You have been hired as a risk manager for Acorn Savings and Loan. Currently, Acorns balance sheet

Question:

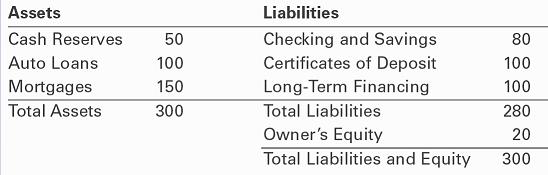

You have been hired as a risk manager for Acorn Savings and Loan. Currently, Acorn’s balance sheet is as follows (in millions of dollars):

When you analyze the duration of loans, you find that the duration of the auto loans is two years, while the mortgages have a duration of seven years. Both the cash reserves and the checking and savings accounts have a zero duration. The CDs have a duration of two years and the long-term financing has a 10-year duration.

a. What is the duration of Acorn’s equity?

b. Suppose Acorn experiences a rash of mortgage prepayments, reducing the size of the mortgage portfolio from $150 million to $100 million, and increasing cash reserves to $100 million. What is the duration of Acorn’s equity now? If interest rates are currently 4% but fall to 3%, estimate the approximate change in the value of Acorn’s equity.

c. Suppose that after the prepayments in part (b), but before a change in interest rates, Acorn considers managing its risk by selling mortgages and/or buying 10-year Treasury STRIPS (zero-coupon bonds). How many should the firm buy or sell to eliminate its current interest rate risk?

Balance SheetBalance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial... Portfolio

A portfolio is a grouping of financial assets such as stocks, bonds, commodities, currencies and cash equivalents, as well as their fund counterparts, including mutual, exchange-traded and closed funds. A portfolio can also consist of non-publicly...

Step by Step Answer:

a From Eq 308 Asset Duration 50300 0yrs 100300 2yrs 150300 7yrs 417yrs Liability ...View the full answer