In 20X0, the cereal division of Bloom Company (a fictional company) decided to test market in 20X1

Question:

In 20X0, the cereal division of Bloom Company (a fictional company) decided to test market in 20X1 an organic corn-based cereal to be called Healthcrisp. The business plan calls for production to begin in late May 20X1, with retail store delivery starting in early June. Madeleine Elster, the marketing brand manager with overall responsibility for the product, has identified 15 metropolitan areas in the upper Midwest of the United States where organic foods already capture a large share of the consumer wallet.

Healthcrisp will be manufactured and distributed using existing technologies and facilities. Bloom has entered into long-term contracts for organic corn with producers located in close proximity to these manufacturing sites. The contracts specify the amount (in bushels) of organic corn to be delivered at each site monthly from May through December 20X1, when the market test ends. The price to be paid by Bloom is not contractually specified, but will instead be determined by market conditions at the time of delivery.

Bloom is not the first company to offer consumers an organic corn-based breakfast cereal. Organic corn flake cereals available currently in the designated test markets sell at the retail level for between $10 and $14 per 11 oz. box. The Healthcrisp business plan calls for the retailer to pay Bloom $9 for each 11 oz. box. The retailer then adds a $5 markup and the consumer pays $14 per box. Elster believes that Bloom’s strong brand awareness and reputation for high-quality, nutritional breakfast products justifies the high-end price point for Healthcrisp. Elter’s business plan calls for the wholesale price to remain constant for the duration of the test market.

Two features of the Healthcrisp business plan expose Bloom to the financial risk that organic corn prices might increase substantially during the test market production run: (1) Bloom will receive a fixed dollar amount ($9) for each box of Healthcrisp sold but (2) must pay the corn growers a price that is only determined upon delivery. There is no organized market for organic corn—buyers such as Bloom must negotiate price and other contract terms directly with each local grower. There is, however, an active market for traditional (nonorganic) corn at the Chicago Board of Trade (CBT), where standardized futures contracts for common corn are traded on a daily basis. Briefly, each corn futures contract entails:

• The right to take delivery of 5,000 bushels (≈127 metric tons) of common corn at a pre-designated location. To put this amount in perspective, a typical railroad grain car can hold between 3,200 and 3,500 U.S. bushels depending on the kernel size and weight.

• Delivery occurs on the second business day following the last trading day of the delivery month. This means that the buyer of a December 20X0 contract either must accept delivery of the 5,000 bushels on Thursday, January 3, 20X1, or sell (cancel) the contract before the close of trading on December 31, 20X0.

• Costs of transporting the corn from the designated delivery location to the buyer’s facilities are not included in the quoted CBT contract price and are the responsibility of the buyer.

• The price of a contract is quoted in cents per bushel; e.g., a price of say “743” is understood to mean $7.43 per bushel or $37,150 per contract.

Large fluctuations in common corn production can occur from one year to the next. Consequently, corn futures contract prices on the CBT tend to be quite volatile during the growing and harvesting season, which for the upper Midwest is May through October. One important factor contributing to this volatility is the unpredictability of weather during the growing and harvesting season and its impact on corn production.

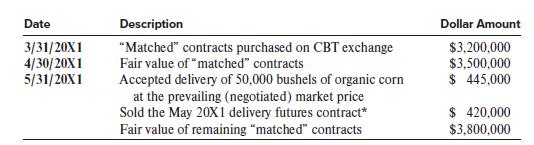

The corporate finance group at Bloom has decided to hedge its exposure to fluctuations in the price of organic corn needed for Healthcrisp by purchasing several common corn futures contracts on the CBT. These futures contracts are “matched” in bushel amount and delivery month to the amount and timing of organic corn required for the Healthcrisp test market production run. The following table provides information about several transactions related to the company’s purchase of organic corn and to this hedge:

Required:

1. Explain why Bloom’s corn price hedge is only partially effective?

2. Explain why the Bloom hedge qualifies for special GAAP “hedge accounting” treatment by describing the eligible market risk being hedged, the required accounting approach (fair value hedge, cash flow hedge, or foreign currency hedge), and why that accounting treatment is appropriate. You should assume that the hedge is sufficiently effective to qualify for GAAP hedge accounting treatment.

3. Prepare journal entries to reflect the purchase of the “matched” CBT corn futures contracts on March 31, 20X1, and the fair value of those contracts on April 30.

4. Prepare general journal entries to reflect the May 31 transactions and events.

5. Explain in words and numbers the economic benefit (if any) of the hedge to Bloom over the period from March 31 through May 31.

6. Suppose corn futures prices (and thus the hedge fair value) had moved in the direction opposite to that shown in the table. Explain in words the economic cost (if any) of the hedge to Bloom over the same period.

Step by Step Answer:

Requirement 1 Notice that the nonorganic corn futures contracts are exactly matched in bushel amount and delivery month to the companys anticipated purchases of organic corn This sort of matching woul...View the full answer

Financial Reporting And Analysis

ISBN: 9781260247848

8th Edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer