Designing a Balanced Scorecard for a pharmaceutical company Chadwick, Inc.: The Balanced Scorecard (Abridged)14 Company Background Chadwick,

Question:

Designing a Balanced Scorecard for a pharmaceutical company Chadwick, Inc.: The Balanced Scorecard (Abridged)14

Company Background

Chadwick, Inc., was a diversified producer of personal consumer products and pharmaceuticals. The Norwalk Division of Chadwick developed, manufactured, and sold ethical drugs for human and animal use. It was one of five or six sizable companies competing in these markets and, while it did not dominate the industry, the company was considered well managed and was respected for the high quality of its products. Norwalk did not compete by supplying a full range of products. It specialized in several niches and attempted to leverage its product line by continually searching for new applications for existing compounds.

Norwalk sold its products through several key distributors who supplied local markets, such as retail stores, hospitals and health service organizations, and veterinary practices. Norwalk depended on its excellent relations with the distributors who served to promote Norwalk's products to end users and also received feedback from the end users about new products desired by their customers.

Chadwick knew that its long-term success depended on how much money distributors could make by promoting and selling Norwalk's products. If the profit from selling Norwalk products was high, then these products were promoted heavily by the distributors and Norwalk received extensive communication back about future customer needs. Norwalk had historically provided many highly profitable products to the marketplace, but recent inroads by generic manufacturers had been eroding distributors' sales and profit margins. Norwalk had been successful in the past because of its track record of generating a steady stream of attractive, popular products. During the second half of the 1980s, however, the approval process for new products had lengthened and fewer big winners had emerged from Norwalk's R&D laboratories.

Research and Development

The development of ethical drugs was a lengthy, costly, and unpredictable process. Development cycles now averaged about 12 years. The process started by screening a large number of compounds for potential benefits and use. For every drug that finally emerged as approved for use, up to 30,000 compounds had to be tested at the beginning of a new product development cycle. The development and testing processes had many stages. The development cycle started with the discovery of compounds that possessed the desirable properties and ended many years later with extensive and tedious testing and documentation to demonstrate that the new drug could meet government regulations for promised benefits, reliability in production, and absence of deleterious side effects.

Approved and patented drugs could generate enormous revenues for Norwalk and its distributors. Norwalk's profitability during the 1980s was sustained by one key drug that had been discovered in the late 1960s. No blockbuster drug had emerged during the 1980s, however, and the existing pipeline of compounds going through development, evaluation, and test was not as healthy as Norwalk management desired. Management was placing pressure on scientists in the R&D lab to increase the yield of promising new products and to reduce the time and costs of the product development cycle. Scientists were currently exploring new bioengineering techniques to create compounds that had the specific active properties desired rather than depending on an almost random search through thousands of possible compounds. The new techniques started with a detailed specification of the chemical properties that a new drug should have and then attempted to synthesize candidate compounds that could be tested for these properties. The bioengineering procedures were costly, requiring extensive investment in new equipment and computer-based analyses.

A less expensive approach to increase the financial yield from R&D investments was to identify new applications for existing compounds that had already been approved for use. While some validation still had to be submitted for government approval to demonstrate the effectiveness of the drug in the new applications, the cost of extending an existing product to a new application was much, much less expensive than developing and creating an entirely new compound. Several valuable suggestions for possible new applications from existing products had come from Norwalk salesmen in the field. The salesmen were now being trained not only to sell existing products for approved applications, but also to listen to end users who frequently had novel and interesting ideas about how Norwalk's products could be used for new applications. Manufacturing

Norwalk's manufacturing processes were considered among the best in the industry. Management took pride in the ability of the manufacturing operation to quickly and efficiently ramp up to produce drugs once they had cleared governmental regulatory processes. Norwalk's manufacturing capabilities also had to produce the small batches of new products that were required during testing and evaluation stages.

