Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

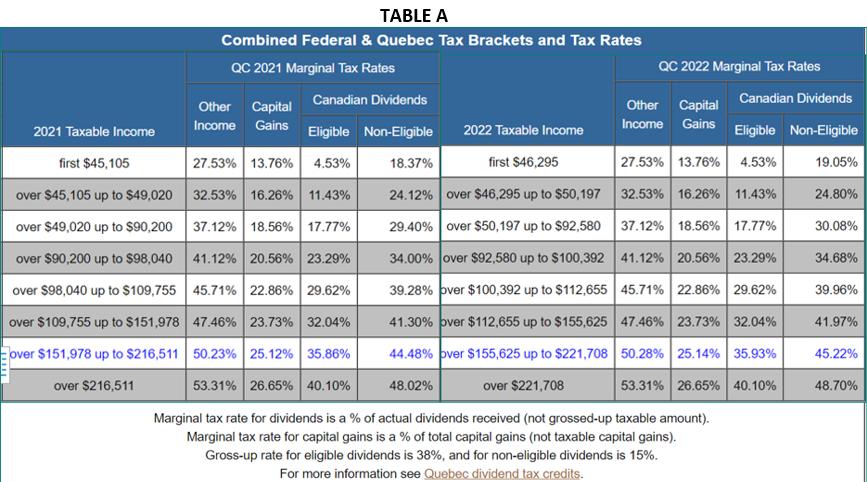

Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits. Ava has asked you to help prepare her 2021 personal income tax returns (combined Federal and Quebec). For 2021, she provided you with the following: • 14 tax slip from Hydro-Québec where she works as an engineer, reporting her 2021 gross annual salary of $105,000; T5 tax slip showing interest income received in 2021 of $1,500; On December 1, 2021, she sold 100 shares in Canadian Tire for $180/share (she had purchased 150 shares when they were at $110/share in 2019); Made a Tax-Free Savings Account (TFSA) contribution of $6,000 on January 1, 2021; Contributed the maximum to her Registered Retirement Savings Plan (RRSP) plan on May 15, 2021, when she received her company bonus (note that her 2020 earned income was $100,000; she maximizes her RRSP contribution each year and is not part of a company pension plan); Professional dues from the Order of Quebec Engineers that she can deduct in the amount of $945; and Has a capital loss of $600 from a previous year that she can deduct against her capital gain. b) Calculate Ava's combined Federal and Quebec taxes payable. Use Table A, 2021 tax rates. Ignore non-refundable tax credits. Calculate Ava's combined Federal and Quebec 2021 taxes payable c) Calculate Ava's average tax rate. Calculate Ava's 2021 average tax rate d) What is Ava's marginal tax rate? Ava's 2021 marginal tax rate TABLE A Combined Federal & Quebec Tax Brackets and Tax Rates QC 2021 Marginal Tax Rates QC 2022 Marginal Tax Rates Other Capital Canadian Dividends Income Gains Eligible Non-Eligible Canadian Dividends Other Capital Income Gains Eligible Non-Eligible 2021 Taxable Income 2022 Taxable Income first $45,105 27.53% 13.76% 4.53% 18.37% first $46,295 27.53% 13.76% 4.53% 19.05% over $45,105 up to S49,020 32.53% 16.26% 11.43% 24.12% over $46,295 up to $50,197 32.53% 16.26% 11.43% 24.80% over $49,020 up to $90,200 37.12% 18.56% 17.77% 29.40% over $50,197 up to $92,580 37.12% 18.56% 17.77% 30.08% over $90,200 up to $98,040 41.12% 20.56% 23.29% 34.00% over $92,580 up to $100,392 41.12% 20.56% 23.29% 34.68% over $98,040 up to $109,755 45.71% 22.86% 29.62% 39.28% þver $100,392 up to $112,655 45.71% 22.86% 29.62% 39.96% over $109,755 up to $151,978 47.46% 23.73% 32.04% 41.30% pver $112,655 up to $155,625 47.46% 23.73% 32.04% 41.97% Eover $151,978 up to $216,511 50.23% 25.12% 35.86% 44.48% þver $155,625 up to $221,708 50.28% 25.14% 35.93% 45.22% over $216,511 53.31% 26.65% 40.10% 48.02% over $221,708 53.31% 26.65% 40.10% 48.70% Marginal tax rate for dividends is a % of actual dividends received (not grossed-up taxable amount). Marginal tax rate for capital gains is a % of total capital gains (not taxable capital gains). Gross-up rate for eligible dividends is 38%, and for non-eligible dividends is 15%. For more information see Quebec dividend tax credits.

