1. Which of the following best describes the recommended format for the government-wide statement of activities? a....

Question:

a. Revenues minus expenses equals change in net position.

b. Revenues minus expenditures and outstanding encumbrances equals change in net position.

c. Expenses minus program revenues equals net (expense) revenue. Net (expense) revenue plus general revenues equals change in net position.

d. Program revenues minus expenses minus general revenues equals changes in net position.

2. Which of the following is an acceptable method of reporting depreciation expense for depreciable assets used by governmental activities?

a. Report as a general expense in the bottom section of the statement of activities.

b. Report as a direct expense of the function or program with which the related depreciable assets are identified.

c. Report as an indirect expense on a separate line if the depreciable assets benefit all functions or programs.

d. Either b or c.

3. Which of the following accounts neither increases nor decreases the fund balance of the General Fund during the fiscal year?

a. Expenditures.

b. Revenues.

c. Encumbrances.

d. Other financing sources.

4. When determining taxable property for the purpose of the property tax levy, which of the following would likely be excluded from the calculation?

a. Property owned by governments.

b. Property exempted from taxation by the government.

c. Property used by religious or charitable organizations.

d. All of the above.

5. Which of the following statements is true for other financing uses but is not true for expenditures?

a. Arise from interfund transfers out.

b. Decrease fund balances when they are closed at year-end.

c. Are included on the budgetary comparison schedule.

d. Have normal debit balances.

6. An internal allocation of funds on a periodic basis, which is often used to regulate the use of appropriations over a budgetary period, is called

a. An encumbrance.

b. A budgetary levy.

c. An ad valorem assessment.

d. An allotment.

7. According to GASB standards, expenditures are classified by

a. Fund, function or program, organization unit, source, and character.

b. Fund, function or program, organization unit, activity, character, and object.

c. Fund, appropriation, organization unit, activity, character, and object.

d. Fund, organization unit, encumbrance, activity, character, and object.

8. Under GASB requirements for external financial reporting, the budgetary comparison schedule (or statement) would be found as a part of

a. Required supplementary information (RSI).

b. Basic financial statements.

c. Note disclosures.

d. Either a or b, as elected by the government.

9. Before placing a purchase order, a department should check that available appropriations are sufficient to cover the cost of the item being ordered. This type of budgetary control is achieved by reviewing

a. Appropriations minus expenditures.

b. Appropriations plus expenditures minus outstanding encumbrances.

c. Appropriations minus the sum of expenditures and outstanding encumbrances.

d. Appropriations minus estimated revenues.

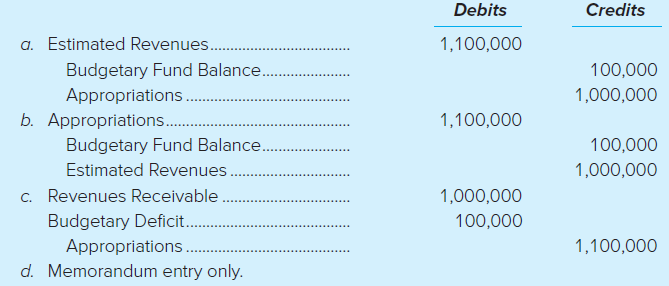

10. Spruce City€™s finance department recorded the recently adopted General Fund budget at the beginning of the current fiscal year. The budget approved estimated revenues of $1,100,000 and appropriations of $1,000,000. Which of the following is the correct journal entry to record the budget?

11. Which of the following is correct concerning the presentation of the budgetary comparison schedule?

11. Which of the following is correct concerning the presentation of the budgetary comparison schedule?

a. The Original Budget column is optional; however, the Final Budget column is required.

b. The Variance column is required.

c. The Actual column is required to be presented using the government€™s budgetary basis of accounting.

d. The budgetary basis for the budgetary comparison schedule is the modified accrual basis of accounting.

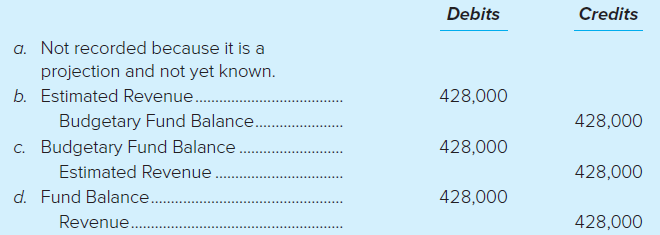

12. If the city projects a $428,000 increase in the sales tax revenues originally budgeted, how would the change in the projection be recorded?

13. If it is in accordance with the government€™s policies, which of the following budgetary accounts can remain open at the fiscal year-end?

a. Appropriations.

b. Estimated Other Financing Sources.

c. Budgetary Fund Balance.

d. Encumbrances.

14. Which of the following best identifies when an encumbrance is recorded?

a. When goods or services are received.

b. When an obligation is incurred that will be paid from current financial resources.

c. When legislative authority has been granted to spend resources.

d. When goods or services are ordered.

15. Supplies ordered by the Public Works function of the General Fund were received at an actual price that was less than the estimated price listed on the purchase order. What effect will this have on Public Work€™s appropriations available balance?

a. Increase.

b. Decrease.

c. No effect.

d. Insufficient information to determine the effect.

Step by Step Answer:

1 c 2 d 3 c 4 ...View the full answer

Accounting for Governmental and Nonprofit Entities

ISBN: 978-1259917059

18th edition

Authors: Jacqueline L. Reck, James E. Rooks, Suzanne Lowensohn, Daniel Neely