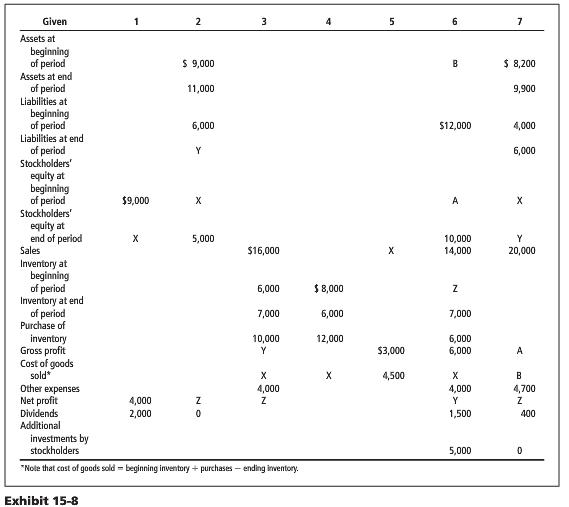

Three former RIM employees decided to go into business for themselves and open a store near an

Question:

Three former RIM employees decided to go into business for themselves and open a store near an office park to sell wireless equipment to young professionals. Their first products were cell phones, PDAs, netbook and notebook computers, and computer accessories. The business was incorporated as Connectivity Plus. The following transactions occurred during April:

a. On April 1, 20X1, each of the three invested $12,000 in cash in exchange for 1,000 shares of stock each.

b. The corporation quickly acquired $40,000 in inventory, half of which had to be paid for in cash. The other half was acquired on open accounts that were payable after 30 days.

c. A store was rented for $500 monthly. A lease was signed for one year on April 1. The first 2 months’ rent was paid in advance. Monthly payments were to be made on the second of each month.

d. Advertising during April was purchased on open account for $3,000 from a newspaper owned by one of the stockholders. Additional advertising services of $6,000 were acquired for cash.

e. Sales were $62,000. Merchandise was sold for twice its purchase cost. Sales of $52,000 were on open account, and the remaining $10,000 were for cash.

f. Wages and salaries incurred in April amounted to $11,000, of which $4,000 was paid in cash.

g. Miscellaneous services paid for in cash were $2,510.

h. On April 1, fixtures and equipment were purchased for $6,000 with a down payment of $1,000 plus a $5,000 note payable in one year.

i. See transaction h and make the April 30 adjustment for interest expense accrued at 9.6%. (The interest is not due until the note matures.)

j. See transaction h and make the April 30 adjustment for depreciation expense on a straight-line basis. The estimated life of the fixtures and equipment is 10 years with no expected residual value. Straight-line depreciation here would be $6,000 ÷ 10 years = $600 per year, or $50 per month.

k. Cash dividends of $6,000 were declared and disbursed to stockholders on April 29.

1. Using the accrual basis of accounting, prepare an analysis of transactions, employing the equation approach demonstrated in Exhibit 15-1 on page 621. Use the following headings: Cash, Accounts Receivable, Inventory, Prepaid Rent, Fixtures and Equipment, Accounts Payable, Notes Payable, Accrued Wages Payable, Accrued Interest Payable, Paid-in Capital, and Retained Earnings.

2. Prepare a balance sheet and a multiple-step income statement. Also show the components of the change in retained earnings.

3. What advice would you give the owners based on the information compiled in the financial statements?

Balance SheetBalance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial... Corporation

A Corporation is a legal form of business that is separate from its owner. In other words, a corporation is a business or organization formed by a group of people, and its right and liabilities separate from those of the individuals involved. It may...

Step by Step Answer:

1 See Exhibit 1539 on the following page 430 5490 52000 9000 500 5950 23000 5000 7000 40 36000 1900 ...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta