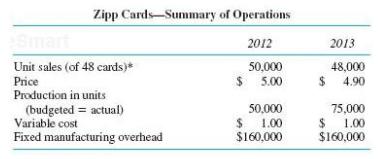

Zipp Cards buys baseball cards in bulk from the companies that produce them. Zipp buys sheets of

Question:

Zipp Cards buys baseball cards in bulk from the companies that produce them. Zipp buys sheets of 48 cards, then cuts the sheets into individual cards, and sorts and packages them, usually by team. Zipp then sells the packages to large discount stores. The accompanying table provides information regarding operations for 2012 and 2013.

Volume is measured in terms of 48- card sheets processed. Budgeted production and actual production in 2012 were both 50,000 units. There were no beginning inventories on January 1, 2012. In 2013, budgeted and actual production rose to 75,000 units.

At the beginning of 2013, the president of Zipp was pleasantly surprised when the accountant showed her the income statement for the year 2012. The president remarked, “ I’m surprised we made more money in 2013 than 2012. We had to cut prices and we didn’t sell as many units, yet we still made more money. Well, you’re the accountant and these numbers don’t lie.”

Required:

a. Prepare income statements for 2012 and 2013 using absorption costing.

b. Prepare a statement reconciling the change in net income from 2012 to 2013. Explain to the president why the firm made more money in 2013 than in 2012.

Step by Step Answer:

a The table below calculates absorption costing net income for 2012 and 2013 b Inco...View the full answer

Accounting for Decision Making and Control

ISBN: 978-0078025747

8th edition

Authors: Jerold Zimmerman