Expert Answer:

Answer rating: 100% (QA)

a It is February 18 2022 calculate Avas 2021 Taxable Income 90455 b Calculate Avas combined Federal and Quebec taxes payable Use Table A 2021 tax rate... View the full answer

Related Book For

Advanced Financial Accounting

ISBN: 978-0078025624

10th edition

Authors: Theodore E. Christensen, David M. Cottrell, Richard E. Baker

Posted Date:

Students also viewed these finance questions

-

A midsized business with 100 end-users has asked you to develop a new intranet with a prioritizing requirement list. It is clear to you that the business cannot function without an intranet these...

-

A local government agency has asked you to consult regarding acquisition of land for recreation needs for the urban area. The following data are provided: Urban population 10 years ago 49,050 Urban...

-

The Pen, Evan, and Torves Partnership has asked you to assist in winding-up its business affairs. You compile the following information. 1. The partnerships trial balance on June 30, 20X1, is 2. The...

-

An interest payment of $650 in a 20 percent tax bracket would result in a tax savings of _____.

-

1. Suppose that the landlord had made good faith efforts to fix the problem, but was unable to for a period of three months. Would that change the outcome of the case? 2. The court noted that tenants...

-

Grant Industries, a manufacturer of electronic parts, has recently received an invitation to bid on a special order for 20,000 units of one of its most popular products. Grant currently manufactures...

-

What are multilateral trading platforms?

-

On September 30, 2012, Synergy Bank loaned $88,000 to Kendall Kelsing on a oneyear, 12% note. Requirements 1. Journalize all entries for Synergy Bank related to the note for 2012 and 2013. 2. Which...

-

An essay on any favorite product about the value chain

-

Note 3 describes Cisco's 2013 acquisition of NDS Group Limited (NDS") for cash totaling $5,005 million and reports the allocation of the purchase price to specific asset and liability accounts. i....

-

Section 3 Personal Development Plan for the year ahead (i.e. twelve months following submission of your portfolio). What do I want/need to Learn. Be specific. What will I do to achieve this?...

-

1. Jerseys, Inc., currently produces 10,000 jerseys a year for its regular customers and charges $10 per jersey. Jerseys, Inc., has capacity to produce an additional 5,000 jerseys if sales grow in...

-

Common Pollution Policy grant of 20 per cent of gross capital expenditure is available, with payment in the year following expenditure. A disadvantage of the new equipment is that it will raise...

-

Q1 Saturn PLC Saturn PLC is considering a capital investment of 2,500,000 in new, state of the art equipment, with a resale value of 750,000 in 3 years' time. The equipment will be used to...

-

In 2020, X Corporation contributed 100 shares of Y corporation stock to a qualified charity. The FMV of the stock was $100,000 and adjusted basis was $40,000. In 2022, X contributed 15,000 cash to a...

-

Private Equity Associates ("Associates") is a limited partnership that buys, restructures, and then sells companies that are not publicly traded. Manager, the sole general partner of Associates, is...

-

Conduct a univariate analysis on the variables in the attached database and report your results in the format you deem most appropriate--either written up in an MS Word document or a recorded Zoom...

-

Pastel Corporation acquired a controlling interest in Somber Corporation in 20X5 for an amount equal to its underlying book value. At the date of acquisition, the fair value of the noncontrolling...

-

Becon Corporations controller has just finished preparing a consolidated balance sheet, income statement, and statement of changes in retained earnings for the year ended December 31, 20X4. Becon...

-

Foster Corporation established Kline Company as a wholly owned subsidiary. Foster reported the following balance sheet amounts immediately before and after it transferred assets and accounts payable...

-

Using Rules 5.1, show that if \(x>0\) and \(y <0\) then \(x y <0\), and that if \(a>b>0\) then \(\frac{1}{a}

-

For which values of \(x\) is \(x^{2}+x+1 \geq \frac{x-1}{2 x-1}\) ?

-

For which values of \(x\) is \(-3 x^{2}+4 x>1\) ?

Study smarter with the SolutionInn App