800 a year.

The Materials Handling Department's budget for 2014, as proposed by Sarah Lindley's predecessor, follows.

Payroll ...............$ 180,000

Employee benefits ......... 36,000

Telephone............. s 38,000

Other utilities............. 22,000

Materials and supplies......... 6,000

Depreciation............. 6,000

Total materials handling costs..... $ 288,000

Direct materials budget

Government contracts......... $1,958,400

Commercial products.......... 921,600

Total direct materials budget...... $2,880,000

After reviewing the situation, Lindley has recommended that allocating materials handling costs based on the number of purchase orders issued is preferable to the current allocation based on direct materials cost. She estimated the number of purchase orders to be processed in 2014 as follows:

Government contracts...... 79,860

Commercial products...... 154,880

Other.............. 7,260

Total ..............242,000

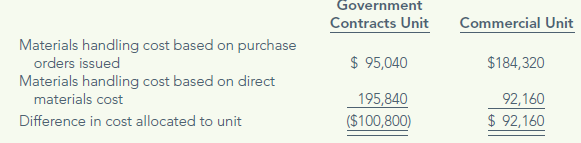

Using the 2014 estimates, she provided the following analysis to Anderson and Mason.

When Mason saw the projected increase in the commercial unit's costs, he exploded. He was not going to lose any of his year-end performance bonus just because Lindley wanted to change the way she calculated the numbers. He marched into Lindley's office and reminded her that he had been with the company for 25 years and had "plenty of pull" with Thomas as a member of the senior management team. He then told her to "adjust" her numbers and modify her recommendation so that the results would be more favorable to the commercial unit. He added that since materials handling costs were only allocated to the government contract and commercial units, she could just hide some of the commercial unit's purchase order volume in those other units.

Given her new position, Lindley is not sure how to proceed. She questions his motivation.

To complicate matters, Thomas has asked her to prepare a three-year forecast of the two units' results, for which she believes the new allocation method would provide the most accurate data. Using the new method would put her in direct opposition to Mason's directives, however.

Lindley has assembled the following forecasted data to project the units’ direct materials handling costs.

Required

a. Using the forecasted information, calculate the materials handling costs that would be allocated to each unit under both allocation methods. Show the cumulative dollar impact over the three-year period 2014–2016.

b. Why might the number of purchase orders be a better cost driver for materials handling costs than direct materials cost?

c. Are there other factors in the allocation that Lindley should consider?

d. In a recent meeting between Sarah Lindley and Reese Mason, Mason said that there is nothing in any accounting pronouncement that requires the use of activity-based costing. Therefore, there is no reason to make Lindley’s recommended change in allocation methods. Do you agree with Mason? Why or why not?

e. What ethical conflict does Sarah Lindley face? What specific steps should she take to resolve it? Refer to the IMA Statement of Ethical Professional Practice (Exhibit 1-8) in developing youranswer.

Step by Step Answer:

a Allocation based on materials cost 2014 2015 2016 Total Government contracts unit 19584000 22874950 26209400 68668350 Commercial unit 9216000 9803550 11232600 30252150 Total direct materials cost 28...View the full answer