Victor Holt, the accounting manager of Sexton, Inc., gathered the following information for 2014. Some of it

Question:

Victor Holt, the accounting manager of Sexton, Inc., gathered the following information for 2014. Some of it can be used to construct an income statement for 2014. Ignore items that do not appear on an income statement. Some computation may be required. For example, the cost of manufacturing equipment would not appear on the income statement. However, the cost of manufacturing equipment is needed to compute the amount of depreciation. All units of product were started and completed in 2014.

1. Issued $864,000 of common stock.

2. Paid engineers in the product design department S10,000 for salaries that were accrued at the end of the previous year.

3. Incurred advertising expenses of $70,000.

4. Paid $720,000 for materials used to manufacture the company’s product.

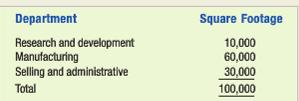

5. Incurred utility costs of $160,000. These costs were allocated to different departments on the basis of square footage of floor space. Mr. Holt identified three departments and determined the square footage of floor space for each department to be as shown in the table below.

6. Paid $880,000 for wages of production workers.

7. Paid cash of $658,000 for salaries of administrative personnel. There was $16,000 of accrued salaries owed to administrative personnel at the end of 2014. There was no beginning balance in the Salaries Payable account for administrative personnel.

8. Purchased manufacturing equipment two years ago at a cost of S 10,000,000. The equipment had an eight-year useful life and a $2,000,000 salvage value.

9. Paid $390,000 cash to engineers in the product design department.

10. Paid a $258,000 cash dividend to owners.

11. Paid $80,000 to set up manufacturing equipment for production.

12. Paid a one-time Sl 86,000 restructuring cost to redesign the production process to implement a just-in-time inventory system.

13. Prepaid the premium on a new insurance policy covering non manufacturing employees. The policy cost $72,000 and had a one-year terni with an effective starting date of May I. Four employees work in the research and development department and eight employees work in the selling and administrative department. Assume a December 31 closing date.

14. Made 69,400 units of product and sold 60,000 units at a price of $70 each.

11. Paid $80,000 to set up manufacturing equipment for production.

12. Paid a one-time SI 86.000 restructuring cost to redesign the production process to implement

a just-in-time inventory system.

13. Prepaid the premium on a new insurance policy covering nonmanufacturing employees. The

policy cost $72,000 and had a one-year term with an effective starting date of May I. Four

employees work in the research and development department and eight employees work in

the selling and administrative department. Assume a December 31 closing date.

14. Made 69,400 units of product and sold 60,000 units at a price of $70 each.

Required

a. Divide the class into groups of four or five students per group, and then organize the groups into three sections. Assign Task I to the first section of groups, Task 2 to the second section of groups, and Task 3 to the third section of groups.

Group Tasks

(1) Identify the items that are classified as product costs and determine the amount of cost of goods sold reported on the 2014 income statement.

(2) Identify the items that are classified as upstream costs and determine the amount of upstream cost expensed on the 2014 income statement.

(3) Identify the items that are classified as downstream costs and determine the amount of downstream cost expensed on the 2014 income statement.

b. Have the class construct an income statement in the following manner. Select a member of one of the groups assigned Group Task (I), identifying the product costs. Have that person go to the board and list the costs included in the determination of cost of goods sold. Anyone in the other groups who disagrees with one of the classifications provided by the person at the board should voice an objection and explain why the item should be classified differently. The instructor should lead the class to a consensus on the disputed ìtems After the amount of cost of goods sold is determined, the student at the board constructs the part of the income statement showing the determination of gross margin. The exercise continues in a similar fashion with representatives from the other sections explaining the composition of the upstream and downstream costs. These items are added to the income statement started by the first group representative. The final result is a completed income statement.

Step by Step Answer:

a Raw materials Utilities Note 1 Labor Depreciation on manufacturing equipment 10000000 2000000 8 Se...View the full answer

Fundamental Managerial Accounting Concepts

ISBN: 978-0078025655

7th edition

Authors: Thomas Edmonds, Christopher Edmonds, Bor Yi Tsay, Philip Old