Thorn Company uses the accounts receivable aging method to estimate uncollectible accounts. At the beginning of the

Question:

Thorn Company uses the accounts receivable aging method to estimate uncollectible accounts. At the beginning of the year, the balance of the Accounts Receivable account was a debit of $45,215, and the balance of Allowance for Uncollectible Accounts was a credit of $4,050. During the year, the store had sales on account of $237,500, sales returns and allowances of $3,100, worthless accounts written off of $4,400, and collections from customers of $226,363. At the end of the year (December 31, 2011), a junior accountant for Thorn was preparing an aging analysis of accounts receivable. At the top of page 6 of the report, the following totals appeared:

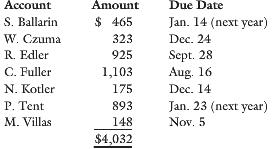

To finish the analysis, the following accounts need to be classified:

From past experience, Thorn has found that the following rates are realistic for estimating uncollectible accounts:

Percentage Considered

Time Uncollectible

Not yet due 2

1–30 days past due 5

31–60 days past due 15

61–90 days past due 25

Over 90 days past due 50

REQUIRED

1. Complete the aging analysis of accounts receivable.

2. Compute the end-of-year balances (before adjustments) of Accounts Receivable and Allowance for Uncollectible Accounts.

3. Prepare an analysis computing the estimated uncollectible accounts.

4. Calculate Thorn’s estimated uncollectible accounts expense for the year (round the amount to the nearest whole dollar).

5. What role do estimates play in applying the aging analysis? What factors might affect these estimates?

Accounts ReceivableAccounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that...

Step by Step Answer:

1 Aging analysis completed Thorn Company Aging Analysis of Accounts Receivable December 31 2011 3 An...View the full answer