Performance Measurement

Chadwick allowed its several divisions to operate in a decentralized fashion. Division managers had almost complete discretion in managing all the critical processes: R&D, production, marketing and sales, and administrative functions such as finance, human resources, and legal. Chadwick set challenging financial targets for divisions to meet. The targets were usually expressed as return on capital employed (ROCE). As a diversified company, Chadwick wanted to be able to deploy the returns from the most profitable divisions to those divisions that held out the highest promise for profitable growth. Monthly financial summaries were submitted by each division to corporate headquarters. The Chadwick executive committee, consisting of the chief executive officer, the chief operating officer, two executive vice presidents, and the chief financial officer met monthly with each division manager to review ROCE performance and backup financial information for the preceding month.

The Balanced Scorecard Project

Bill Baron, comptroller of Chadwick, had been searching for improved methods for evaluating the performance of the various divisions. Division managers complained about the continual pressure to meet short-term financial objectives in businesses that required extensive investments in risky projects to yield long-term returns. The idea of a Balanced Scorecard appealed to him as a constructive way to balance short-run financial objectives with the long-term performance of the company.

Baron brought the article and concept to Dan Daniels, the president and chief operating officer of Chadwick. Daniels shared Baron's enthusiasm for the concept, feeling that a Balanced Scorecard would allow Chadwick divisional managers more flexibility in how they measured and presented their results of operations to corporate management. He also liked the idea of holding managers accountable for improving the long-term performance of their division.

After several days of reflection, Daniels issued a memorandum to all Chadwick division managers. The memo had a simple and direct message: Read the Balanced Scorecard article, develop a scorecard for your division, and be prepared to come to corporate headquarters in 90 days to present and defend the divisional scorecard to Chadwick's executive committee.

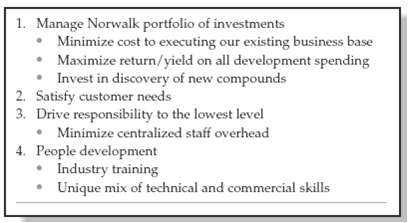

John Greenfield, the division manager at Norwalk, received Daniel's memorandum with some concern and apprehension. In principle, Greenfield liked the idea of developing a scorecard that would be more responsive to his operations, but he was distrustful of how much freedom he had to develop and use such a scorecard. Greenfield recalled:

This seemed like just another way for corporate to claim that they have decentralized decision making and authority while still retaining ultimate control at headquarters.

Greenfield knew that he would have to develop a plan of action to meet corporate's request but lacking a clear sense of how committed Chadwick was to the concept, he was not prepared to take much time from his or his subordinates' existing responsibilities for the project.

The next day, at the weekly meeting of the Divisional Operating Committee, Greenfield distributed the Daniels memo and appointed a three-man committee, headed by the divisional controller, Wil Wagner, to facilitate the process for creating the Norwalk Balanced Scorecard. Wagner approached Greenfield later that day:

I read the Balanced Scorecard article. Based on my understanding of the concept, we must start with a clearly defined business vision. I'm not sure I have a clear understanding of the vision and business strategy for Norwalk. How can I start to build the scorecard without this understanding? Greenfield admitted: "That's a valid point. Let me see what I can do to get you started."

Required(a) How does the Balanced Scorecard approach differ from traditional approaches to performance measurement? What, if anything, distinguishes the Balanced Scorecard approach from a "measure everything, and you might get what you want" philosophy?(b) Develop the Balanced Scorecard for the Norwalk Pharmaceutical Division of Chadwick, Inc. What parts of the business strategy that John Greenfield sketched out should be included? Are there any parts that should be excluded or cannot be made operational? What scorecard measures would you use to implement your scorecard in the Norwalk Pharmaceutical Division? What new measures need to be developed, and how would you go about developing them?(c) How would a Balanced Scorecard for Chadwick, Inc., differ from ones developed in its divisions, such as the Norwalk Pharmaceutical Division? Do you anticipate that there might be major conflicts between divisional scorecards and those of the corporation? If so, should those conflicts be resolved, and, if so, how should they be resolved?

Step by Step Answer:

Substantive Issues Raised Division managers at Chadwick had complained to the Controller about the continual pressure to meet shortterm financial objectives As a producer of consumer products and phar...View the full answer

Management Accounting Information for Decision-Making and Strategy Execution

ISBN: 978-0137024971

6th Edition

Authors: Anthony A. Atkinson, Robert S. Kaplan, Ella Mae Matsumura, S. Mark Young