On 1 April 20X1, Picant acquired 75 per cent of Sanders equity shares in a share exchange

Question:

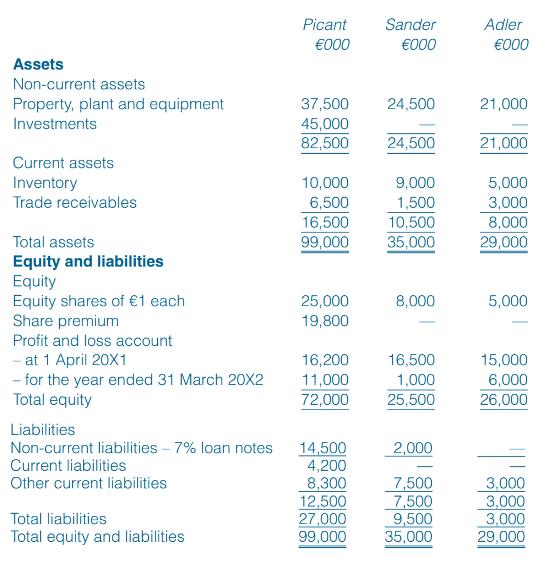

On 1 April 20X1, Picant acquired 75 per cent of Sander’s equity shares in a share exchange of three shares in Picant for every two shares in Sander. The market prices of Picant’s and Sander’s shares at the date of acquisition were €3.20 and €4.50 respectively. In addition to this, Picant agreed to pay a further amount on 1 April 20X2 that was contingent upon the post-acquisition performance of Sander. At the date of acquisition, Picant assessed the fair value of this contingent consideration at €4.2m, but by 31 March 20X2 it was clear that the actual amount to be paid would be only €2.7m (ignore discounting). Picant has recorded the share exchange and provided for the initial estimate of €4.2m for the contingent consideration. On 1 October 20X1, Picant also acquired 40 per cent of the equity shares of Adler paying €4 in cash per acquired share and issuing at par one €100 7 per cent loan note for every 50 acquired shares in Adler. This consideration has also been recorded by Picant. Picant has no other investments. The summarized statements of financial position of the three companies at 31 March 20X2 are:

The following information is relevant:

The following information is relevant:

(i) At the date of acquisition, the fair values of Sander’s property, plant and equipment were equal to their carrying amounts with the exception of Sander’s factory which had a fair value of €2m above its carrying amount. Sander has not adjusted the carrying amount of the factory as a result of the fair value exercise. This requires additional annual depreciation of €100,000 in the consolidated financial statements in the post-acquisition period. Also, at the date of acquisition, Sander had an intangible asset of €500,000 for software in its balance sheet. Picant’s directors believed the software to have no recoverable value at the date of acquisition and Sander wrote it off shortly after its acquisition.

(ii) At 31 March 20X2, Picant’s current account with Sander was €3.4m (debit). This did not agree with the equivalent balance in Sander’s books due to some goods-in-transit invoiced at €1.8m that were sent by Picant on 28 March 20X2 but had not been received by Sander until after the year end. Picant sold these goods at cost plus 50 per cent.

(iii) Impairment tests were carried out on 31 March 20X2. It was identified that the value of the investment in Adler was not impaired but, due to poor trading performance, the consolidated goodwill was impaired by €2.7 million.

(iv) Assume all profits accrue evenly through the year.

Required:

Prepare the consolidated statement of financial position for Picant as at 31 March 20X2.

(b) Picant has been approached by a potential new customer, Trilby, to supply it with a substantial quantity of goods on three months’ credit terms. Picant is concerned at the risk that such a large order represents in the current difficult economic climate, especially as Picant’s normal credit terms are only one month’s credit. To support its application for credit, Trilby has sent Picant a copy of Tradhat’s most recent audited consolidated financial statements. Trilby is a wholly owned subsidiary within the Tradhat group. Tradhat’s consolidated financial statements show a strong statement of financial position including healthy liquidity ratios.

Required:

Comment on the importance that Picant should attach to Tradhat’s consolidated financial statements when deciding on whether to grant credit terms to Trilby.

Step by Step Answer:

ANSWER To prepare the consolidated statement of financial position for Picant as at 31 March 20X2 we need to first adjust the assets liabilities and e...View the full answer

International Financial Reporting And Analysis

ISBN: 9781473766853

8th Edition

Authors: David Alexander, Ann Jorissen, Martin Hoogendoorn