You are evaluating various investment opportunities currently available and you have calculated expected returns and standard deviations

Question:

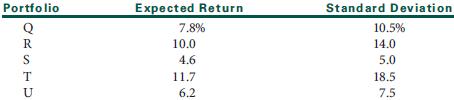

You are evaluating various investment opportunities currently available and you have calculated expected returns and standard deviations for five different well-diversified portfolios of risky assets:

a. For each portfolio, calculate the risk premium per unit of risk that you expect to receive ([E(R) − RFR]/σ). Assume that the risk-free rate is 3.0 percent.

b. Using your computations in Part a, explain which of these five portfolios is most likely to be the market portfolio. Use your calculations to draw the capital market line (CML).

c. If you are only willing to make an investment with σ = 7.0%, is it possible for you to earn a return of 7.0 percent?

d. What is the minimum level of risk that would be necessary for an investment to earn 7.0 percent? What is the composition of the portfolio along the CML that will generate that expected return?

e. Suppose you are now willing to make an investment with σ = 18.2%. What would be the investment proportions in the riskless asset and the market portfolio for this portfolio?

What is the expected return for this portfolio?

Step by Step Answer:

a Q 48105 04571 R 714 05000 S165 03200 T87185 04703 U 3275 04267 b The CML slope ER MKT RFR MKT is the ratio of risk premium per unit of risk Portfoli...View the full answer

Investment Analysis and Portfolio Management

ISBN: 978-0538482387

10th Edition

Authors: Frank K. Reilly, Keith C. Brown