Thurgood Devices uses activity-based costing to allocate overhead costs to customer orders for pricing purposes. Many customer

Question:

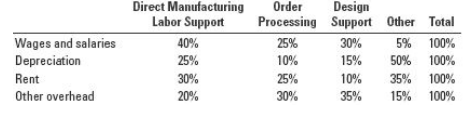

Thurgood Devices uses activity-based costing to allocate overhead costs to customer orders for pricing purposes. Many customer orders are won through competitive bidding. Direct material and direct manufacturing labor costs are traced directly to each order. Thurgood?s direct manufacturing labor rate is $ 20 per hour. The company reports the following yearly overhead costs: Wages and salaries $ 480,000 Depreciation 60,000 Rent 120,000 Other overhead 240,000 Total overhead costs $ 900,000

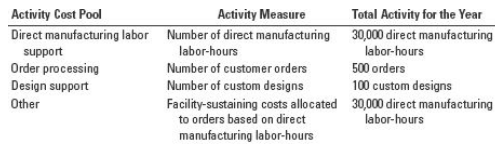

Thurgood has established four activity cost pools:

Only about 20% of Thurgood?s yearly orders require custom designs. Paul Moeller, Thurgood?s controller, has prepared the following estimates for distribution of the over-head costs across the four activity cost pools:

Order 448200 required $ 4,550 of direct materials, 80 direct manufacturing labor-hours, and one custom design.

Required

1. Allocate the overhead costs to each activity cost pool. Calculate the activity rate for each pool.

2. Determine the cost of Order 448200.

3. How does activity-based costing enhance Thurgood?s ability to price its orders? Suppose Thurgood used a traditional costing system to allocate all overhead costs to orders on the basis of direct manu-facturing labor-hours. How might this have affected Thurgood?s pricing decisions?

DistributionThe word "distribution" has several meanings in the financial world, most of them pertaining to the payment of assets from a fund, account, or individual security to an investor or beneficiary. Retirement account distributions are among the most...

Step by Step Answer:

1 Direct Manuf Labor Support Order Processing Design Support Other Total Wages and salaries 192000 1...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0133428704

15th edition

Authors: Charles T. Horngren, Srikant M. Datar, Madhav V. Rajan