Activity-based costing, oh-costing system. The Hewlett-Packard (HP) plant in Roseville, California, operates at capacity and assembles and

Question:

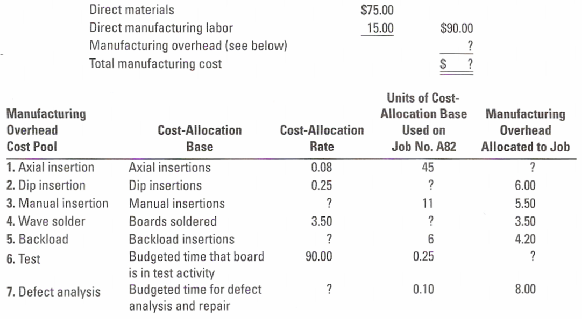

Activity-based costing, oh-costing system. The Hewlett-Packard (HP) plant in Roseville, California, operates at capacity and assembles and tests printed-circuit (PC) boards. The job-costing system at this plant has two direct-cost categories (direct materials and direct manufacturing labor) and seven indirect cost pools. These indirect-cost pools represent the seven activity areas that operating personnel at the plant determined are sufficiently different (in terms of cost-behavior patterns or individual products being assembled) to warrant separate cost pools. The cost-allocation base chosen for each activity area is the cost driver at that activity area.

Debbie Berlant, a newly appointed marketing manager at HP, is attending a training session that describes how an activity-based costing approach was used to design the Roseville plant’s job-costing system. Berlant is provided with the following incomplete information for a specific job (an order for a single PC board, No. A82):

1. Prepare an overview diagram of the activity-based job-costing system at the Roseville plant.

2. Fill in the blanks (noted by question marks) in the cost information provided to Berlant for Job No. A82.

3. Why might manufacturing managers and marketing managers favor this ABC job-costing system over the simple costing system, which had the same two direct-cost categories but only a single indirect- cost pool (manufacturing overhead allocated using direct manufacturing labor costs)?

Step by Step Answer:

Activitybased costing jobcosting system 1 An overview of the activitybased jobcosting system is 2 Di...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0136126638

13th Edition

Authors: Charles T. Horngren, Srikant M.Dater, George Foster, Madhav