Toni Tickmark has been assigned to plan the audit of the Cajuzzi Corporation, and is currently planning

Question:

Toni Tickmark has been assigned to plan the audit of the Cajuzzi Corporation, and is currently planning the circularization (confirmation) of accounts receivable. Cajuzzi sells a number of products in the personal health care field but its mainstay is a portable whirlpool unit for use in bathtubs called the

“Ecstasizer.” Offering the same therapeutic muscle-relaxing benefits as built-in units costing up to four times more, the Ecstasizer has been an outstanding success and is largely responsible for the 14% jump in sales this year.

Cajuzzi has five major categories of customers: wholesalers, department store chains, drug stores, hardware stores, and sporting goods stores. Because the health care industry is highly competitive and a number of “clones” are appearing on the market, Cajuzzi has an aggressive sales strategy coupled with fairly liberal credit policies. Viewing onsite store displays as its primary advertising media, Cajuzzi actually gives each customer a display unit for demonstration purposes. These costs are charged to promotion expense. It is the stated objective of the company to have every store in the country displaying its products.

New customers are extended credit using a very liberal credit policy, and terms are net/30. Cajuzzi will not stop shipments unless balances are more than 120 days old. Customers’ credit status is returned to normal as soon as the overdue balances are paid. Cajuzzi is loathe writing off any account unless the customer is actually insolvent or has given intent not to pay.

Gucci Schedule

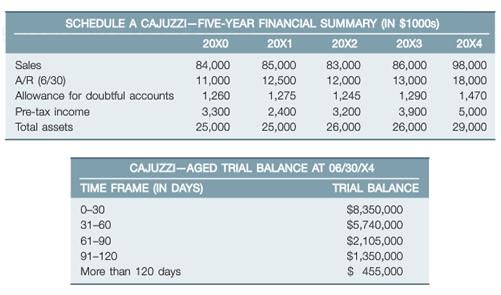

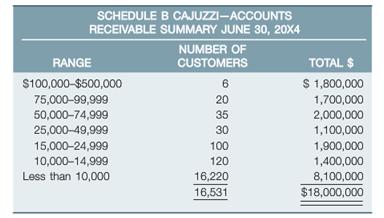

Schedule A contains a five-year summary of key financial data, and Schedule B has a summary of accounts receivable at the year-end circularization date (June 30, 20X4). This is the second year that Toni’s firm has been the auditor of Cajuzzi, and her first year on the engagement. Last year’s working papers showed that the 50 largest accounts were circularized, which was coverage of 20% ($2,600,000).

Overstatement of accounts receivable of $190,000 was discovered, but no adjustment was proposed as the error was deemed immaterial.

Required:

a. Critique last year’s (20X3) approach to the circularization of receivables and the subsequent disposition of errors discovered.

b. What is meant by random (representative) selection, and why is it the most fundamental principle of sampling theory? Under what conditions is nonrandom selection appropriate?

c. What is meant by the terms sampling error and non-sampling error? What steps can the auditor take to control these?

d. Design a sampling plan for the circularization of receivables for Cajuzzi at June 30, 20X4. Cajuzzi’s product line includes the following:

• Bathtub whirlpool units

• Exercise equipment (rowers, bikes, and mini-gyms)

• Heating pads, massage units, and footbaths

• Air purifiers and ionizers

• “Healthware” cooking utensils

• Skin care products and vitamin supplements

• Track suits, footwear, and sportswear

Accounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that...

Step by Step Answer:

a Critique of Last Years Circularization Sample Selection The method of sampling chosen in 1996 was only specific items and not representative The selection was made according to size and therefore ca...View the full answer

Auditing An International Approach

ISBN: 978-0071051415

6th edition

Authors: Wally J. Smieliauskas, Kathryn Bewley