Companies often buy bonds to meet a future liability or cash outlay. Such an investment is called

Question:

Companies often buy bonds to meet a future liability or cash outlay. Such an investment is called a dedicated portfolio because the proceeds of the portfolio are dedicated to the future liability. In such a case, the portfolio is subject to reinvestment risk. Reinvestment risk occurs because the company will be reinvesting the coupon payments it receives. If the YTM on similar bonds falls, these coupon payments will be reinvested at a lower interest rate, which will result in a portfolio value that is lower than desired at maturity. Of course, if interest rates increase, the portfolio value at maturity will be higher than needed.

Suppose Ice Cubes, Inc., has the following liability due in five years. The company is going to buy five-year bonds today to meet the future obligation. The liability and current YTM are below.

Amount of liability: ......... $100,000,000%Current YTM: ........................................ 8%

a. At the current YTM, what is the face value of the bonds the company has to purchase today to meet its future obligation? Assume that the bonds in the relevant range will have the same coupon rate as the current YTM and these bonds make semiannual coupon payments.

b. Assume that the interest rates remain constant for the next five years. Thus, when the company reinvests the coupon payments, it will reinvest at the current YTM. What is the value of the portfolio in five years?

c. Assume that immediately after the company purchases the bonds, interest rates either rise or fall by 1 percent. What is the value of the portfolio in five years under these circumstances?

One way to eliminate reinvestment risk is called immunization. Rather than buying bonds with the same maturity as the liability, the company instead buys bonds with the same duration as the liability. If you think about the dedicated portfolio, if the interest rate falls, the future value of the reinvested coupon payments decreases. However, as interest rates fall, the price of the bond increases. These effects offset each other in an immunized portfolio.

Another advantage of using duration to immunize a portfolio is that the duration of a portfolio is the weighted average of the duration of the assets in the portfolio. In other words, to find the duration of a portfolio, you take the weight of each asset multiplied by its duration and then sum the results.

d. What is the duration of the liability for Ice Cubes, Inc.?

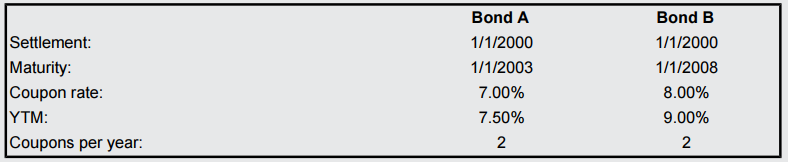

e. Suppose the two bonds shown below are the only bonds available to immunize the liability. What face amount of each bond will the company need to purchase to immunize the portfolio?

Face value is a financial term used to describe the nominal or dollar value of a security, as stated by its issuer. For stocks, the face value is the original cost of the stock, as listed on the certificate. For bonds, it is the amount paid to the... Future Value

Future value (FV) is the value of a current asset at a future date based on an assumed rate of growth. The future value (FV) is important to investors and financial planners as they use it to estimate how much an investment made today will be worth... Portfolio

A portfolio is a grouping of financial assets such as stocks, bonds, commodities, currencies and cash equivalents, as well as their fund counterparts, including mutual, exchange-traded and closed funds. A portfolio can also consist of non-publicly...

Step by Step Answer:

a The face value of the bonds the company has to purchase today to meet its future obligation is 100 000 000 This is calculated by taking the amount o...View the full answer

Fundamentals of Corporate Finance

ISBN: 978-1260153590

12th edition

Authors: Stephen M. Ross, Randolph W Westerfield, Robert R. Dockson, Bradford D Jordan