Question:

Assume it is Monday, May 1, 2020, the first business day of the month, and you have just been hired as the accountant for Alpine Company, which operates with monthly accounting periods. All of the company?s accounting work has been completed through the end of April and its ledgers show April 30 balances. Alpine uses a perpetual system to account for inventory. The terms of all credit sales are 2/10, n/30. During your first month on the job, you record the following transactions on page 2 of each journal.

If the Working Papers that accompany this textbook are not being used, the forms needed to complete this problem are available on Connect.

Required

1. Enter the transactions in the appropriate journals and post when instructed to do so.

2. Prepare a trial balance in the Trial Balance columns of the provided work sheet form and complete the work sheet using the following information.

a. Expired insurance, $553.

b. Ending store supplies inventory, $2,632.

c. Ending office supplies inventory, $504.

d. Estimated depreciation of store equipment, $567.

e. Estimated depreciation of office equipment, $329.

f. Ending merchandise inventory, $191,000.

3. Prepare a May classified, multiple-step income statement, a May statement of changes in equity, and a May 31 classified balance sheet.

4. Prepare and post adjusting and closing entries (omit explanations).

5. Prepare a post-closing trial balance. Also prepare a list of the accounts receivable subledger accounts and a list of the accounts payable subledger accounts.

Accounts Payable

Accounts payable (AP) are bills to be paid as part of the normal course of business.This is a standard accounting term, one of the most common liabilities, which normally appears in the balance sheet listing of liabilities. Businesses receive...

Accounts Receivable

Accounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that...

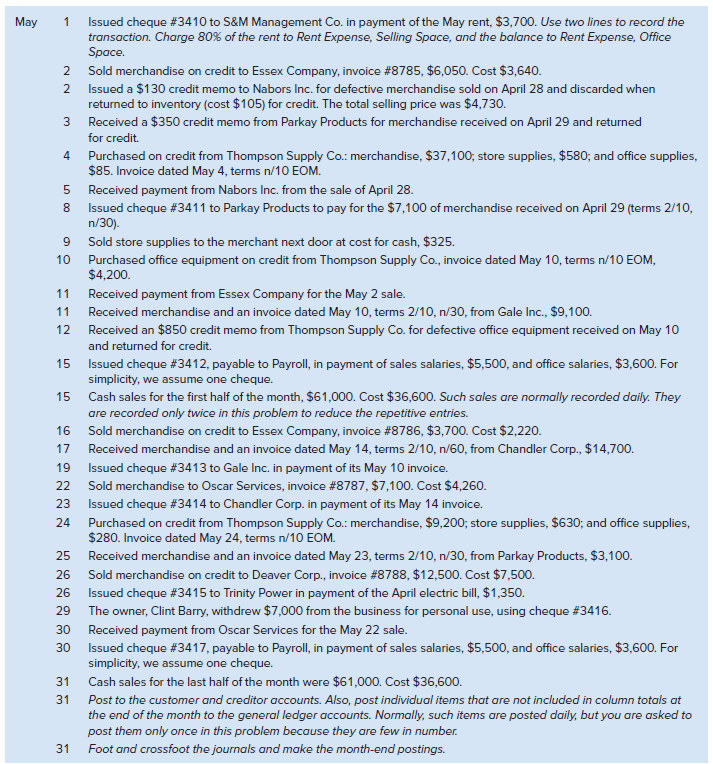

Transcribed Image Text:

Issued cheque #3410 to S&M Management Co. in payment of the May rent, $3,700. Use two lines to record the transaction. Charge 80% of the rent to Rent Expense, Selling Space, and the balance to Rent Expense, Office Space. May Sold merchandise on credit to Essex Company, invoice #8785, $6,050. Cost $3,640. Issued a $130 credit memo to Nabors Inc. for defective merchandise sold on April 28 and discarded when returned to inventory (cost $105) for credit. The total selling price was $4,730. Received a $350 credit memo from Parkay Products for merchandise received on April 29 and returned for credit. Purchased on credit from Thompson Supply Co.: merchandise, $37,100; store supplies, $580; and office supplies, $85. Invoice dated May 4, terms n/10 EOM. 4 Received payment from Nabors Inc. from the sale of April 28. Issued cheque #3411 to Parkay Products to pay for the $7,100 of merchandise received on April 29 (terms 2/10, n/30). Sold store supplies to the merchant next door at cost for cash, $325. 10 Purchased office equipment on credit from Thompson Supply Co., invoice dated May 10, terms n/10 EOM, $4,200. 11 Received payment from Essex Company for the May 2 sale. Received merchandise and an invoice dated May 10, terms 2/10, n/30, from Gale Inc., $9,100. Received an $850 credit memo from Thompson Supply Co. for defective office equipment received on May 10 11 12 and returned for credit. Issued cheque #3412, payable to Payroll, in payment of sales salaries, $5,500, and office salaries, $3,600. For simplicity, we assume one cheque. 15 Cash sales for the first half of the month, $61,000. Cost $36,600. Such sales are normally recorded daily. They are recorded only twice in this problem to reduce the repetitive entries. 15 Sold merchandise on credit to Essex Company, invoice #8786, $3,700. Cost $2,220. Received merchandise and an invoice dated May 14, terms 2/10, n/60, from Chandler Corp., $14,700. 16 17 19 Issued cheque #3413 to Gale Inc. in payment of its May 10 invoice. Sold merchandise to Oscar Services, invoice #8787, $7,100. Cost $4,260. 22 23 Issued cheque #3414 to Chandler Corp. in payment of its May 14 invoice. Purchased on credit from Thompson Supply Co.: merchandise, $9,200; store supplies, $630; and office supplies, $280. Invoice dated May 24, terms n/10 EOM. Received merchandise and an invoice dated May 23, terms 2/10, n/30, from Parkay Products, $3,100. 24 25 Sold merchandise on credit to Deaver Corp., invoice #8788, $12,500. Cost $7,500. 26 Issued cheque #3415 to Trinity Power in payment of the April electric bill, $1,350. 26 The owner, Clint Barry, withdrew $7,000 from the business for personal use, using cheque #3416. 29 30 Received payment from Oscar Services for the May 22 sale. Issued cheque #3417, payable to Payroll, in payment of sales salaries, $5,500, and office salaries, $3,600. For simplicity, we assume one cheque. 30 Cash sales for the last half of the month were $61,000. Cost $36,600. 31 31 Post to the customer and creditor accounts. Also, post individual items that are not included in column totals at the end of the month to the general ledger accounts. Normally, such items are posted daily, but you are asked to post them only once in this problem because they are few in number. Foot and crossfoot the journals and make the month-end postings. 31