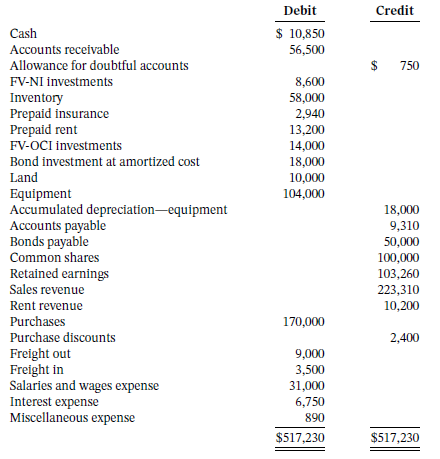

The unadjusted trial balance of Imagine Ltd., a private company following ASPE, at December 31, 2020 is

Question:

The unadjusted trial balance of Imagine Ltd., a private company following ASPE, at December 31, 2020 is as follows:

Additional information:

1. On November 1, 2020, Imagine received $10,200 rent from its lessee for a 12-month lease beginning on that date. This was credited to Rent Revenue.

2. Imagine estimates that 7% of the Accounts Receivable balances on December 31, 2020, will be uncollectible.

On December 28, 2020, the bookkeeper incorrectly credited Sales Revenue for a receipt of $1,000 on account. This error had not yet been corrected on December 31.

3. After a physical count, inventory on hand at December 31, 2020, was $77,000.

4. Prepaid insurance contains the premium costs of two policies: Policy A, cost of $1,320, two-year term, taken out on April 1, 2020; Policy B, cost of $1,620, three-year term, taken out on September 1, 2020.

5. The regular rate of depreciation is 10% of cost per year. Acquisitions and retirements during a year are depreciated at half this rate. There were no retirements during the year. On December 31, 2019, the balance of Equipment was $90,000.

6. On April 1, 2020, Imagine issued at par value 50 $1,000, 11% bonds maturing on April 1, 2024. Interest is paid on April 1 and October 1.

7. On August 1, 2020, Imagine purchased at par value 18 $1,000, 12% Legume Inc. bonds, maturing on July 31, 2022. Interest is paid on July 31 and January 31.

8. On May 30, 2020, Imagine rented a warehouse for $1,100 per month and debited Prepaid Rent for an advance payment of $13,200.

9. Imagine?s FV-NI investments consist of shares with total market value of $9,400 as at December 31, 2020.

10. The FV-OCI investment is an investment of 500 shares in Yop Inc., with current market value of $25 per share as at December 31, 2020.

Instructions

a. Prepare the year-end adjusting and correcting entries for December 31, 2020, using the information given. Record the adjusting entry for inventory using a Cost of Goods Sold account.

b. Indicate which of the adjusting entries could be reversed.

Par ValuePar value is the face value of a bond. Par value is important for a bond or fixed-income instrument because it determines its maturity value as well as the dollar value of coupon payments. The market price of a bond may be above or below par,...

Step by Step Answer:

a Adjust ing Ent ries 1 Allow ance for Dou bt ful Accounts ...View the full answer

Intermediate Accounting Volume 2

ISBN: 9781119497042

12th Canadian Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy