Prove that the forward swap rate can be understood as a weighted average of all forward LIBORs

Question:

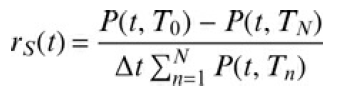

Prove that the forward swap rate

can be understood as a weighted average of all forward LIBORs within the tenor of the swap.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The forward swap rate F can be represented as F S x T1 L x T2 where S ...View the full answer

Answered By

SABARI P R S

My name is Ajith. I have completed my graduation from Mahatma Gandhi University Kottayam and also completed certificate of computer application with two year experience.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: